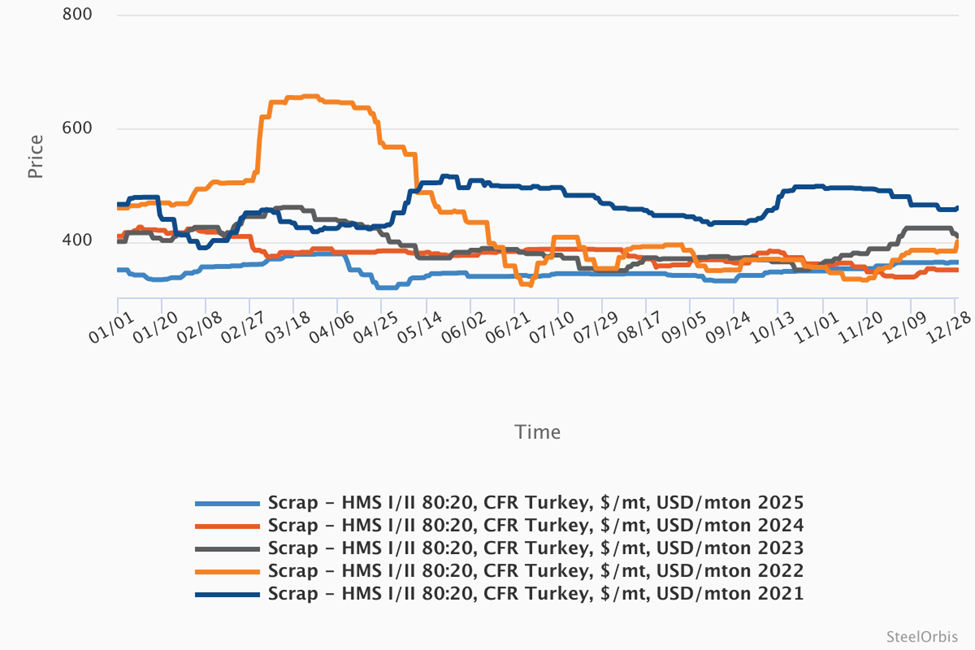

In 2025, Turkey’s import scrap prices fell to their lowest levels since 2021. Turkey struggled during the year having lost most of its steel export markets and also given its underperforming local steel demand, rapid changes in the international trading environment and unexpected financial changes. In addition, attractive billet prices especially in the first half of 2025 negatively impacted Turkish mills’ appetite for scrap. They had leverage to exert pressure on scrap prices during most of 2025 and managed to keep scrap prices in a relatively narrow range for more than 20 weeks. Only when scrap availability and collection costs forced their hands did deep sea scrap prices move up and give suppliers some room to negotiate.

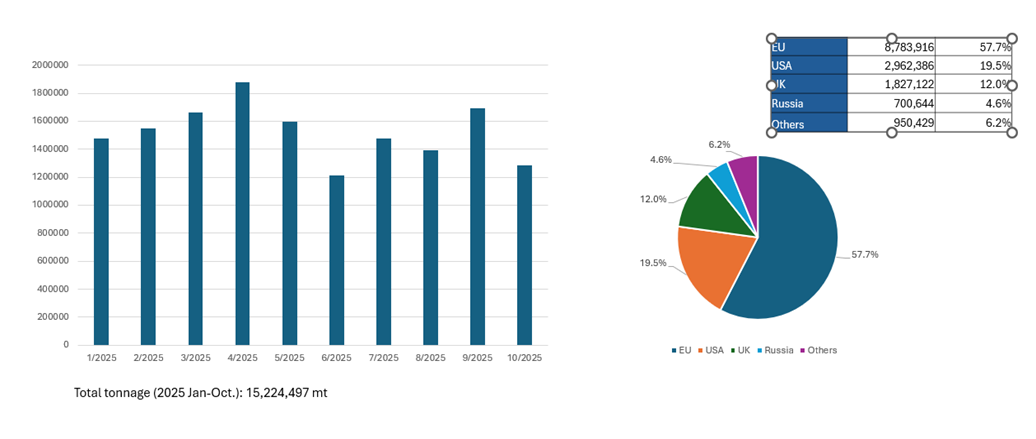

Turkey’s main scrap supplier regions did not change much during the year. While the EU was the biggest supplier in 2025, with its total tonnage reaching 8.7 million mt and with a 57.7 percent share, US suppliers came second with 2.9 million mt and a 19.5 percent share.

Examined country by country, the US came in first place, followed by the Netherlands and the UK, respectively, with 2.2 million mt and 1.8 million mt of scrap exports to Turkey. According to the TCUD data, Turkey’s scrap imports from the US and the EU declined in the first ten months of the year, though Turkish mills decided to buy more from the CIS region and the UK as compared to 2024.

Highlights of 2025

The Turkish steel and scrap markets made a reluctant start to 2025. Turkish mills were trying to lower scrap prices and were briefly successful. However, the first price increase was observed at the end of January due to seasonal expectations and lively demand from Turkey. The fundamentals of the international scrap market were signaling a positive price trend as scrap availability remained on the low side, collection prices were moving up at export yards, and domestic scrap demand in the supplier regions was gaining pace with spring approaching.

At the beginning of February, the main topic in the markets was the US tariffs. US President Trump slapped tariffs on Canada, Mexico and China at 25 percent, 25 percent and 10 percent, respectively. “The extraordinary threat posed by illegal aliens and drugs, including deadly fentanyl, constitutes a national emergency under the International Emergency Economic Powers Act (IEEPA),” Trump stated. The US dollar showed record strength against the Chinese yuan, while the Canadian dollar depreciated to its lowest level against the US currency since 2003. Trump also said he planned to announce tariffs for the European Union in the future. The global markets were impacted by these developments and were being monitored closely by Turkish players. However, Trump then decided to postpone the announced additional 25 percent tariffs on imports from Canada and Mexico. Turkish steel mills did not dwell on this issue much in terms of trading initially. Turkey has largely been out of the US market since 2018 after the US initiated Section 232 tariffs against Turkish steel. However, the positive mood observed in the US markets was closely monitored by Turkish market players as it was expected to have an impact on ex-US scrap prices. The total increase in import scrap prices in February was $15/mt.

In March, Turkey’s import scrap purchase prices increased by 5.28 percent, continuing the upward trend which started in the fourth week of the year, and rising by a total of $42.25/mt since then. At the start of March, Turkey’s import scrap market was expected to increase further during the month as international sentiments remained strong against the backdrop of the US tariffs against its two biggest trading partners, the EU announcing funds for defense and infrastructure, and hopes for an end to the Russia-Ukraine war. Meanwhile, the depreciation of the euro supported upward expectations, causing an additional $13/mt increase in costs. The low scrap availability from the EU and the US was a significant factor supporting the uptrend of scrap prices in March.

However, sentiments in the Turkish market changed very quickly on March 19. Trading in the Turkish steel and scrap markets almost came to a halt given the sudden sharp depreciation of the Turkish lira against the US dollar following the detention of Istanbul mayor Ekrem Imamoğlu on March 19. The sharp volatility of the Turkish lira-US dollar exchange rate created great uncertainty in the market. Trading at Istanbul’s stock exchange was closed twice in one hour as circuit breakers stepped in, Bloomberg reported. Turkey’s treasury and finance minister Mehmet Şimşek made an announcement assuring the markets that the government was doing everything to make sure the markets continued operating in a healthy manner. Following the political developments in Turkey which started on March 19, players in the Turkish steel and scrap markets started to evaluate the economic impact of these events.

In April, Turkey’s import scrap prices declined by 15.9 percent, far exceeding the 5.28 percent upward movement recorded in March. The fall from $378.75/mt CFR at the start of April was a rapid one. Sentiment was pessimistic when April started amid increased global protectionism and the ongoing political turmoil in Turkey. The sharp decline in the local US scrap market, initially viewed as a domestic phenomenon by exporters, created downward pressure on ex-US scrap quotations starting in the second week of April. While the European market managed to remain positive in the first week of April, its resistance was broken due to the significant downward pressure observed on the export side. Amid Turkish mills’ sustained indifference to the offers shared by scrap suppliers and due to their continuous lowering of bids, scrap exporters realized they had high tonnages in their yards with almost no buyers. Turkish mills drew attention to the more attractive levels of billet prices as well as the silence observed in their steel sales departments. Though some believed that the continued decline in billet prices was triggered by high production in March and early April and the lack of strength of local Turkish demand, the main factor - an unexpected one - remained the global trade war, with the US and China slapping huge tariffs on each other. Turkey’s domestic steel market continued to underperform during April, providing no support for any increases in scrap prices.

The political turmoil in Turkey that started on March 19 also took its toll on the steel sector. The downward trend in the reserves of Turkey’s central bank observed after March 19 continued with each passing week. According to the data from the central bank, gross reserves fell to $141 billion in the week ending April 25. In the previous week, gross reserves had stood at $146.6 billion. Net reserves dropped from $38.6 billion to $35 billion. The downward trend in net reserves, excluding swaps, also continued after March 19. In the week ending April 25, net reserves excluding swaps decreased from $20.4 billion to $16.4 billion. This marked the lowest level of net reserves excluding swaps since June 2024. With high loan interest rates exacerbating the situation, the recovery anticipated in the construction industry was now considered by Turkish steel mills to be unlikely.

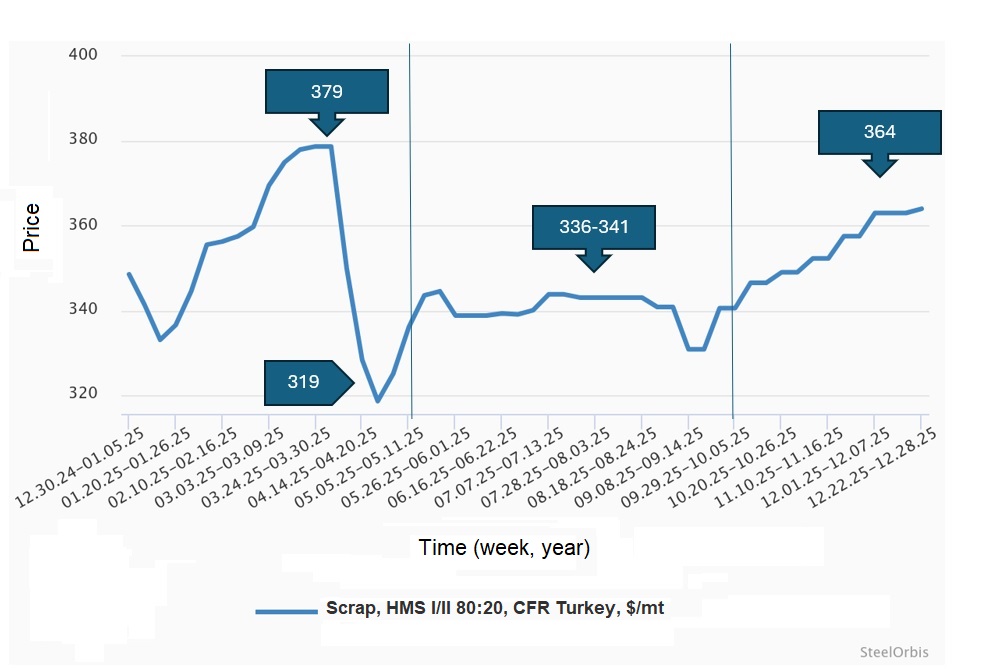

As can be seen in the graph above, after hitting an annual low of $319/mt CFR on average, Turkey’s import scrap market managed to gain some upward ground in May. Scrap flow to export yards was slow in the EU, while the collection costs of exporters were moving up gradually to secure the tonnages they needed. But the problem in Turkey’s steel segment still existed. As Turkish mills were trying to increase their rebar sales prices, they were failing to receive orders for high tonnages. In subsequent weeks, the fluctuations seen in Turkey’s import scrap market were completely the result of the dynamics of scrap availability and steel sales, as well as being due to the cheaper billets arriving in Turkey. For more than 20 weeks, Turkey’s import scrap prices remained in the range of $336-341/mt CFR.

In June, Trump announced a doubling of tariffs on steel and aluminium to 50 percent. The US-China tariff negotiations were ongoing and everyone was waiting to see the outcome, though with little hope. Trump announced on June 11 that a deal had been done. The relationship between the world’s two largest economies is “excellent”, Trump said in a post on Truth Social, adding in block capitals, “We are getting a total of 55% tariffs, China is getting 10%.” Another significant factor in June was the Israel-Iran war which continued for 12 days during June 13-24. In the second half of June, sentiment in Turkey’s import scrap market was showing signs of a recovery. Trade in the local rebar market was accelerating and Turkish mills were increasing their prices a little, testing the waters. But the positive mood disappeared quickly due to the escalating military conflict between Israel and Iran. The war in the Middle East had a negative impact on Turkey’s steel and scrap markets, curbing the upward expectations for scrap prices. Very early in July, Turkey’s Petroleum Pipeline Corporation (BOTAŞ) announced, in line with its 2025 budget targets, an increase in wholesale natural gas prices effective as of July 2. Natural gas prices for industrial users were raised by an average of 7.86 percent. Having struggled to increase their rebar sales prices for weeks, Turkish mills started evaluating how they could pass on this cost increase to their customers. Even scrap suppliers pointed to the obstacles Turkish mills were facing locally and in their export markets. As August started, Turkish mills were unwilling to conclude deals at the higher end of the price range, citing decreasing profit margins, low steel sales and empty order books, while pointing to the lack of any recovery in steel demand on the horizon. A similar situation was seen globally, not just in Turkey. While the first scrap deals in August were closed at $340-346/mt CFR and remained in this range for most of the month, the pace of trading was already slow. At the end of the month, scrap suppliers decided that it was time to cut their losses. Some of them were forced to accept lower price levels due to their need for cash, some due to their high inventory levels, and others due to their contracts with ports, market sources reported.

Early in September, Turkish mills showed significant resistance to deep sea scrap prices in the range of $337-344/mt CFR. Their bids were significantly lower, exerting pressure on suppliers, whose inventory levels were high, while the high number of offers shared with Turkish mills also strengthened the position of the latter. On September 11, SteelOrbis reported that the usual correlation between ex-EU and ex-US scrap prices had been disrupted. This new dynamic was raising questions amongst market players, who observed the same disruption of the usual correlation between short sea and deep sea scrap prices. Market sources reported that the decision of a major Marmara-based Turkish mill to cut its capacity utilization rate had created a void in the market, giving more leverage to alternative buyers. In the middle of the month, the soft trend of import scrap prices was still observed but it had lost significant momentum. On September 15, there was an expectation that the bottom would be reached. On September 25, deep sea scrap prices recorded their anticipated recovery, starting the uptrend that lasted until the end of 2025.

When October started, US sellers were not inclined to accept lower export price levels, citing their struggle to collect HMS grades from their local market. The livelier demand in the local US market for HMS grades was the result of stronger domestic rebar demand after the imposition of import tariffs. On the other hand, a high number of Turkish mills were in the market looking for scrap, supporting expectations of higher deal prices in the next round of bookings. A question asked in the international scrap markets was why the Turkish mills accepted increases in import scrap prices when domestic scrap prices in the supplier regions were declining. In the US, the lack of available sea vessels was creating a problem for sellers and increasing their freight costs. Still, after the price cuts expected in the local US market, US-based scrap buyers’ purchase prices were more attractive than the purchase prices of export yards. In the EU, even with local steel producers cutting their scrap purchase prices, their price levels were in line with or slightly higher than exporters’ purchase prices. As a result, the declines in domestic scrap prices in the supplier regions did not have any direct impact on scrap exports. The average HMS I/II 80:20 scrap price to Turkey was at $340.5/mt CFR when October started and reached $346.5/mt CFR in the second week of the month. On October 15, Turkey’s import scrap market saw increased price levels for ex-US cargoes, more in line with the expectations voiced earlier in the month. “It will depend on freight costs though,” a European scrap supplier said, adding, “The new tension between the US and China about ocean transport is not helping either.” The demand received from Turkish mills increased, while the number of available offers in the market had not changed much. On October 21, it was observed that Turkey had almost finished its deep sea scrap purchases for November shipment, with the average price level settling at $349/mt CFR for benchmark HMS I/II 80:20 scrap.

As SteelOrbis anticipated, Turkey’s import scrap market was a seller’s market at the start of November, with buyers actively seeking scrap cargoes for December shipment, while sellers were in no rush to meet this demand due to their expectations of higher prices. Despite having concluded a high number of deals for scrap cargoes for November shipment, Turkish mills had been working with very strict scrap inventory management in past months. As SteelOrbis mentioned previously, their demand for scrap was very sensitive to external factors. Acceleration of steel demand, slowness in scrap generation or fluctuations in sea vessel freight rates could influence their purchasing strategies. This last minute demand received from Turkey continued through December, despite Turkish mills’ efforts to curb the uptrend, deep sea scrap quotations closed the year at $364/mt CFR on average.

Conclusion

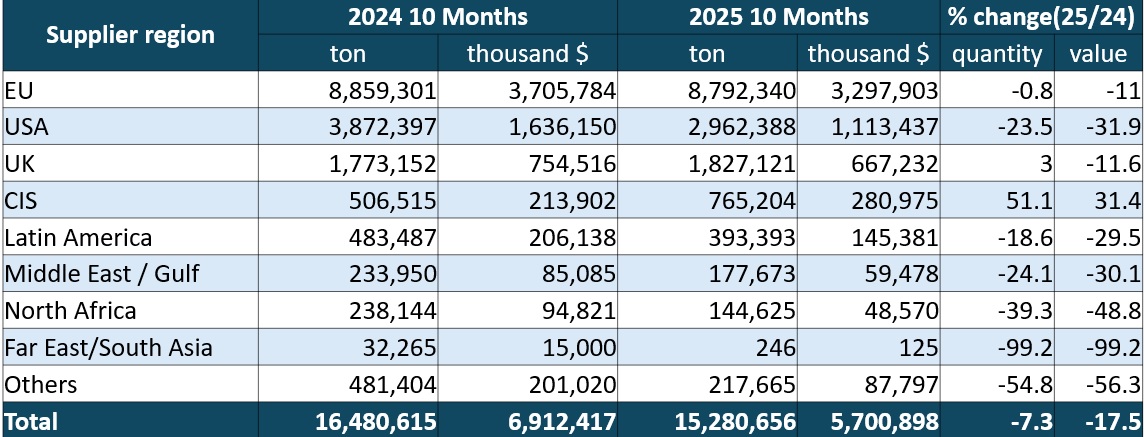

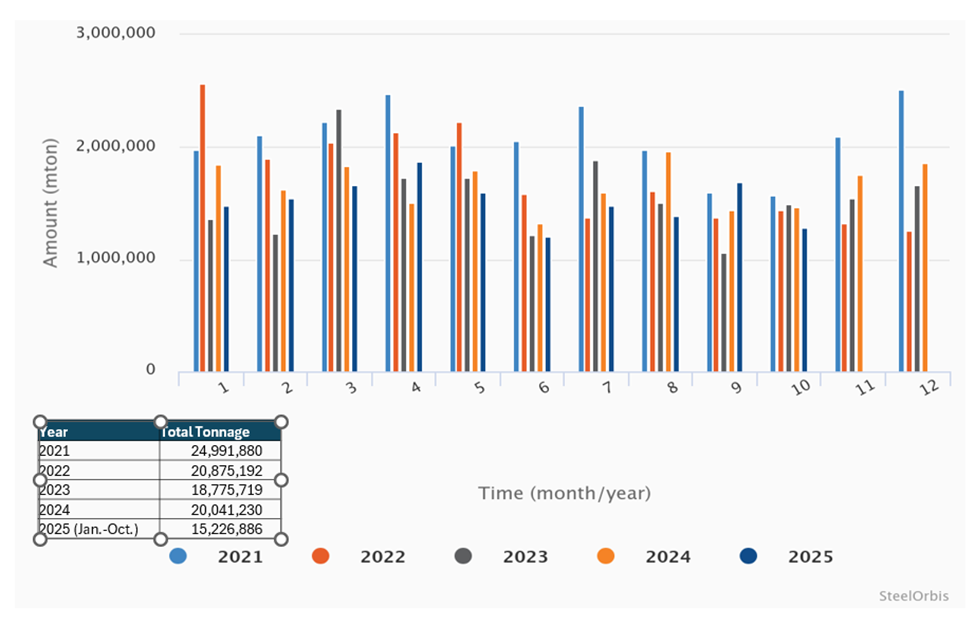

Turkey’s import scrap volume in the first ten months of 2025 reached 15.2 million mt and is expected to exceed 18.2 million mt for the full year. This tonnage is lower than the previous years, though import activity at the end of 2025 was lively, which could push the final volume closer to 20 million mt.

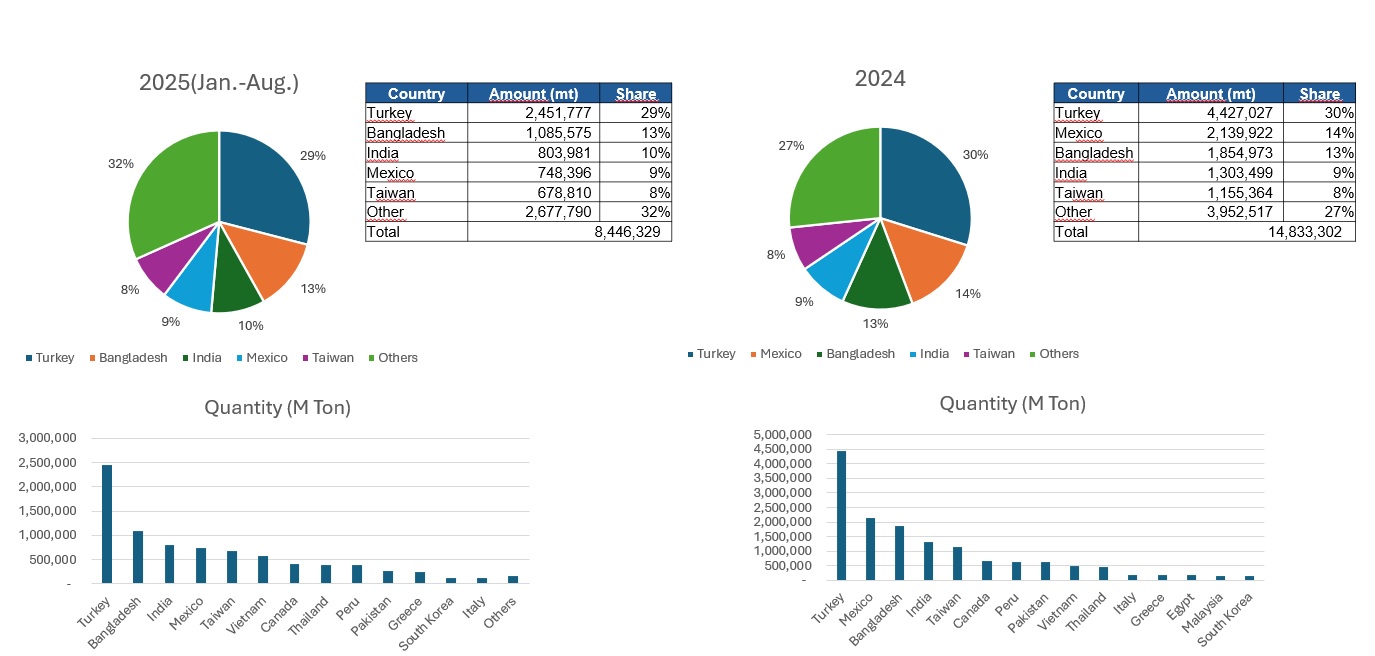

Compared to 2024, Turkey’s share in US origin scrap exports has not changed much, despite the decline seen in the total tonnage.

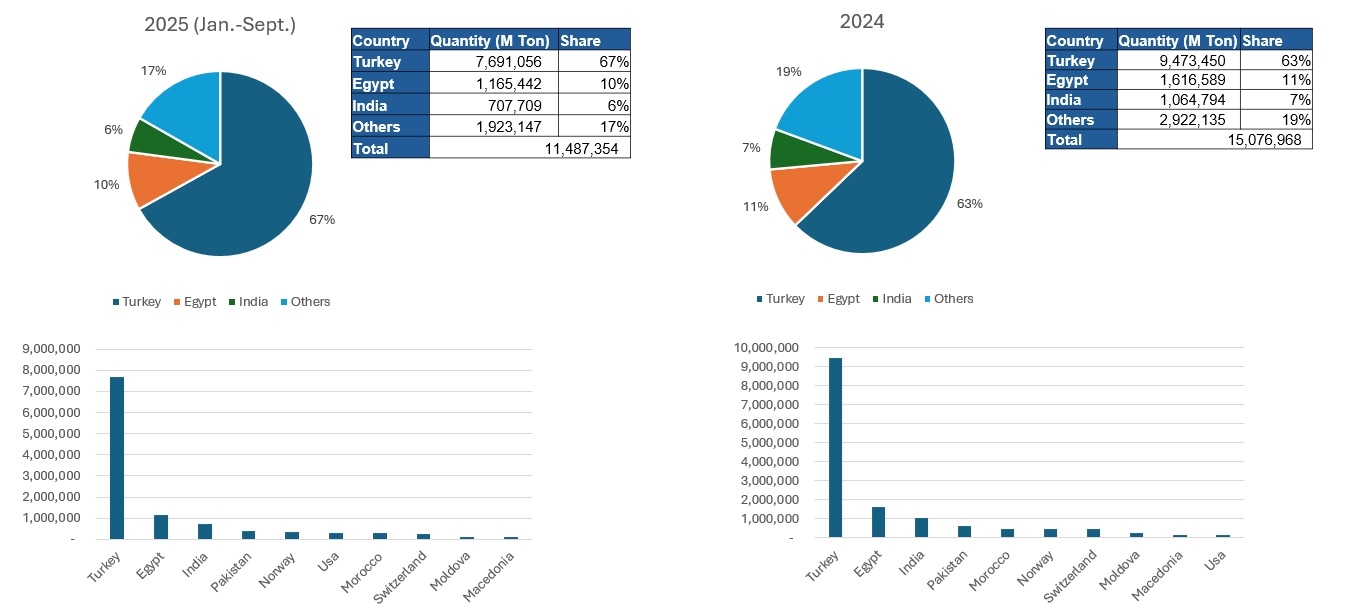

On the other hand, for EU-based suppliers Turkey has become a more attractive market, increasing its share of ex-EU scrap exports from last year’s 63 percent to 67 percent in the first ten months of 2025.

As the year ends, the mood in Turkey’s import scrap market is positive. The dynamics in the supplier regions are signaling a firm stance on scrap prices for Turkey. Low availability is pushing suppliers to accept higher collection costs, which will be reflected in prices to Turkey. The local US scrap market is expected to move up in the January buy-cycle, while EU-based suppliers have mentioned risks relating to the exchange rate and slow scrap generation. Meanwhile, Turkish mills do not expect any significant recovery in their steel sales over the winter months. Any upward movement may remain limited while Turkish mills try to prevent prices from moving up as they start seeking cargoes for February shipment.