The pricing trend for domestic hollow structural section (HSS) remains neutral from our report two weeks ago as buyers and sellers in the domestic market continue to proceed with caution. Tubing mills have not yet reacted to the price increase announcements made by leading flat rolled mills over the past week that cited an average of $1.50 cwt. ($33/mt or $30/nt) increase on spot prices on all hot rolled coil (HRC) products. After Atlas Tube's late September HSS price increase announcement of $1.50 cwt. ($33/mt or $30/nt) didn't stick whatsoever, and spot prices even dropped about $3.00 cwt. ($66/mt or $60/nt) further in the weeks that followed, mills are being careful not to replicate hot rolled coil (HRC) price movements too suddenly.

Some tubing buyers view the recent HRC price announcements as not really a reaction to any upticks in demand levels, but rather just an attempt "to stem the tide of massive decreases." Therefore, many HSS mills are skeptical as to how effective the price increases will be, and are opting for a wait-and-see policy before issuing any price announcements of their own. Overall, if the entirety of the HRC price increase doesn't hold, it could take until the end of Q4, and possibly the start of 2011 before the HSS market issues any sort of price adjustment.

Order books for November remain soft, with those for December not faring much better, as year-end inventory levels continue to be the main concern for buyers who don't want to pay taxes on product that's just "lying around" at year's end.

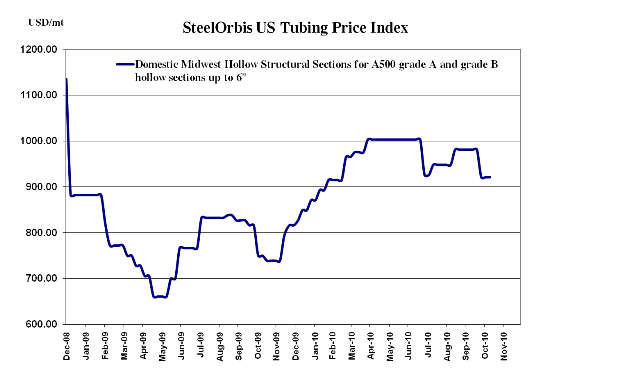

So for now, domestic spot prices remain at previously reported levels of $41.00-$43.00 cwt. ($904-$948/mt or $820-$860/nt) ex-Midwest mill, and $45.00-$46.00 cwt. ($992-1,014/mt or $900-$920/nt) delivered ex- West Coast. There are still plenty of deals out there, however, and reports of orders being placed $0.50-$1.00 cwt. ($11-$22/mt or $10-$20/nt) below the above ranges are not uncommon.

Looking offshore, import offers remain scarce, with rumblings of offers from Turkey not garnering any real interest from domestic buyers.

In terms of inventory from imports, preliminary license data from the US Steel Import Monitoring and Analysis System (SIMA) demonstrate that total import tonnage of structural pipe and tube fell significantly in October to 21,785 mt from the 29,352 mt imported in September, likely a result of lackluster demand in July in August. SIMA also reports that imports from Canada and China experienced the sharpest monthly decline in October, falling from 14,782 mt to 9,807 and 4,699 mt to a mere 1,986 mt, respectively.