Upon returning to office, President Trump acted swiftly to strengthen Section 232 tariffs on steel and aluminum. In February 2025, he issued proclamations that eliminated all remaining country-specific exemptions and product exclusions while raising the tariff on aluminum imports to 25%, aligning it with the steel rate, effective March 12, 2025.

On June 4, 2025, the tariffs on both steel and aluminum were doubled to 50%. These actions have not been overturned in court because the administration adhered to the required Section 232 process under the Trade Expansion Act of 1962. Trump directed the Department of Commerce (DOC) to investigate potential threats to national security. The DOC found that excessive imports were impairing domestic production from reaching the necessary levels to support defense and critical infrastructure requirements. The DOC had originally recommended policy measures sufficient to bring U.S. steel mill capacity utilization up to at least 80%.

Other factors have helped shore up steel prices, of course. Phil Flynn, market analyst in the energy sector for the FOX Business Network, told SteelOrbis that a continuation of elevated global oil prices could continue to support steel prices, most likely through the end of 2026. He said the combination of high energy prices with elevated freight rates is expected to further slow import competition with domestic supply.

Flynn, who also serves as Senior Account Executive at the Prices Future Group, added: “Diesel and bunker fuel prices have been through the roof and there’s been an exceptional squeeze in some parts of the world. High energy prices have been a particular issue, especially with the steel mills in Asia and Europe. Still, the margins for steel producers should stay positive into the new year.”

US steelmakers’ recent financial performance

Recently, US steelmakers reported strong financial performance in Q1. In the case of Nucor, the company reported $743mn of net earnings, up by 376 percent from $156 million in Q1 2025, just before the steel tariffs were implemented, while shipments reached 7.4mn nt, up by 9pc during the same period. The company reported an 86pc steel mill utilization rate from 80pc during the same period.

In the first quarter of the year, Steel Dynamics Inc. (SDI) reported a net income of $403.4mn, up by 85pc from $217.1mn in Q1 2025. The company’s total shipments reached 3.63mn nt, up by 4.3pc from 3.48mn nt during the same period.

Cleveland Cliffs (Cliffs) still reported a net loss in Q1, but at least it was smaller than last year. This year, it amounted to a negative $229mn from a negative $486mn in Q1 2025. The company’s EBITDA did see a significant improvement during the same period, rising to $97mn from a negative $213mn. It should be noted that Cliffs still relies heavily on blast furnaces (BOFs) as opposed to SDI or Nucor. Cliffs acquired scrap processor Ferrous Processing and Trading Company (FPT) in 2021 to serve its future decarbonization processes.

Financial results for steelmakers were not immediately positive when the import tariffs were implemented, but this year, it appears that the benefits of the trade policies are accelerating. It is not yet a definitive conclusion, but steelmakers are attributing (in part) their better performance to the import duties. Nucor’s chief executive officer (CEO), Leon Topalian, attributed the strong performance in Q1 to increased demand, higher investment contributions, and tariffs. In his words, “federal trade policies that continue to reduce the flood of unfairly traded imports to the US”.

Data from the American Iron and Steel Institute (AISI) show that this year the US steel sector’s installed capacity utilization rate has breached the 80pc threshold (historically a good level) for five weeks since Q2 began, peaking at 82.2pc in the week of May 16. The 80pc level had not been seen since the week of August 24, 2024.

Nevertheless, even though the signs are positive, it might be too little in a short span of time before definitive conclusions can be reached. After all, long-lasting shifting trends in the industrial sector tend to move at glacial speed. It can be surmised that a positive enduring trend may be brewing, but not a return to the golden era of the 1970’s, as an example. The US steel sector just lost too much in the years in between.

Have scrap prices been lagging compared to steel prices?

Ken Schutt, chief operating officer (COO) of Kimmel Scrap Iron and Metal Company in Detroit, helped explain why ferrous scrap prices have not grown on par with finished steel prices. He commented on which grades and products are being compared, what is the historical reference, and what is the logic, from the seller's point of view, of why scrap could be presently undervalued?

“I guess to look at it historically, if you go back a couple of years, you know, the number that was often used in the spread between busheling and hot-rolled coil, the sweet spot at that time was around $400. And if you're looking at it now, hot-rolled coil is at $1086/nt this week. And you've got Detroit busheling priced at $450/gt. So, now you're looking at a difference of $600. Should busheling be $236/gt more dollars today? I don't know if it should be that much higher, but I believe we should be getting paid more. I do believe mills are suppressing the market”.

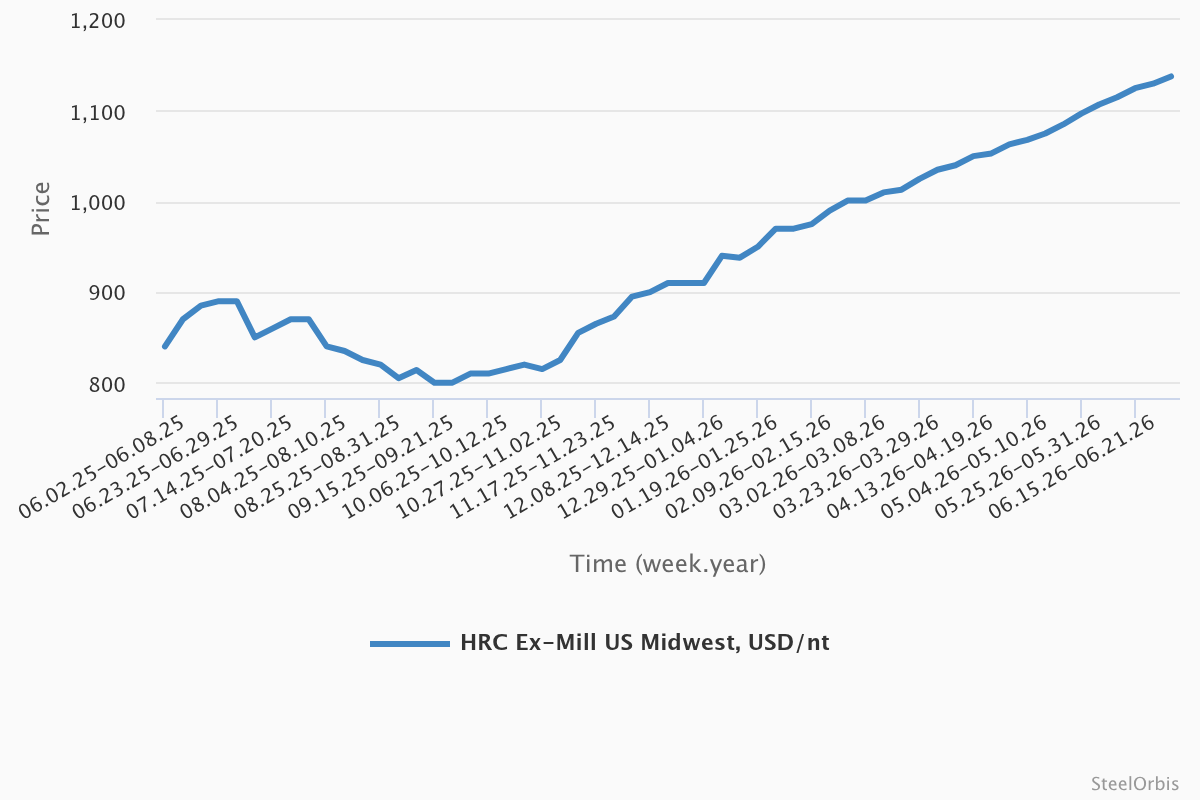

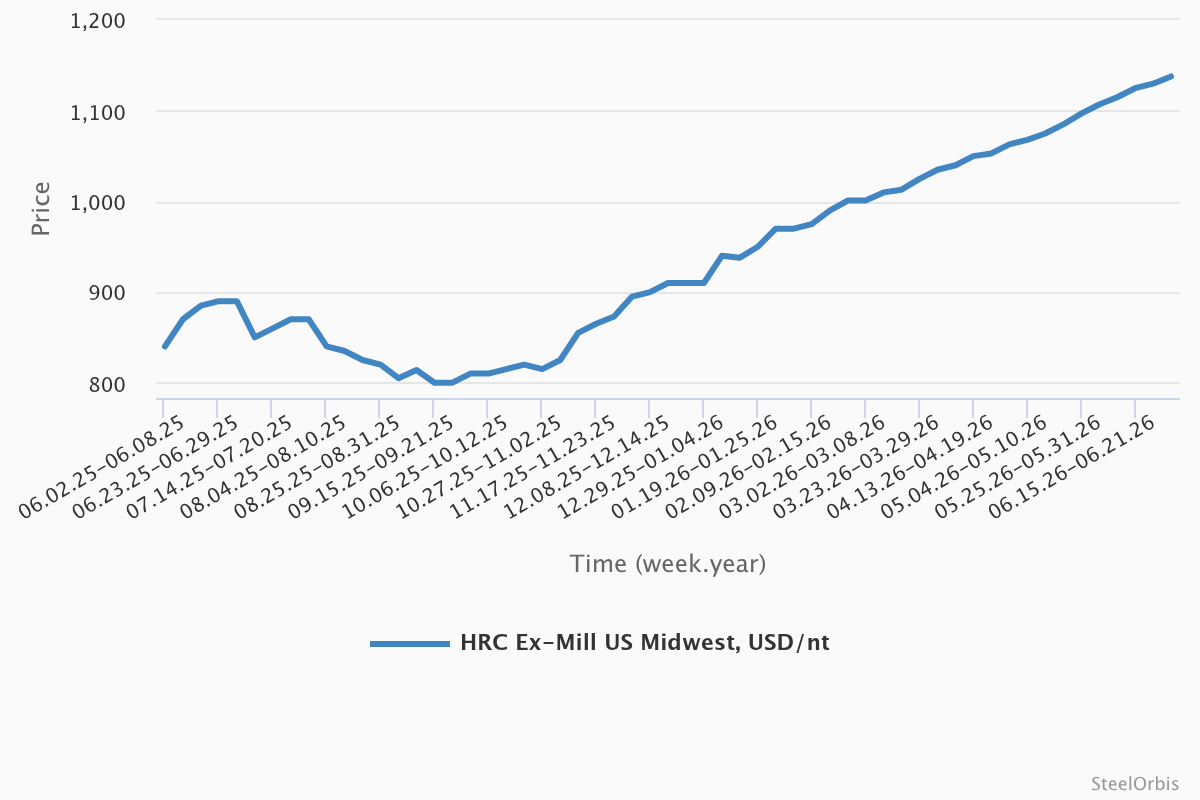

Indeed, #1 busheling has actually decreased by 6.2pc in the Chicago domestic market to $450/gt delivered consumer in June from $480/gt delivered in March 2025 (and has practically stayed at the same level from February 2025, when it was also at $450/gt delivered). During the same period, the price of hot-rolled coil (HRC) has grown by 31pc to ex-US mill $1,124.75/nt as of Jun 24 from $859/nt in March 2025.

Prices for HRC in the US have grown continuously since Q4 2025

“In the last four months, certainly, we haven't seen the scrap market move in tandem with hot-rolled coil. You can attribute this to, to a lesser extent, the export market, as well, up the East coast for heavy melt, the domestic prices aren't moving in tandem with that, but again, the spread is much tighter”, Schutt added. “Pig iron and busheling, you know, tend to trade fairly close to each other. Pig iron, we’re currently seeing it at $530/mt CFR US. You're looking at an $80/gt spread there. That in turn should start to make busheling look more attractive than pig iron. You would assume that they're going to supplement more of their pig iron with busheling because it's cheaper”, he added.

HMS I for the export market in the US East Coast (USEC), for example at the Philadelphia docks, has grown by 15 percent since March 2025 to a current level of $270-280/gt delivered export yard. To compare pig iron with #1 busheling prices in the Midwest, a $530/mt CFR New Orleans (NOLA) price (as of late June) that considers a conversion to $538.5/gt, plus transloading, barge and trucking costs, would result in a $606/gt delivered US mill equivalent. That is about a $156/gt spread with #1 busheling prices in Chicago, and slightly less in other markets, for example, Cleveland, where busheling prices lie slightly above at $475/gt delivered consumer as of June.

Some stakeholders in the scrap sector have noticed an interesting trend. Even with high installed capacity utilization rates for the steel sector, and robust demand for finished steel, scrap consumption does not seem to be moving up significantly either.

“With all of this HRC that is flying off the shelf, it is not translating to more scrap. So why is that not happening? I've not been able to pinpoint that. I’ve talked to my colleagues in Detroit, in Canada, in the US, asking, ‘Are you guys seeing the same thing?’ Demand for prime grades has not really returned. It fell off, going back to last year, 20-30 percent, and it just has never really recovered”, Schutt mentioned.

Is more scrap pouring into the US?

US scrap imports grew annually in 2025 by 5.3 percent to 5 million mt from 4.75 million mt in 2024 according to US Customs data, but could this increase account for the lag in scrap prices considering that finished steel production has been growing too? Data for 2026 is not in, of course, but so far the US has imported 1.84 million mt of scrap. There will be ebbs and flows in scrap consumption throughout the rest of the year, but the US could be on track to import 5.52 million mt of scrap by the end of the year, a 10.4 percent increase from 2025, and a 16.2 percent rise from 2024. The annual increases in scrap imports are not that impressive, but there is a steady stream of material into the US that keeps growing.

For context, US finished steel production in 2025 rose by 4.5pc to 89.3 million nt from 85.4 million nt in 2024. So, 2025’s rise in scrap imports seems aligned with the increase in finished steel production, and it does not seem that the rise in scrap imports is disproportionate.

A brief look into metallics

The rising prevalence of metallics in the steel-making mix has also been something put forward by some contacts as a possible reason for the stagnation in scrap prices. Some have mentioned that while years ago pig iron content in the steel mix was in the single digits, it has now been engineered to reach about 40 percent. It has been posited that scrap is becoming more polluted with alloys each year derived from specialty steel production. A look at pig iron imports, nevertheless, shows that at least in that area the growth has not been disproportionate. US pig iron imports in 2025 grew by 12.7pc to 5.3 million mt from 4.7 million mt in 2024. Yet it does not directly reflect consumption, and it remains to be seen how the new DRI plant at Big River Steel in Arkansas could affect consumption of prime scrap grades in the region.

Scrap viewed from the buyers' side

It is prevalent, though, to hear from contacts in the scrap trade that “steel and scrap prices are disconnected”. On this matter, a scrap buyer from a prominent mill in the Midwest helped us analyze the matter from his point of view.

“I don't see a correlation between finished steel prices, HRC, plate, long products, whatever you want to call it, and scrap prices. They're two different things. And it comes down to supply and demand. So I can't say scrap is undervalued. You know, it's just that scrap is basically supply-driven. In my career, that's the way it's always been. And right now, there seems to be plenty of supply. And that's why scrap prices are where they're at compared to finished steel prices”, he said.

“I don't like to compare them to finished steel prices because in the past, and it'll happen again, finished steel prices will go down, but scrap prices will go up. And we can't go back to the sellers and say, ‘Well, our finished steel prices are down, so your scrap prices should be down too’. They can say, ‘Well, we just don't have it to sell. And if you want it, we have a finite amount, and this is the price.’ So, even though our production might be down, our steel prices might be down, we still need scrap. So we have to pay what the market will bear. So right now, we're in a supply-rich environment”, he added.

Scrap supply in the US has been adequate since the winter months ended this year. Some contacts mention that the hot weather in summer could curtail scrap generation, a seasonal trend, but right now the weather is still a non-factor. As the buyer also mentioned, there is particularly more available material for shredded and obsoletes. Prime grades’ relatively tighter flows have also helped prices grow recently. As a matter of fact, for the July trading cycle, the whole market is expected to trend sideways with a possible $10-20/gt increase for #1 busheling. Some argue a slight decrease in cut grades is also a possibility.

Another recurring theme in the scrap trade is the need to uphold long-lasting relationships, both on behalf of the buyers and the sellers. Some agree that a short-term compromise sometimes is better for a long-term fruitful symbiosis. Yet, even with this in mind, the buyer notes that mills are sometimes wary of offering premiums on quiet deals for good reason.

“As a mill buyer, and I think I speak for many of them because I've known throughout my years, they're afraid to go out and put a premium on some of the deals with large processors, because they know it's not going to be quiet. It's going to get out into the market. Like I'm buying 100 tons from a local guy, and they hear that one of those big players got $20 more. Sellers can say, ‘Well, how come you're paying them more?’ And it just snowballs from there, and everyone hears it. So, why do quiet deals anymore? I prefer to say: ‘Here's my price to everyone. '" The buyer commented on the intricacies in scrap negotiations.

Moving forward: Will import tariffs remain in place to boost the US steel sector

Whether the duties stay is the easier question. The Trump administration has shown no inclination to retreat and has, if anything, deepened its commitment. A proclamation on April 2, 2026, moved the tariffs onto the full customs value of imported steel rather than the metal content alone, and a follow-up proclamation on June 1 further refined the scope and product coverage. Section 232 also rests on firmer legal ground than the broader tariffs imposed under the International Emergency Economic Powers Act (IEEPA). Even so, several of the relief provisions in the Section 232 Tariffs are written to expire on December 31, 2027, which is intended to leave the door open for rates to be dialed up or down as conditions change.

While the harder question is what happens after President Trump leaves office, the precedent is toward durability rather than repeal. The original 2018 steel tariffs outlived the president’s first administration once already. The Biden administration left them largely intact as support is not confined to one party. The Congressional Steel Caucus has a long bipartisan record, the United Steelworkers backs continued protection, and bipartisan proposals such as the Leveling the Playing Field Act 2.0 suggest the appetite for trade enforcement would survive a change in administration. This protection has created a safe environment for steel companies to invest billions in growth, something they would not likely commit to if they thought the tariffs were temporary.

More immediate is the July 2026 review of the United States-Mexico-Canada Agreement (USMCA), which will likely not be renewed for a blanket 16-year period but be reviewed year by year with little hope that steel tariff relief will come at its outcome. While any future president retains the same discretion President Trump has used to expand tariffs, for now, the tariffs look less like one administration's experiment and more like a settled feature of US trade policy, even if the sector's longer-term health will ultimately rest on demand, energy costs, and global overcapacity rather than on the duties alone.