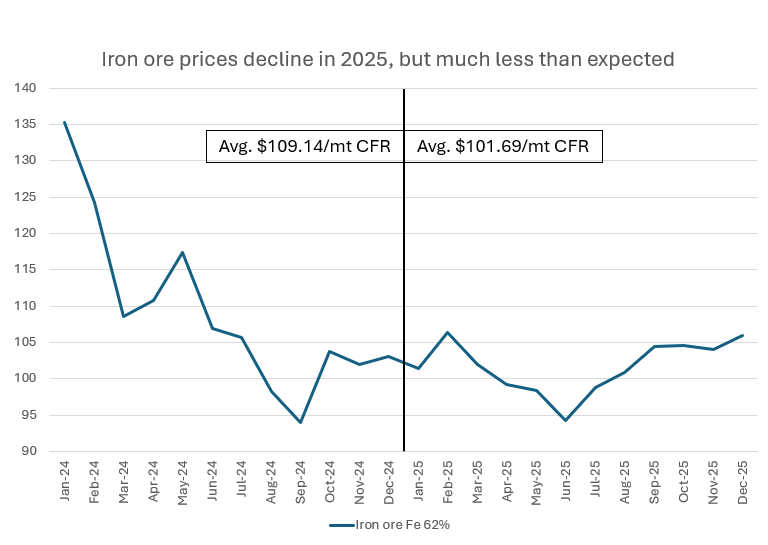

The major raw material markets - iron ore and coking coal - were moving in very different directions in 2025. The iron ore market, the most carefully watched of these two markets, did not follow a common logic, according to market sources, with far more price declines having been expected. At the same time, the global coking coal market was more based on fundamentals, with the supply of high-grade coal being the major factor. SteelOrbis has polled market sources regarding their forecasts for the dynamics of these two major raw material markets in 2026.

China’s crude steel output fell by four percent or 37 million mt in January-November 2025, while iron ore imports, in contrast, amounted to 1.1392 billion mt, up 1.4 percent year on year. The overall iron ore imports in 2025 will likely exceed 1.237 billion mt, the previous historical high recorded in 2024. The answer to these illogical dynamics of steel production and iron ore imports lies in two major fields: expectations of a better market situation and changes in import grades.

Expectations became the leading driver. After falling to low prices in June and July, import iron ore prices saw a continuous rebounding trend as China aimed to put an end to involution-driven competition, while the iron ore contract price at Singapore Exchange exceeded $100/mt, reinforcing the market’s restocking activities to some extent. In addition, market players expected an improved performance due to China’s pro-growth policies and macro-stimulus measures, resulting in steelmakers and traders’ willingness to build up stocks of iron ore.

“The iron ore prices moving at high levels [in 2025] have mainly been due to expectations and structural conflicts, and not from an actual improvement in downstream users’ demand,” a Chinese source commented.

Promising expectations together with a significant drop in real iron ore consumption in China eventually resulted in a rise in port stocks, which reached 159.7 million mt (for 45 ports, reported by Mysteel) in the last days of December 2025, a level last seen in February 2022. This shows that port inventories added almost 20 million mt since late September 2025. One large trader said that iron ore port inventories above 150 million mt are unnecessarily high and should put pressure on prices and “kill” all hopes of traditional seasonal restocking activities in 2026.

Another reason for the higher volumes of iron ore shipped to China was the much bigger share of Australian iron ore with Fe content of 60.8-61 percent, versus the previous benchmark 62 percent Fe fines. “This is simply because mines [in Pilbara mainly] depleted higher Fe resources,” a representative of a Chinese mill said. Also, Chinese mills prefer to blend bigger volumes of fines with slightly lower Fe content, trying to balance costs.

- Downtrend in iron ore to continue in 2026, but…

Prices of iron ore imports for China are expected to continue to move down in 2026, according to all major analysts and investment banks. But whereas a year or two ago all of them expected prices for the benchmark fines with 62 percent Fe content to go below the $90/mt CFR mark (forecasts a year ago were in the range of $80-90/mt for 2026), now all expectations are higher. In fact, most price forecasts range from $98/mt CFR to $90/mt CFR, with only Citi Group remaining pessimistic, citing all the negative factors that should put pressure on prices.

Price forecasts of major investments banks and analysts for 2026, iron ore fines Fe 62%, CFR China

| Invest bank/analyst | Recent price forecast for 2026 |

| Wood Mackenzie | $98/mt |

| JP Morgan | $95/mt |

| BMI | $95/mt |

| Goldman Sachs | $93/mt |

| Fitch Ratings | $90/mt |

| Citi | $85/mt |

So, basically the higher-than-earlier price forecasts for iron ore prove that the market is unlikely to become fully logical, at least in 2026. Even though two main fundamental drivers will try to pull prices down further.

In terms of supply, the new Simandou project is expected to export around 20 million mt of iron ore in 2026. “Simandou is a game changer, yes, since we do not expect any big rises from Australia [in 2026], but Vale itself may provide some surprises,” a market source said, saying that the increase in supply volumes may be even bigger.

In terms of demand, as SteelOrbis published earlier, China’s steel production is forecast to decline by a further 15-35 million mt in 2026, so, even in the best-case scenario, the decline in iron ore consumption may reach 20 million mt.

But these factors would have more impact if the market was more logical. At least in the short term of one year, market sources expect a continuation of the dispute between BHP and the Chinese government-based iron ore procurement arm China Mineral Resources Group (CMRG). For now, the Chinese side has failed to achieve lower prices and managed to insist only on some tonnages being shipped on RMB price terms.

In December, CMRG made another attempt to gain more pricing power for the Chinese mills - it proposed to increase storage fees for foreign companies having their own stocks at Chinese ports. According to unofficial information, CMRG has sought to charge RMB 0.1/mt per day, after a 30-day free period, increasing the fee to RMB 1/mt after 180 days. So far, there has been no reaction in the market to this attempt.

"The Chinese would really like CMRG to be more effective. So far, the fundamentals of demand and supply continue to define the price," commented Gautam Varma, founder of commodity advisory firm V2 Ventures, who previously worked at Fortescue, as reported by Reuters.

- Indian factor

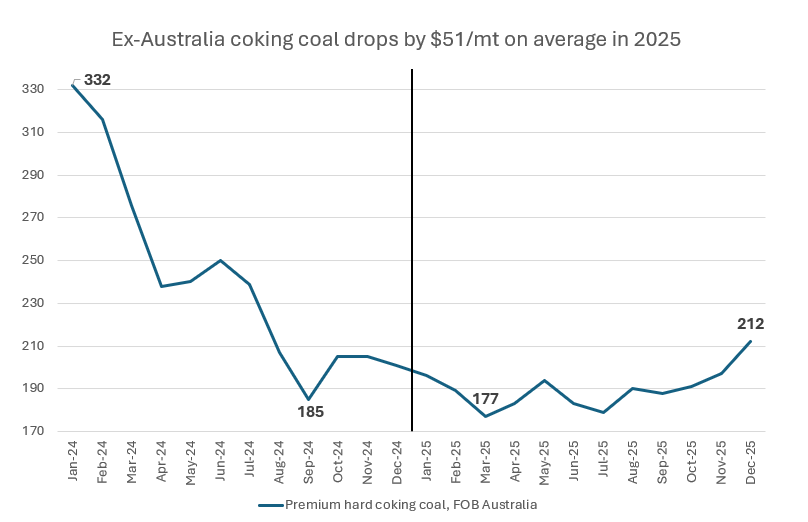

Unlike the situation in iron ore, the leading Australian coking coal export market has been dependent on the main fundamentals: weaker demand led to a drop in premium hard coking coal (PHCC) prices from Australia by 21 percent or $51/mt to $190/mt FOB on average in 2025. At the same time, supply of coking coal remained one of the major factors in the market.

The price range in 2025 narrowed significantly. The highest price level was seen in December at $212/mt FOB on average (or $220/mt FOB as the highest tradable level at the end of the month). This hike in the last quarter of 2025 was due to the increase in demand from India and the reduction in supply for December-January laycans in Australia.

For the Australian coking coal market, over the past two years India has come to play a bigger role as it is still a growing market with great potential and needs high grade coking coal that cannot be supplied in the same big volumes by other global suppliers.

India’s coking coal imports during the April-December period of the fiscal year 2025-26 totaled 48 million mt, a rise of 11 percent or 4.7 million mt year on year, according to the India Ports Association. Australia’s share in total Indian imports came to 48-51 percent in this period, so Australia benefited from the growth in demand in general. But since Indian mills have been actively trying to diversify their import sources, Australia’s share now is much less than in 2021 when it was up to 80 percent. Cheaper Russian coking coal managed to account for a 25 percent share in the Indian market, a surge from less than 10 percent in 2021. Coking coal supply from the US and Mozambique totaled 20 percent to India in 2025, more than double since 2021.

As for the forecast for 2026, Australia’s Department of Industry, Science and Resources expects the ex-Australia PHCC price to be at $190/mt FOB, relatively stable from the level seen in 2025 amid strong demand from India in the first quarter and part of the second quarter. Supply of coking coal from Australia totaled 146 million mt in the 2024-25 financial year (July 2024-June 2025), down by 4 million mt year on year, but in the 2025-26 financial year export volumes are forecast to rebound by 5 million mt.

- Chinese factor

China’s total imports of coking coal decreased in 2025. In the January-November period of 2025, China’s coking coal imports amounted to 104.8558 million mt, down 5.67 percent year on year. Moreover, as steel mills in China focused on cutting costs, they chose to buy more from Mongolia and Russia - focusing on medium and low-grade coking coal and PCI, and from Canada - focusing on higher grade PHCC (which is cheaper than the same material from Australia). In 2025, there was a very short period when Chinese mills resumed purchases of Australian PHCC, but total import volumes from Australia to China in 2025 will be below 8 million mt.

China’s coking coal imports in Jan-Nov 2025, million mt

| Country | Volume | Share | Change (y-o-y) |

| Mongolia | 53.36 | 50.89% | +1.50% |

| Russia | 29.16 | 27.81% | +4.56% |

| Canada | 9.7 | 9.25% | +21.30% |

| Australia | 7.08 | 6.75% | -18.51% |

| The US | 2.91 | 2.77% | -69.94% |

| Total | 104.856 | 100% | -5.67% |

China’s coking coal imports in 2026 will likely reach 119 million mt, up 3-4 million mt year on year, with the increase expected to come mostly from Mongolia, as the transportation restrictions seen in 2025 are expected to ease.

China’s coking coal output in 2026 may rise by 5 million mt amid the fading impact of environmental protection and safety inspections which affected output previously, and with new coking coal mines coming into operation.

As a result, there will be a lack of support from the Australian market coming from China in 2026.

At the same time, Chinese coke exports will see a decreasing trend in 2026 due to India’s AD duty at $130.66/mt, increased competition with Indonesia, and negotiations between China and Japan. The oversupply of coke in China may continue in 2026 with some capacities being put into operation. Coke capacity in China is foreseen to reach its peak level in 2028 and then to start shrinking.