USMCA – Will the Tariffs deliver Re-Shoring?

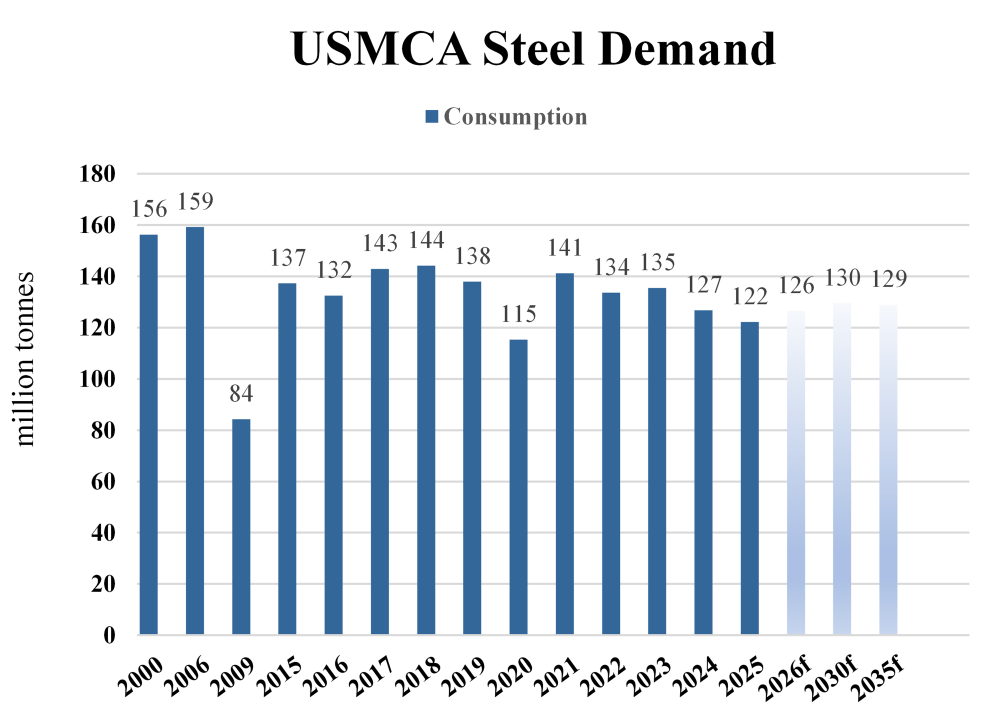

From the viewpoint of apparent consumption of steel products, the USMCA has been a stagnant to declining market for decades:

- On a finished product basis, ASC stood at about 156 million tonnes at the turn of the century, peaked-out at 159 million tonnes in 2006 and collapsed to 84 million tonnes in 2009 amidst the Great Financial Crisis.

- Demand slowly recovered in the following decade, reaching about 138 million tonnes in 2019 (and a peak of 149 million in 2014) just prior to Covid.

- After sharply contracting again in 2020 to 115 million, it rebounded to the recent high of 141 million tonnes in 2021 and has gradually declined since to about 122 million tonnes in 2025 (and an average of 128 million tonnes from 2023-2025).

Much of the decline in direct steel consumption can be ultimately attributed to the steady rise in net imports of indirect steel goods, which in the case of the USA alone have risen from about 22 million tonnes in 2015 to about 44 million tonnes in 2024 according to an analysis performed by AISI/WSA, of which a significant portion is cross-border trade with Mexico and Canada. On this basis, it’s easy to see why there is such an emphasis on the part of the Trump administration to re-establish manufacturing as a key driver of economic growth and reduce imports of foreign products – i.e. “re-shoring.”

The key question is: “will it actually happen?” And, if so, “to what degree?”

As WSD sees it, the challenges in achieving a meaningful resurgence in manufacturing-led economic growth, and consequently a recovery in direct steel demand, are substantial. The automotive sector might be the perfect microcosm for this dynamic:

- US imports of light vehicles from non-USMCA partners have averaged about 3.8 million units from 2019-2024. The dominant portion of this figure is comprised of vehicles imported from South Korea, Japan and Germany.

- All three of these countries are now subject to a 10 to 15% import tariff on their exports to the USA, including light vehicles. (Depending on how the latest policies take shape after the Supreme Court ruling on February 20, 2026 that the President cannot use the International Emergency Economic Powers Act (IEEPA) to impose tariffs.)

- Further complicating matters is the trade of steel intensive auto parts and components. In the case of Mexico, notable volumes of U.S. produced steel is shipped to Mexican auto-parts producers who then ship the parts back to the United States for final assembly further blurring the lines of what may be considered off-shore manufacturing and potentially inflating the calculations of cross-border indirect steel trade.

The question is whether this is a sufficient incentive to invest billions into localizing production in the USA? Considering the factories already producing them are largely depreciated, employ workers in the home countries (where governments are likely seeking to preserve the jobs) it is not out of the question that the bulk of these imports will simply carry-on whilst absorbing the new tariffs.

This report includes forward-looking statements that are based on current expectations about future events and are subject to uncertainties and factors relating to operations and the business environment, all of which are difficult to predict. Although we believe that the expectations reflected in our forward-looking statements are reasonable, they can be affected by inaccurate assumptions we might make or by known or unknown risks and uncertainties, including among other things, changes in prices, shifts in demand, variations in supply, movements in international currency, developments in technology, actions by governments and/or other factors.

The information contained in this report is based upon or derived from sources that are believed to be reliable; however, no representation is made that such information is accurate or complete in all material respects, and reliance upon such information as the basis for taking any action is neither authorized nor warranted. WSD does not solicit, and avoids receiving, non -public material information from its clients and contacts in the course of its business. The information that we publish in our reports and communicate to our clients is not based on material non-public information.

The officers, directors, employees or stockholders of World Steel Dynamics Inc. do not directly or indirectly hold securities of, or that are related to, one or more of the companies that are referred to herein. World Steel Dynamics Inc. may act as a consultant to, and/or sell its subscription services to, one or more of the companies mentioned in this report.

Copyright Ó 2026 by World Steel Dynamics Inc. all rights reserved