The Russian metallurgical industry is entering 2026 in a structural crisis, seeing an annual decline in production and a considerable weakening of local consumption. Along with the clear reasons for the deterioration, given the internation sanctions imposed after Russia’s full-scale military invasion of Ukraine, the resulting financial and economic issues have deepened in the past year, thus significantly bringing down demand. Export activity has also remained subdued, again due to sanctions-related limitations in some markets, price pressure from most buyers due to risks, and competition with China. In the meantime, the share of steel imports arriving in Russia has been rising, thus making the imbalance in the local market even more profound. Moreover, despite the optimistic announcements and targets of the Russian government, the steel industry outlook for 2026 is rather gloomy due to the harsh economic and monetary policy of the government, influencing the mills’ production, cash flows and investments, as well as the situation in the main consuming industries in Russia.

Steel market imbalance deepens in Russia amid falling output, limited export presence and revenues, rising imports

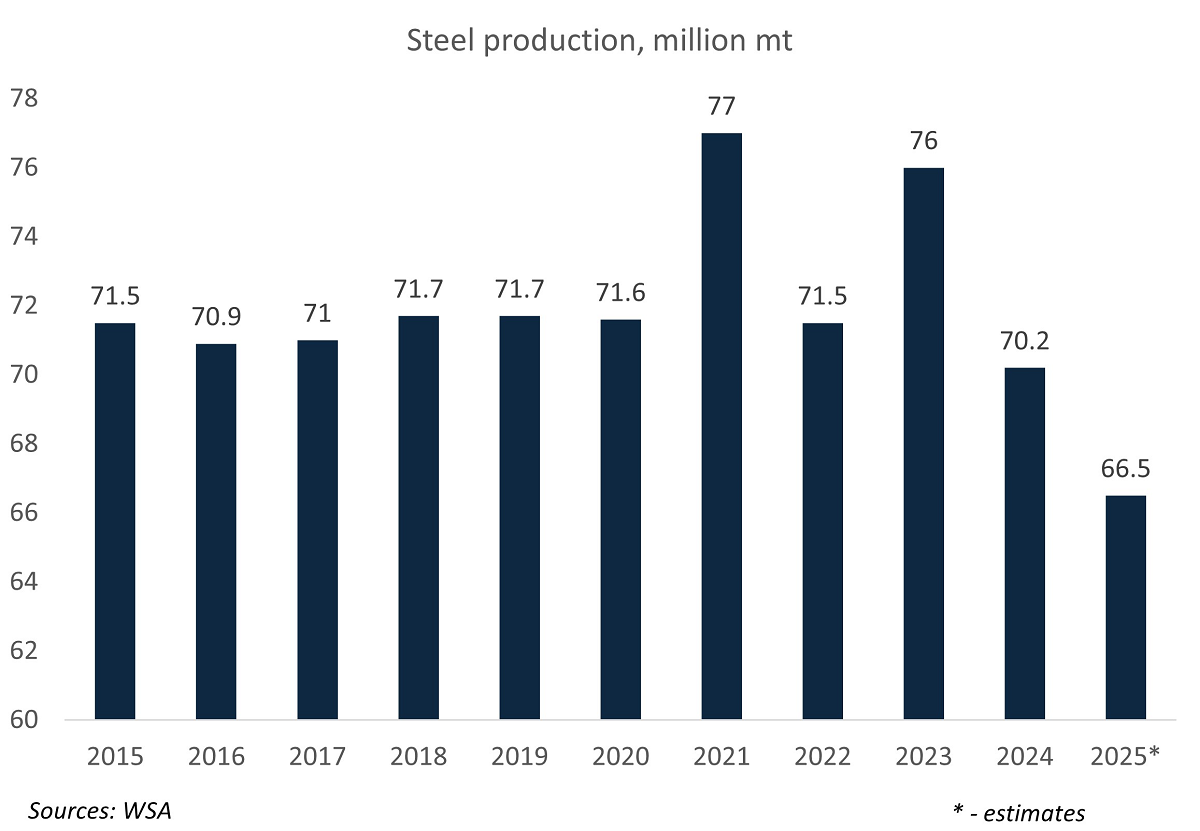

According to local sources, in the January-November period of 2025 Russian crude steel production dropped by 5.1 percent to 61.5 million mt, while the output for the full year is expected to be around 66.5 million mt. Finished steel production is foreseen to post a drop to 58 million mt, down from 61 million mt in 2024.

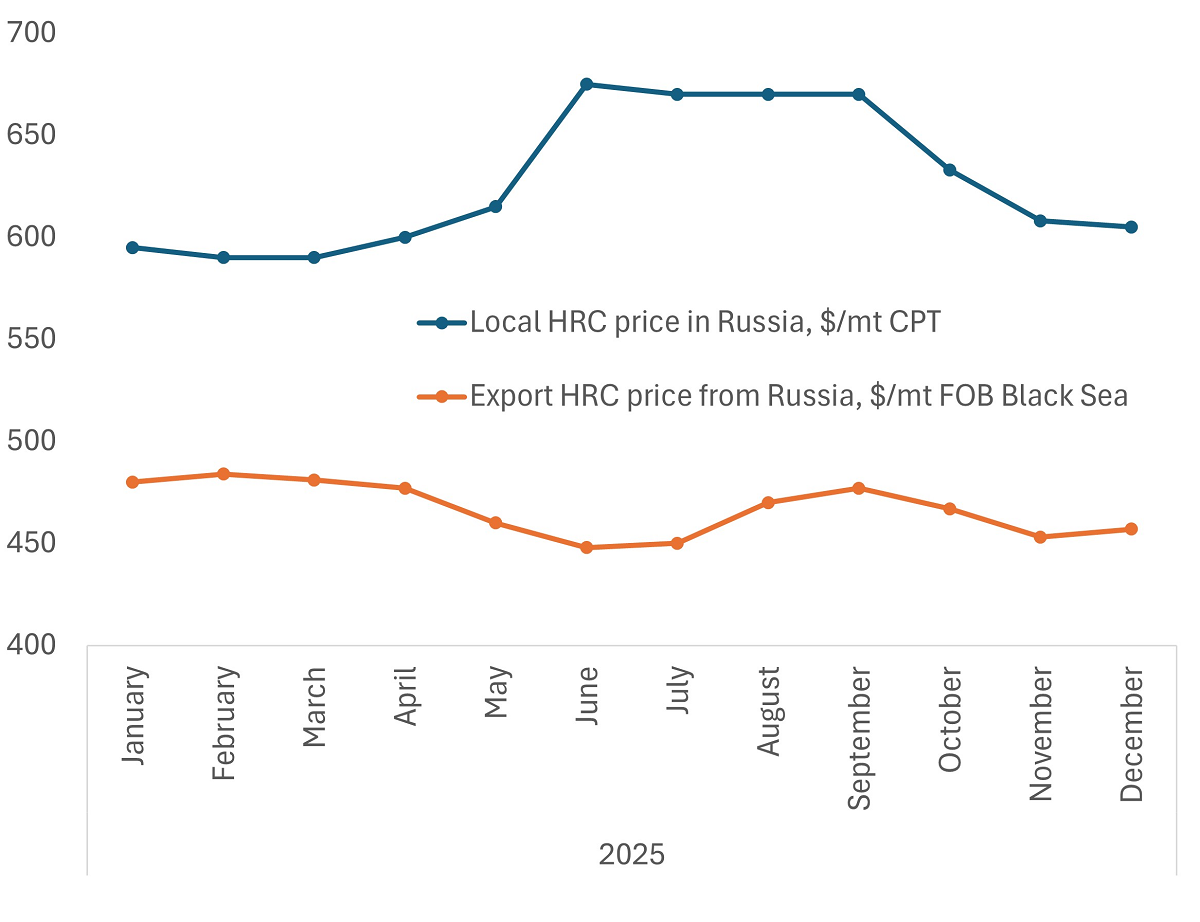

In the meantime, steel exports, which stood at 20 million mt in 2024, were first projected to fall by another 2.5 percent since Russia’s presence in overseas markets is significantly limited due to sanctions - with no chance for sales by most Russian steel producers to destinations like the EU and the US and with significant pressure in regions like MENA due to risks and competition with China. Still, some believe that Russia’s exports in 2025 could show a four million mt increase due to the abolition of the export tax on finished steel. The low revenues from the steel export trade are another issue for Russian mills, since the workable prices are affected by various global factors, unlike the domestic market in Russia. Therefore, in some periods of 2025, export sales prices specifically for Russian hot rolled steel fell $150-200/mt below the domestic price levels.

In addition, increasing steel imports intensify pressure on Russian mills, since they claim more and more of the already declining domestic consumption. The main volumes are coming from China, with the share of import steel in Russia reaching almost 10 percent in the third quarter (with China accounting for almost 25 percent of this), local expert sources state. “The ruble became firmer … the trade balance becomes more tense, and it has an impact … Our export opportunities are shrinking and our competitiveness in the local market is declining. We are seriously seeing the appearance of foreign goods in large volumes and the strong competition with imports of course raises the question about local market protection,” Alexey Mordashev, a key shareholder of Severstal, said in an official statement. However, despite mills’ intentions to push for an excise tax on imported steel goods, no government movement towards trade restrictions of imports or investigations have been reported.

Tight monetary policy and sanctions push local steel usage in Russia to 11-year low

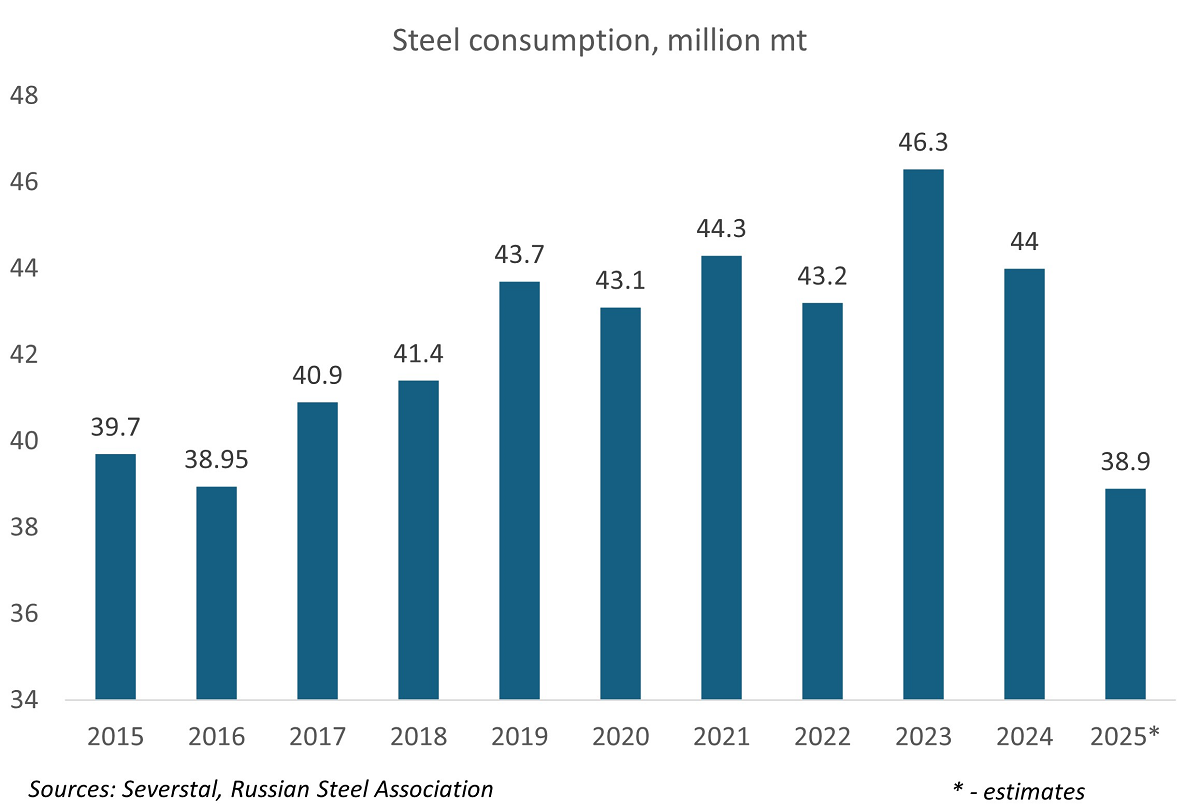

Russia’s total steel consumption is projected to drop by 14 percent in 2025 to 38.9 million mt, falling to the lowest level in the last 11 years.

In fact, the Russian Steel Association expects a considerable contraction in most of the steel consuming industries in Russia in 2025, with the deepest crises seen in automotive production (-36.4 percent) and heavy machinery (-30 percent). The construction and metallurgical trade sectors are expected to show declines of around 10-10.5 percent, while steel consumption in the energy sector is expected to drop by 19.4 percent due to low prices for hydrocarbons and the pressure from sanctions, according to the association’s data. “When the first sanctions [against Russia] were introduced in 2022, the effect was predicted to be seen within three years and this has happened. The steel industry is a good example of that,” an analytical source said in his report.

In the local Russian market, the main negative effect on steel demand came from the real estate sector cooling down, while construction accounts for almost 80 percent of total steel consumption in Russia. According to experts, the sales of new houses may drop by 19-35 percent in 2025 compared to 2023, which means the loss of over RUB 3 trillion (around $25 billion). The crisis in the real estate sector has been fueled by high interest rates, the drop of real incomes and certain limitations in the financing of projects. The increase in prices for building materials leads to higher construction costs, while at the same time the demand for houses drops due to monetary policies and the overall high degree of uncertainty.

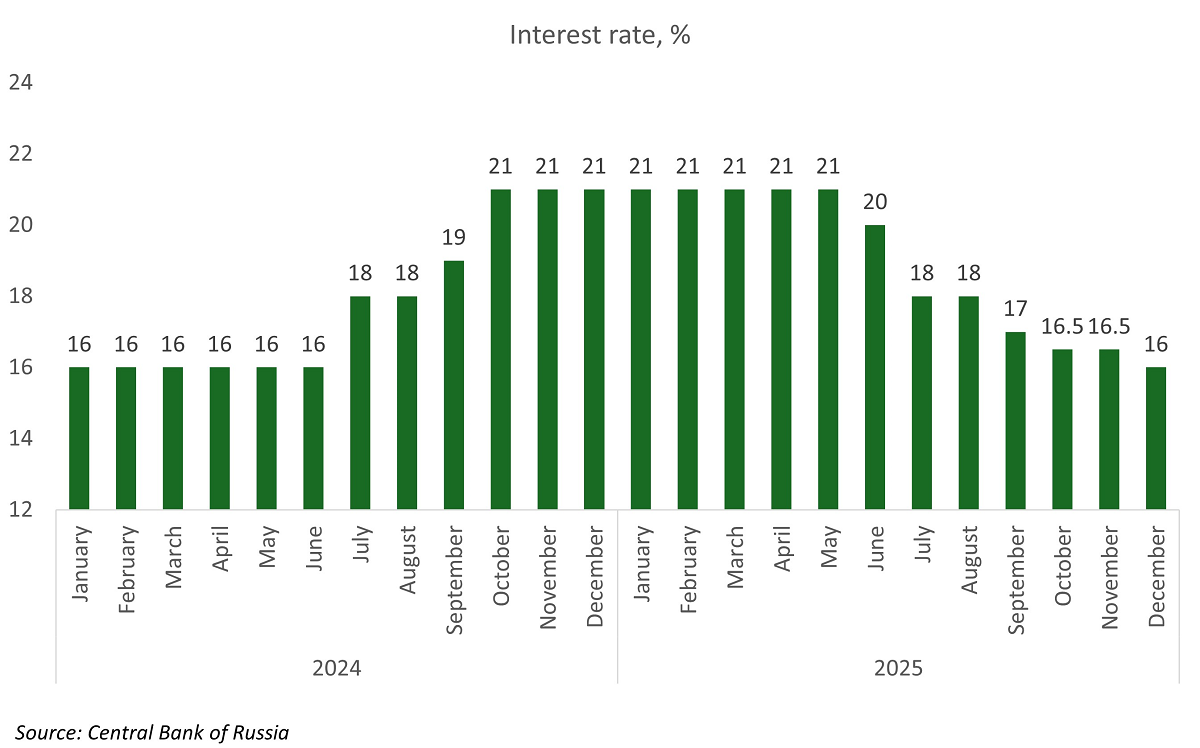

Interest rates in Russia stood at 20-21 percent in January-June 2025 and, starting from August dropped first to 18 percent, and then gradually to 16 percent at the end of December of the same year. “The [interest] rates were too high during most of the year and the decline to 16-17 percent does not help when the industry is already this much imbalanced. Things might get better and start moving if we see a 14-15 percent interest rate, but at the same time we have the VAT increase [from 20 to 22 percent] which will bring up the prices for steel as well as for logistics,” a Russian source told SteelOrbis.

Excise tax on steel contributes strongly to falling revenues of Russian mills

Back in 2022, the Russian government introduced the excise tax of 2.7 percent on the average monthly export price for BF-based steel slab on FOB port basis in the southern part of the country as a means to get additional budget money. From August 2022, the tax was to be zeroed if the price went below RUB 30,000/mt, which allowed mills to save money, while the budget lost around RUB 29 billion, local Russian media stated.

Starting from 2023, the local steel market lobby has been trying to convince the government to increase the threshold price to RUB 60,000/mt, with following annual indexation. The government, however, has been strong in its opposition and is not willing to lose tax revenues, which were planned in 2025 at RUB 47.4 billion ($0.6 billion). According to the budget projections for 2026 and 2027, the amounts to be received are at RUB 51.6 billion and RUB 50.9 billion, which is around $0.63-0.64 billion. According to the latest developments, while the steel industry asks for a threshold increase to RUB 54,000/mt, the government remains unconvinced and only some consent for payment delays was provided. One of the arguments is that EAF-based mills are paying much lower amounts of excise tax, since their formula is different with 0.3 percent from the difference between FOB South Russia billet price, the scrap price in Ural Federal District and half of the spending on ferroalloy purchases. As a result, the planned tax revenues from EAF mills in Russia totaled RUB 6.5 million in 2025, with a gradual decline projected for the next two years, official data indicate.

Coupled with the tough monetary policy and its results on mills’ cash flows, domestic steel consumption, pressurized exports and low investment returns, the excise tax on steel in Russia is expected to contribute considerably to mills’ declining financial performances. In particular, the net profit of Severstal is expected to drop by 30 percent, that of MMK by 15 percent, while NLMK, being the only non-sanctioned steel producer in Russia, is foreseen to record a drop of only four percent in its net profit. The declining net profits of even the strongest mills, whereas the rate of 15 percent profitability is required for effective operations, is considered an alarming development. “A balance is possible only with flexible taxation, with the market prices to be considered, but for now the advantage is on the side of the Ministry of Finance due to the budget deficit,” Dmitriy Vishnevskiy, a market analyst, commented to the Russian media outlet Kommersant.

Outlook for Russian steel sector in 2026 remains gloomy, crisis likely to deepen

Despite the Russian government’s projections for local steel production and consumption to recover in 2026 to 69 million mt and 40.5 million mt, up 3.7 and 4.1 percent, respectively, most market players are less optimistic for developments in 2026. The profitability of export sales, which is largely defined by price competition with China in the Turkish and MENA markets, will remain low at least in the first half of the year, while the pressure from sanctions will still have an impact on steel and raw material exports from Russia, as well as on the development of certain steel consuming industries in the country.

The excise tax on steel, which is being fought over by the mills and the government, is another issue pushing down the sector’s profitability. “It [the tax] was introduced when the foreign markets were more open and domestic consumption was increasing. Today, the situation for all Russian mills is very uneasy and their existence is under question. Any additional financial burden may become the last drop at any moment,” a RUSLOM representative said in an official statement. “The heavy hand of monetary policy has weakened only nominally. For now, we are going toward a situation when we might face stoppages of production at some steel producers who have issues with costs. The sector’s competitiveness will drop and mills will exist with limited domestic demand,” another expert said.

The reversal of the downturn in steel consumption is also not considered possible without governmental support in terms of certain real estate preferential programs, support of construction investments, as well as without a further decrease in interest rate. Others believe that in case of a further decrease in interest rates a certain revival of end-user demand might be triggered, while the Russian government, along with a possible weakening of the ruble, might consider that all of the above may offset the potential loss of gains from the steel excise tax. In addition, the potential decrease of interest rates may trigger subsidiary investment programs in the retail sector. A certain increase is expected in the logistics sector, but it represents a relatively small volume of steel consumption.

However, it is mostly believed that a limited steel consumption revival is possible at the earliest in the second half of 2026, but in the basic scenario a market rebound is possible only in 2027. Experts see the potential in industrial and logistic projects, in the energy, oil and gas sectors, as well in certain parts of the machinery sectors. However, the recent decision of the Russian government regarding additional capitalization of the Industry Development Fund by only RUB 1.8 billion versus much greater requirements shows that the money and governmental support are absent in view of the planned budget deficit for 2026 at 1.6 percent of GDP, SteelOrbis has learned.

The head of the Russian union of industrial entrepreneurs, Alexandr Shohin, stated that by the end of 2026 “business would like to see an interest rate of 12 percent with 4-5 percent inflation and the US dollar/ruble exchange rate at RUB 90-95. A lot of uncertainties will prevail in the Russian economy for the 2026-27 period, but most experts agree that, while Russia’s military aggression against Ukraine continues and the international sanctions remain in place or are even increased, the Russian economy will remain under considerable pressure with direct effects on domestic consumption and the steel industry overall.