In 2025, imports of semi-finished products remained one of the key objectives for Turkish mills given their aim to balance out their costs, while in certain periods of the year the price situation in the finished steel sector, particularly in the longs segment, did not match the levels of production costs from imported scrap. Dealing for import billet and slab allowed Turkish mills to have more control over their margins or to soften losses in certain periods. In 2026, despite a lot of uncertainty mainly connected with CBAM in Europe, but also in terms of rising geopolitical issues as well as the general imbalance in global steel markets and the issue of overcapacity, Turkey is expected to sustain sizeable semis purchases, but might also increase scrap imports if it becomes attractive to increase EAF capacity utilization rates.

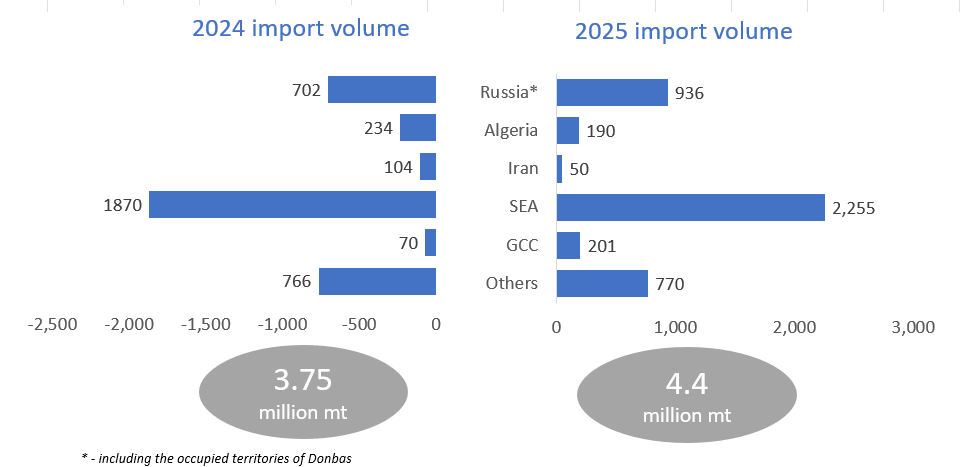

Turkey increased its square billet purchases by almost 15 percent in 2025 with the total volume reaching 4.4 million mt, versus 3.75 million mt seen in 2024. A share of over 50 percent belonged to shipments from Asian countries, with China and Malaysia being the top two suppliers. In particular, China increased its shipments to Turkey by 87 percent year on year to 937,000 mt, while Malaysia increased its shipments by seven percent to 858,000 mt. “Both these origins are the most regular if we are talking about long lead times, with China being the most plentiful since many suppliers out there are willing to sell. Malaysia, in its turn, is basically the only duty-free origin that can be dealt for on a relatively regular basis and this means that it was an option for Turkish steel producers and re-rollers to avoid issues with export licenses,” a Turkish trader told SteelOrbis.

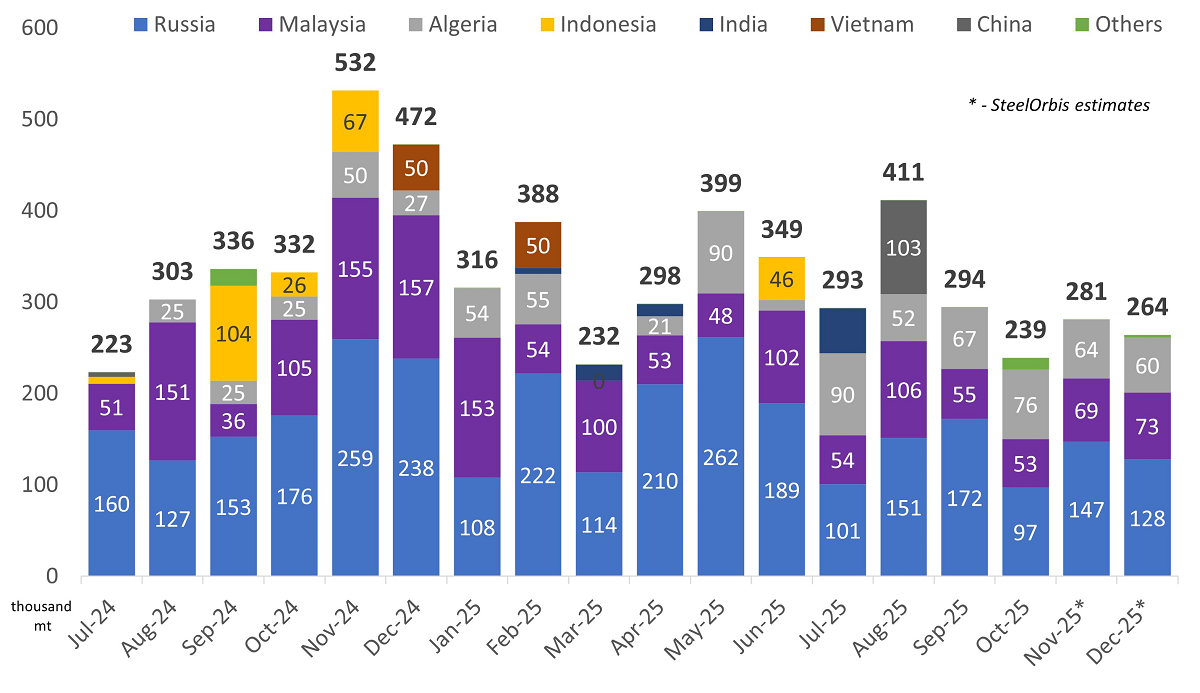

Turkey’s square billet imports

Suppliers from Russia, including the occupied territories of Ukraine’s Donbass region, increased shipments to Turkey by 25 percent in 2025, reaching close to 1 million mt. The key advantage remained the same - it is one of the few origins that can be booked in smaller volumes, whereas Asian billet has to be purchased in 20,000-50,000 mt lots depending on the supplying country. Another advantage is the short lead time - from immediate shipments to supplies in three or four weeks or longer. The pressure from the international sanctions applied on Russia and its steel sector in particular was not a much restrictive obstacle for many Turkish buyers in 2025, but the overall risky situation urged them to push for at least $30/mt lower price levels from Russia compared to the domestic workable billet price levels in Turkey.

Ukraine, where steel production is limited due to the ongoing military aggression of Russia, managed to sustain its billet sales to Turkey at 203,000 mt, supplied by two regular sellers. However, sources noted that in 2025 Ukraine’s presence in the Turkish market was more stable in terms of offers and deals, but still the Ukrainian mills prefer to first pay attention to some European destinations where workable prices can exceed those in the Turkish market.

The Algerian presence in the import billet market in Turkey declined by 23 percent in 2025. However, this did not disturb the market balance so much since the Algerian mill was selling to the Turkish company in the same holding. “It is most likely that the Algerian mill decreased shipments of billet to Turkey since using billets for its own longs to be sold domestically or for export was more profitable. Europe was also able to pay higher for billet than Turkey during a certain period of the year,” a Turkish producer told SteelOrbis.

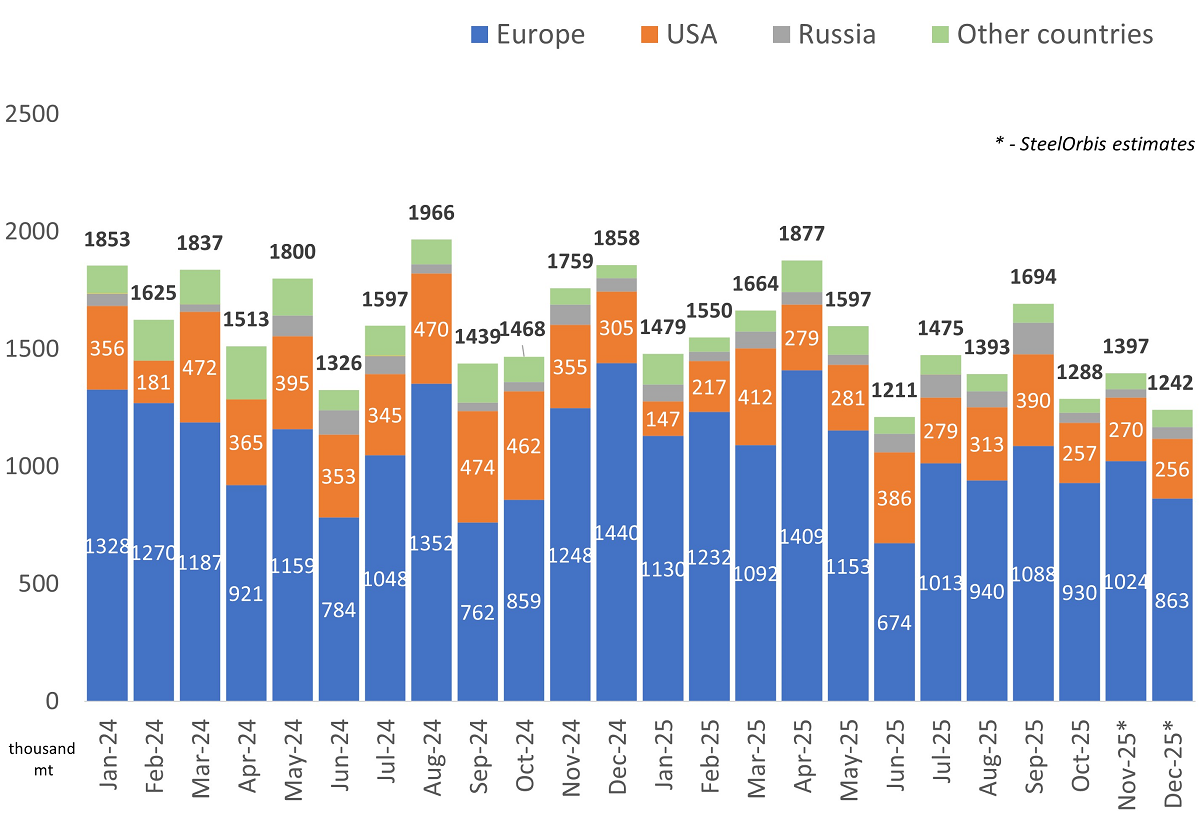

In the import slab segment, on the contrary, Turkish mills’ purchases indicated a decrease in 2025 by around seven percent to 3.76 million mt, versus four million mt in 2024. According to SteelOrbis’ evaluations, the availability of slab for the Turkish market, which was much less if compared to billet, affected the volume of shipments. Basically, most supplies were done by Russia, including shipments from the occupied territories in Donbass, with Russia leading the imports to Turkey with 1.9 million mt, versus 1.7 million mt in 2024. Again, the shorter lead time from the Black Sea coupled with high BF quality were the main advantages, along with the fact that Russian slab was at times a minimum $30-40/mt less expensive than that from Asia. In their turn, Malaysia and Indonesia were first focusing on their HRC sales, since in 2025 both had firmly entered the commercial segment with the high-paying EU market targeted. In addition, even in terms of the slab trade, Turkey is not considered to be one of the highest-paying destinations compared to the EU and Latin America. In 2025. Malaysia traded 0.9 million mt to Turkey, being in demand as a duty-free origin, down from 1.4 million mt in the previous year.

Turkey’s steel slab imports

Along with abovementioned situation in the import semis segments, in 2025 Turkey’s own square billet production increased by 5.4 percent to 24 million mt, while slab output fell by 1.4 percent to 13.9 million mt, according to SteelOrbis Research’s data. In the meantime, the total scrap imports to Turkey in 2025 are estimated at almost 17.9 million mt, versus slightly over 20 million mt seen in 2024. The European countries, including most of the EU Baltic states as well, topped the list of the suppliers with around 70 percent of the total shipments to Turkey, followed by the US with a 20 percent market share.

Turkey’s ferrous scrap imports

In 2026, according to the opinions collected from the market and according to SteelOrbis’ evaluations, Turkey will overall preserve the scheme of balancing its own production costs with semi-finished imports and, again, the availability of slab will be less than for billet. The main question is which shifts might be seen this year due to the influence of CBAM implementation in Europe and its potential effects on trade flows from Turkey to Europe.

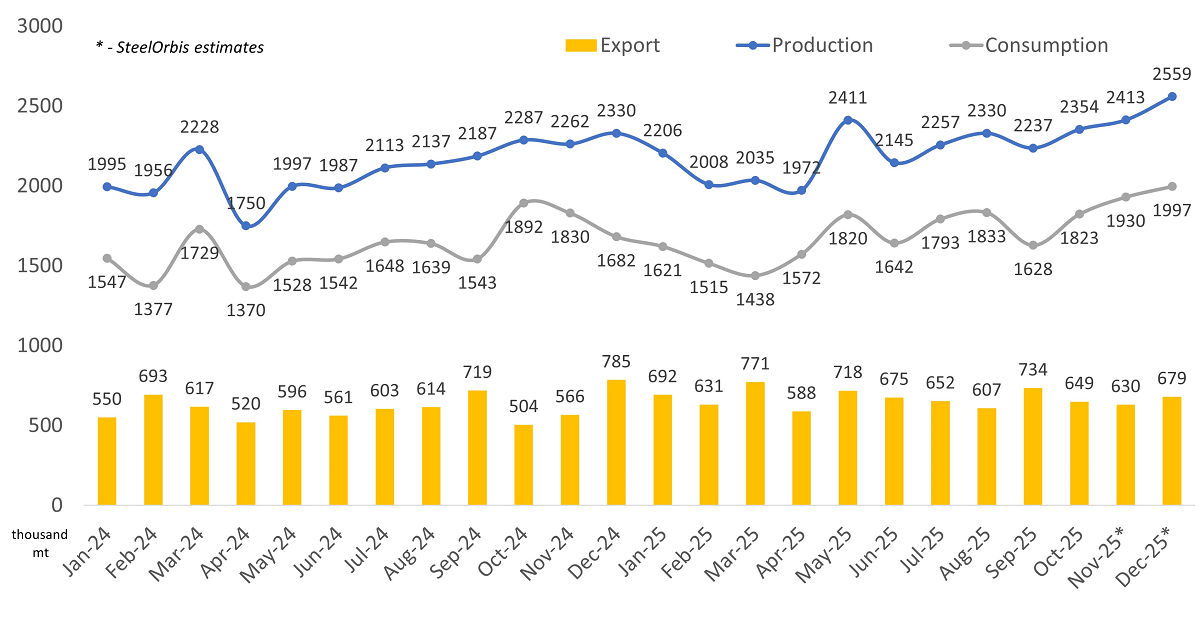

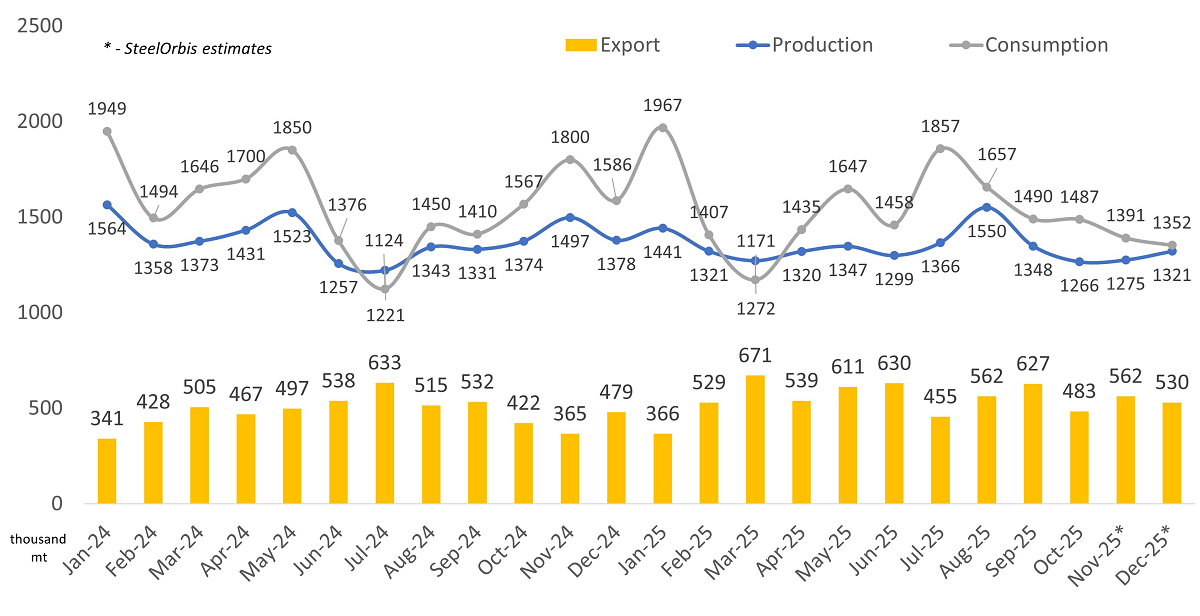

In 2025, according to SteelOrbis Research’s estimates, Turkey’s square billet capacity utilization rates stood at 58 percent on average, so, in theory, there is a room for EAF billet production to rise. However, the general situation in the longs segment, particularly the rebar segment and specifically in the export segment, will most likely put a ceiling to any potential billet production increase in Turkey. Although in 2025 the estimated consumption and export numbers for longs in Turkey indicated an increase of seven percent and 10 percent, respectively, there is hardly much more room for further rises, particularly on the export side.

Turkey’s longs production, consumption and exports

In fact, import quotas for Turkish materials have been decreased in the EU markets, and much attention is expected to be focused on non-EU destinations in Europe, where strong competition is expected to continue with suppliers from Egypt and Algeria. Some sources are hopeful for the easing of the situation with Israel, which could reopen doors for imports from Turkey. Similarly, there are certain hopes for increasing demand from Syria for ongoing reconstruction projects. Some players are optimistic also regarding the market in Ukraine, being hopeful of a positive outcome of the peace talks to end the war in Ukraine. However, many believe this is a rather long shot for an increased number of orders from Ukraine to be seen in 2026. The domestic longs market in Turkey, which accounts for around 70 percent of Turkey’s production, seems more positive in terms of activity for 2026, but, again, no significant rise in demand is expected, mainly due to the economic and financial issues persisting in the country.

In the flats segment, which is mostly healthier than the longs segment at least for exports, with the estimated figures for November and December the total production and consumption figures are expected to decrease for 2025 by around three percent, while exports are projected to show an increase of 15 percent, mainly due to shipments to the main partner of Turkey in terms of HRC trade, namely, Europe.

Turkey’s flats production, consumption and exports

According to SteelOrbis Research’s calculations, the general average capacity utilization rate for slab production in Turkey in 2025 stood at 72 percent, while the market sources estimate the average utilization rate for EAF slabs at around 75-80 percent. Overall, the potential for a better export performance in the flats segment, particularly in HRC, is higher compared to longs, considering the theoretical advantage in Europe in view of CBAM with Turkey having over half of its local production based on EAF-based scrap usage along with geographical proximity. Considering that the import availability of steel slab will remain limited in 2026, the room to increase domestic slab production may be supported by a potential increase in flats exports, but not in terms of unused EAF-based steel slab production capacities in Turkey.

A lot of questions exist in terms of the CBAM mechanism as regards tracking the origin of the semi-finished products used for finished products to be exported to Europe. Theoretically, Turkey can manage combining local EAF-based production and mostly BF-based semis imports in the framework of its current inward processing regime. However, much will depend on how CBAM costs will be calculated at the end of the year. Overall, cautiously optimistic market players believe that Turkey’s own steel slab production will be utilized within a range of 70-80 percent in 2026 or slightly higher, while billet production might be limited to an increase to 60-65 percent. As a result, steel scrap imports to Turkey might return to or even exceed the 20 million mt mark seen back in 2024. Still, a lot of uncertainty will be seen in the steel market in 2026, which could change the general forecasts.