According to the Metal Service Center Institute (MSCI)'s shipment and inventory report, demand for pipe and tubing products has worsened over the last several months. Monthly service center shipments declined from 293,000 nt in October to 197,000 nt and 179,000 nt in November and December respectively. And despite inventory levels decreasing from approximately 803,000 nt in October to 742,000 nt in November and 712,000 nt in December, the lower December inventories equated to about 4.0 months of inventory on hand, compared to 3.8 months in November and only 2.7 months in October.

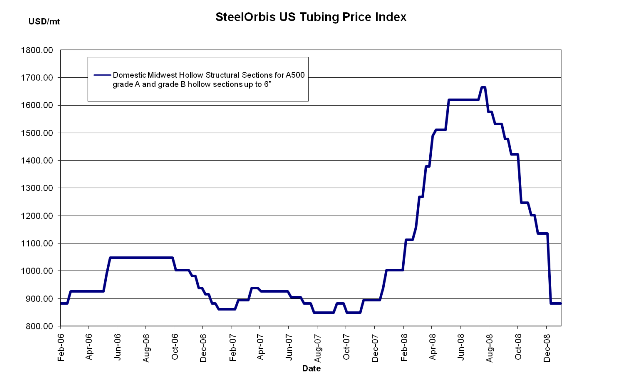

Nonetheless, official domestic HSS prices at the mill level remained unchanged from SteelOrbis' report two weeks ago and are still offered in the approximate range of $39.00 cwt. to $41.00 cwt. ($860 /mt to $904 /mt or $780 /nt to $820 /nt) for A500 grade A and grade B hollow sections up to 6" ex-mill in the Midwest. However, buyers may be able to negotiate deals at up to $1.00 cwt. ($22 /mt or $20 /nt) below the low end of this range on substantial orders of certain sizes. There could still be another moderate decrease on the horizon for most HSS products, although a price decrease would probably first have to be established in the flat rolled market before US tubing mills will lower their prices. Flat rolled products are currently showing signs of softening but no price reductions have yet officially taken place.

Due to the expected decreases on the flat rolled side, the tubing market will most likely trend down and register a decrease of up to about $1.00 cwt. ($22 /,mt or $20 /nt) over the next couple weeks. US tubing prices will not start to trend up again until demand at least firms up, which could take longer than most steel professionals originally anticipated, as the credit crisis is far from stabilizing and any positive economic factors, such as the recently passed stimulus package, are not expected to produce positive results for the steel industry until the latter half of this year at the earliest.

On the import side, most foreign tubing mills are struggling to remain firm in this volatile market. They do not want to lower prices because most feel lowering rates will not generate more sales when demand is so depressed. Nonetheless, most mills will be willing to negotiate orders containing significant tonnage.

South Korea has become more active over the last few weeks and has taken over the place of Mexico as the most aggressive import supplier to the US on the West Coast. While South Korean HSS tubing offers to the US continue to be in the same range as two weeks ago at about $36.00 to $37.00 ($794 /mt to $816 /mt or $720 /nt to $740 /nt) duty-paid, FOB loaded truck in West Coast ports, they may be a little more willing to negotiate than their competition from Mexico, which remains slightly higher in the range of approximately $37.00 cwt. to $39.00 cwt. ($816 /mt to $860 /mt or $740 /nt to $780 /nt), delivered to Texas and California.

Turkish mills seem content to wait for import demand to increase and are remaining firm with price offers in the range of approximately $35.00 cwt. to $36.00 cwt. ($772 /mt to $794 /mt or $700 /nt to $720 /nt) FOB loaded truck, US Gulf Coast ports.

Preliminary license data from the US Import Administration demonstrates that total import structural pipe and tube tonnage arriving to the US in January 2009 is an estimated 22,123 mt, with Canada providing the most tonnage at 9,030 mt. South Korea, China, Mexico and Ukraine all imported similar tonnage during January, at 2,289 mt, 2,252 mt, 2,246 mt, and 2,199 mt respectively.