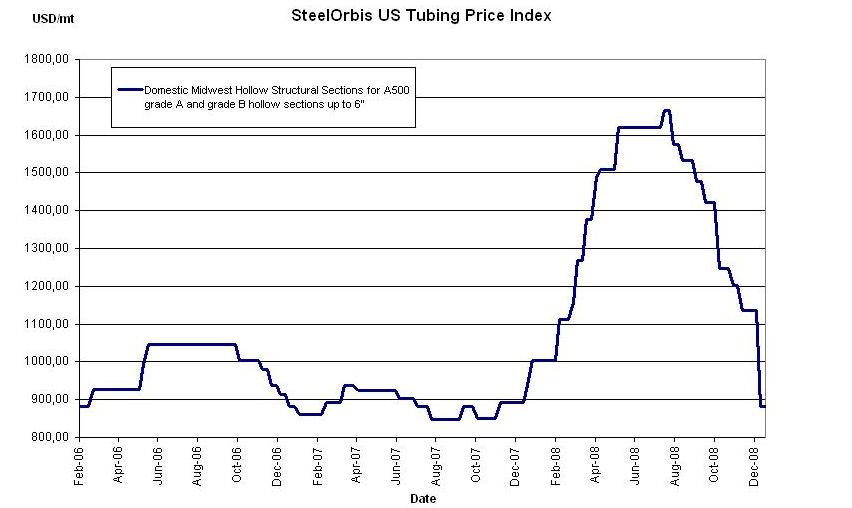

US domestic hollow structural section (HSS) demand remains weak, which may result in further, albeit more modest price declines on top of the drastic price decreases seen in December.

Official domestic HSS prices at the mill level have remained unchanged from SteelOrbis' report two weeks ago and are still offered in the approximate range of $39.00 cwt. to $41.00 cwt. ($860 /mt to $904 /mt or $780 /nt to $820 /nt) for A500 grade A and grade B hollow sections up to 6" ex-mill in the Midwest. However, buyers may be able to negotiate deals for substantial orders of certain sizes at around $38.00 cwt. ($838 /mt or $760 /nt). The next decrease, probably a moderate one, is expected before the end of January. This decrease will likely be in the vicinity of $1.00 cwt. to $2.00 cwt. ($22 /mt to $44 /mt or $20 /nt to $40 /nt), and should more accurately reflect the actual spot prices, which have been sliding due to the slow demand.

In addition to the overall weak demand for HSS, the credit crisis continues to loom over the heads of many potential buyers. Despite the prospect of good fortune that President-elect Obama's proposed infrastructure plan could bring to the US steel industry, any positive effects of the plan will most likely not be experienced until after the second quarter, at the very earliest.

On the import side, foreign tubing offers continue to have difficulty competing against domestic offers, mostly due to lead times and the small price gap between import and domestic offers. However, prices from Turkey are firming because of the rising raw material costs in the region. Turkish offers went up by $2.00 cwt. since our last report and now range approximately from $35.00 cwt. to $36.00 cwt. ($772 /mt to $794 /mt or $700 /nt to $720 /nt) FOB loaded truck, US Gulf Coast ports. Most HSS tubing offers from Mexico have remained unchanged since our last report, still slightly less than domestic offers at a range of about $37.00 cwt. to $39.00 cwt. ($816 /mt to $860 /mt or $740 /nt to $780 /nt) delivered to Texas and California. Further price declines are expected over the next couple of weeks, or even longer, depending on how long the domestic tubing price continues to fall.

As for the West Coast, South Korean HSS tubing offers to the US are becoming more frequent and are in the range of about $36.00 to $37.00 ($794 /mt to $816 /mt or $720 /nt to $740 /nt) duty-paid, FOB loaded truck in West Coast ports. Meanwhile, Chinese offers have yet to gain any US interest although the Chinese government lifted its fifteen percent export tax on HSS products in December.

Census and license data from the US Import Administration demonstrate that Canada exported the most structural pipe and tube tonnage to the US during the third quarter of 2008, with 38,361 mt. South Korea and Mexico were the second and third largest import tubing sources over that time period, with 14,814 mt and 7,491 mt respectively.