Russia’s military invasion of Ukraine has triggered a lot of issues globally and, particularly, effected the energy balances in several regions, given that Russia had been one of the world’s major hydro-carbon exporters.

Particularly, in 2022 the energy crisis hit EU countries and their steel sectors, and affected the costs, production rates, competitiveness and margins in business. By the end of the year and in early 2023, the situation eased somewhat due to government policies in the EU to reduce dependency on Russian energy and also owing to favorable weather conditions, which enabled household energy consumption to remain at acceptable levels.

The high energy prices which the EU countries had to implement in 2022 rewrote the structure of the European steel industry. Gas supply issues resulted in energy prices spiking, so steel producers were forced to increase steel prices while facing higher costs or to cut their output. The situation resulted in some production cuts since some European mills chose to suspend operations at some of their facilities or to reduce utilization rates significantly starting from August and during the autumn months of 2022.

List of main European mill with idled or reduced capacity in H2 2022

Country |

Company name |

Facilities |

Idled or reduced capacity, million mt |

Germany |

ArcelorMittal Hamburg |

EAF |

1.1 million mt |

Germany |

ArcelorMittal Bremen |

BF |

1.98 million mt |

Germany |

ArcelorMittal Duisburg |

BF |

6.8 million mt |

Germany |

Salzgitter |

BF |

1.6 million mt |

Germany |

ArcelorMittal Eisenhuttenstandt |

BF |

2.34 million mt |

Germany |

Total |

13.82 million mt |

|

Italy |

Arvedi |

EAF |

3.85 million mt |

Italy |

Arvedi |

EAF |

0.73 million mt |

Italy |

Acciaierie d'Italia |

BF |

4.8 million mt |

Italy |

Total |

9.38 million mt |

|

Spain |

ArcelorMittal Gijon |

BF |

2.24 million mt |

Spain |

ArcelorMittal Sestao |

EAF |

2 million mt |

Spain |

Total |

4.24 million mt |

|

France |

ArcelorMittal Dunkirk |

BF |

4.5 million mt |

Poland |

ArcelorMittal (Warsaw) |

EAF |

0.75 million mt |

Poland |

ArcelorMittal (Dabrowa Gornicza) |

BF |

2.25 million mt |

Poland |

Total |

3 million mt |

|

Slovakia |

USS Kosice |

BF |

1.42 million mt |

Czech Republic |

Liberty (Ostrava) |

BF |

1.06 million mt |

Integrated coil producers, mainly in Italy, started purchasing imported slabs from China, India, Indonesia, South Korea, Vietnam and Brazil in order to replace the missing semis volumes from Ukraine and Russia. In fact, while Ukraine has hardly been present in the slab market since the war started, some Russian mills have still had the chance to sell to the EU based on EU regulations. Along with the target to substitute the regular missing imported tonnages, some mills in the region were buying slabs, aiming to get better margins from slab rolling compared to own slab production.

During 2022, European electricity and natural gas prices for industry increased by two- or three-fold. The highest average monthly wholesale electricity price in the EU was recorded in August 2022 at €543/MWh. It was caused by a rise in gas prices, which prompted European politicians to consider intervening in the energy market to protect consumers and businesses.

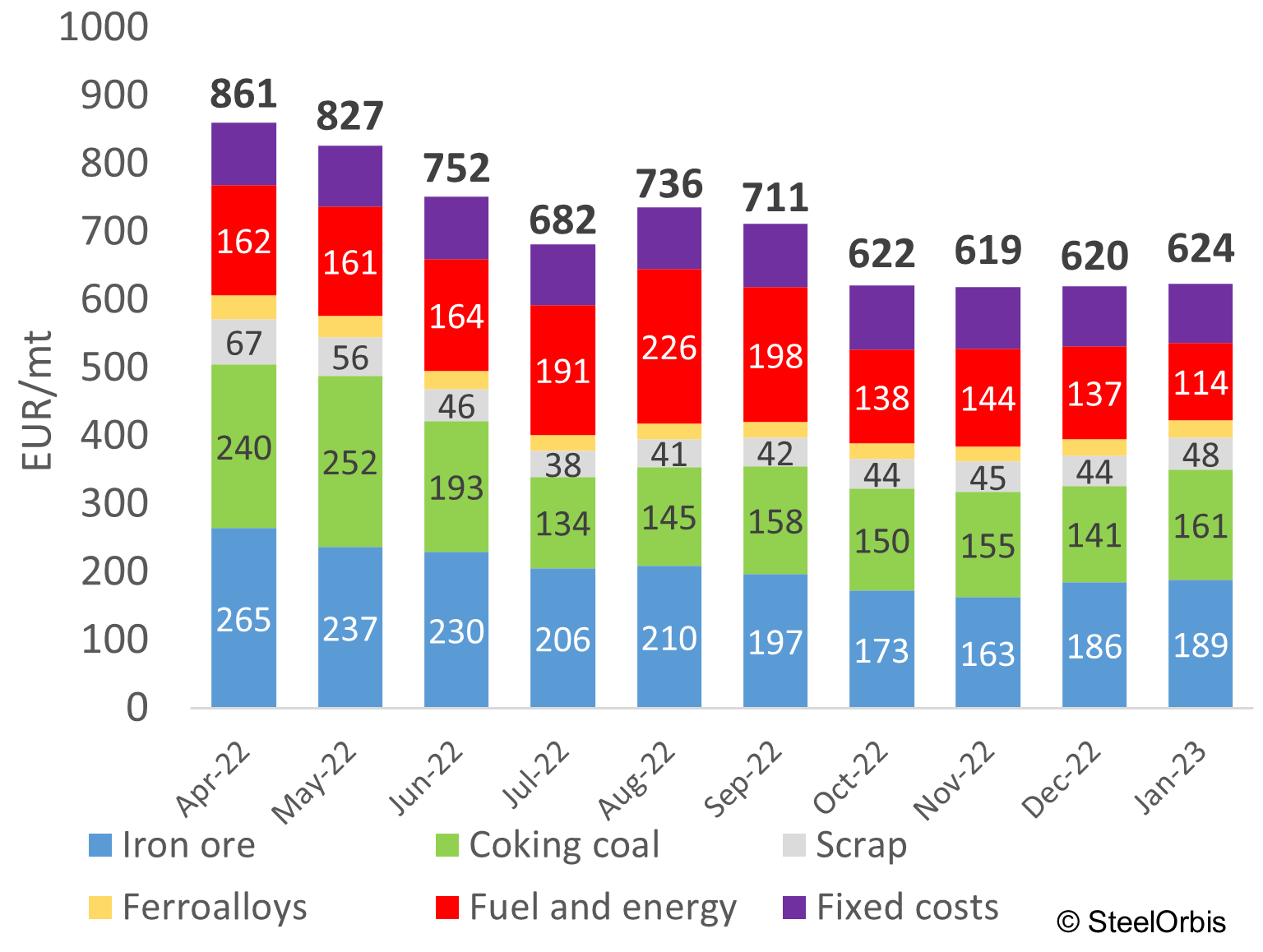

Before the electricity and natural gas prices increased in 2022, the share of energy in steel production costs was 10-18 percent for BOF steel and 9-16 percent for EAF steel, SteelOrbis estimates. In the third quarter of 2022, the share of energy costs in the European steel sector’s cost increased to 25-40 percent against the backdrop of natural gas and electricity prices rising.

Italian HRC (BOF steel) production cost structure

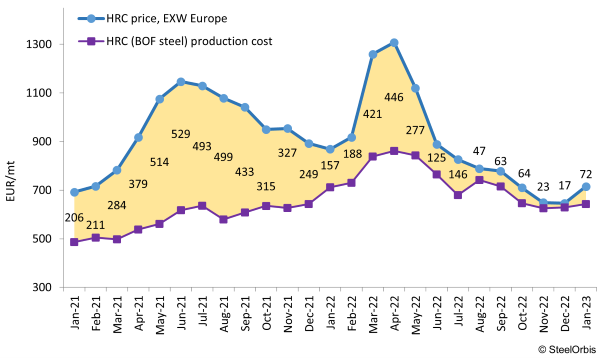

In the second half of 2022 the higher increases in steel product costs due to energy prices cut the profit margins from steel products by several times over. The Italian HRC margin (from BOF steel) decreased to €25-100/mt (from €110-440/mt in the first half of 2022 depending on the month). The profitability of German HRC made from iron ore (from BOF steel) while selling in the domestic market decreased to €20-150/mt, against €130-457/mt during the first two quarters. The margin per metric ton of Poland BOF-based HRC (ex-works basis) in the second half of 2022 decreased to €50-190/mt. In the first half of 2022, the margin was several times higher.

German HRC (BOF steel) domestic market margin, ex-works basis

From September, the governments of the largest European countries such as Germany, France, Italy, and Spain adopted several programs to support the metallurgical industry amid the sharp price increases and shortages of energy resources. For example, Germany has already spent €440 billion to combat the energy crisis. This figure is already almost comparable to the approximately €480 billion which the country has directed since 2020 to protect its economy from the impact of the coronavirus pandemic. These stimulus packages helped producers to reduce energy costs and to restore outputs to a certain extent.

In early 2023, energy prices in the EU have fallen to levels which are closer to those at the start of the Russian invasion of Ukraine. The main reasons are the positive results of the government policies to ease the situation in the sector, the abnormally warm weather, falling EU gas spot prices, and sufficient filling of European gas storage facilities, as well as the European Commission’s plans to reform the electricity market.

The volatility of prices, which are still significantly higher than at the beginning of 2022, continues to affect energy-intensive sectors in EU industry, although pressure on the steel segment may be reduced. However, companies are still considering worst-case scenarios. In Europe, there are also fears regarding the escalation of the war with Russia and the possibility of emergency situations which may affect the supply of energy resources.

Although the energy crisis in the EU and its effects on the steel business have weakened for now, there is a risk of investments shifting from energy-intensive production sectors in the EU to other segments where the cost of energy is lower and margins are still decent. Given competitors with low electricity costs, particularly the US, this factor could weaken Europe’s long-term price competitiveness.