Although US flat rolled demand is unlikely to exhibit any real up-tick in the near future, there are a few factors that are providing glimmer of hope on the horizon.

According to the most recent Metal Service Center Institute (MSCI) monthly shipment and inventory report, monthly flat rolled shipments increased from 1.40 million nt in February to 1.53 million nt in March; total flat rolled inventory decreased from 4.45 million nt in February to 4.23 million nt in March; and average service center inventory overhang decreased from 3.2 months in February to 2.8 months in March. However, even though most service center inventory factors improved in March, monthly shipments are still down by an astounding 1.39 million nt and inventory overhang has grown by an estimated 0.5 months, since March 2008.

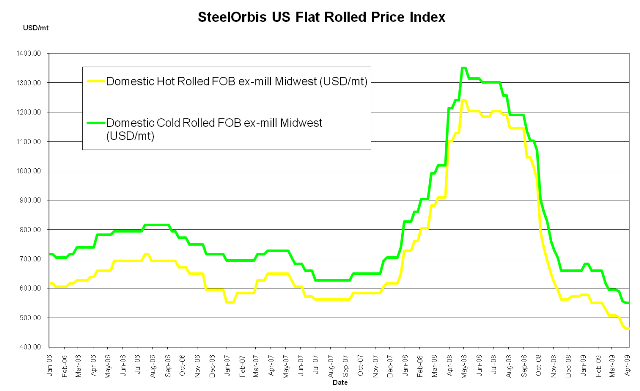

In addition to the slowly shrinking inventories, another glimmer of hope is the potential upward correction in domestic scrap pricing in May , which could produce some market confidence heading into the summer months.For the first time in about a month, most domestic hot rolled coil (HRC) and cold rolled coil (CRC) spot prices trended sideways this week, resulting in the average HRC offering range remaining at approximately $20.00 cwt. to $22.00 cwt. ($441 /mt to $485 /mt or $400 /nt to $440 /nt) and CRC offers ranging from $24.00 cwt. to $26.00 cwt. ($529 /mt to $573 /mt or $480 /nt to $520 /nt) ex-mill in the Midwest. However, the current overall lack of demand will continue to contribute to softening prices and will place pressure on US mills to offer discounts to customers depending on order size and specifics.

The three major minimills (Nucor, SDI and Severstal) have been the price leaders and have been competing fiercely for each order. The integrated mills also do not want to lose market share and in a business environment like this, it is easy for seasoned and serious buyers to play one mill against another to negotiate lower numbers.

On the import side, foreign mills continue to follow US domestic prices downwards as foreign mills attempt to compete with the aggressive US mills; however, generally the import price deductions are coming too little too late to attract any attention and imports cannot come close to matching the domestic mills' short lead times.

Mexico has been the primary competitive foreign source offering HRC and CRC to the US mostly due to Mexican mills' proximity to US borders and their ability to ship quick orders. However, their order books for May shipments are filling up quickly and most mills are no longer eager to do quick orders for HRC or CRC shipments. While one of the major Mexican suppliers is completely out of market, another continues to offers to US customers aggressively. Therefore Mexican CRC offers still decreased by about $1.00 cwt. ($22 /mt or $20 /nt) over the past week and now range from approximately $24.00 cwt. to $26.00 cwt. ($529 /mt to $573 /mt or $480 /nt to $520 /nt) delivered to the US at the border crossing, and in some cases, delivered to major cities in Texas and beyond. Mexican HRC offers to the US, in the meantime, remained at about $20.00 cwt. to $22.00 cwt. ($441 /mt to $485 /mt or $400 /nt to $440 /nt) delivered to the US at the border crossing.

On the CRC side, Argentina also lowered their offered prices by about $1.00 cwt. ($22 /mt or $20 /nt) over the past week to keep pace with Mexico and most offers now range from approximately $24.00 cwt. to $26.00 cwt. ($529 /mt to $573 /mt or $480 /nt to $520 /nt) duty-paid, FOB loaded truck in US Gulf ports, while most Brazilian offers remained at about $25.00 cwt. to $27.00 cwt. ($551 /mt to $595 /mt or $50 /nt to $540 /nt) duty-paid, FOB loaded truck in US Gulf ports, with the ability to negotiate for significant orders.

Furthermore, Indian and Chinese CRC offers remained unchanged since last week at about $26.00 cwt. to $28.00 cwt. ($573 /mt to $617 /mt or $520 /nt to $560 /nt) duty-paid, FOB loaded truck in US Gulf ports. Indian mills will probably be willing to lower their offers by about another $1.00 cwt. ($22 /mt or $20 /nt ) depending on order specifics, while Chinese offers remain about $1.00 cwt. $22 /mt or $20 /nt) higher than their competition.