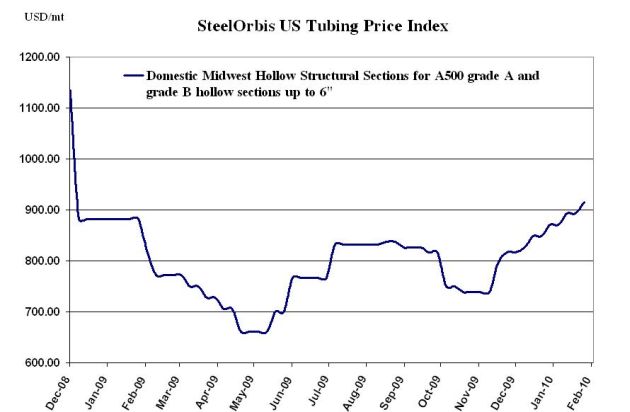

Spot prices for US hollow structural section (HSS) tubing have moved up slightly since our last report, although the second $3.00 cwt. ($66/mt or $60/nt) price increase announced by mills in January has yet to be fully accepted.

Most spot offers have gone up approximately $1.00 cwt. ($22/mt or $20/nt) and now range between $41.00 cwt. to $42.00 cwt. ($904/mt to $926/mt or $820/nt to $840/nt) ex-mill, despite mills’ continuing to push for $43.00 cwt. to $44.00 cwt. ($948/mt to $970/mt or $860/nt to $880/nt) ex-mill. Deals may still be available for those purchasing significant tonnage, but buyers are reluctant to buy large tonnages therefore most deals are executed at the above level.

For the West Coast, tube makers are still offering a range from around $42.00 cwt. to $44.00 cwt. ($926/mt to $970/mt or $840/nt to $880/nt) ex-mill.

Flat rolled prices continue their upward trend, but tubing demand has not increased noticeably until now, and is expected to remain relatively flat through the spring. But since tubing mills see their raw materials cost increase they will continuously push for higher prices in order to protect their margins.

Offshore offers have become relatively quiet since our last report Mexican offers have remained neutral and are still being priced between $38.00 cwt. to $40.00 cwt. ($838/mt to $882/mt or $760/nt to $800/nt) delivered to California and Texas. There are some Turkish and Korean offers that are more competitive for larger and unusual sizes, yet many traders are hesitant to take the 4-month gamble at the offered pricing.