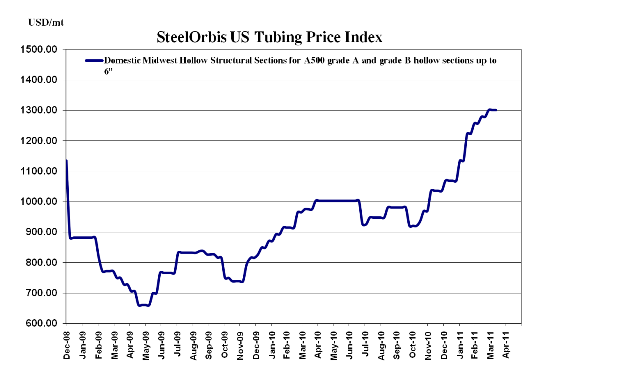

Spot prices for US domestic hollow structural sections (HSS) have followed a neutral trend since late March, while certain import offer prices to the US have fallen dramatically.

Domestic HSS spot prices were forecasted to rise to approximately $60.00-$61.00 cwt. ($1,323-$1,345/mt or $1,200-$1,220/nt) ex-Midwest mill by mid-April, which would reflect a full absorption of the early-February announced $3.00 cwt. ($66/mt or $60/nt) price increase. But while demand levels from end-use sectors like rail car manufacturers and agricultural machinery suppliers are keeping the tubing market relatively steady, concern has been mounting over wavering hot rolled coil (HRC) spot prices and a possible downtrend in scrap prices in May.

As a result, many buyers are being extremely cautious with their bookings, only making purchases to fill inventory holes. For now, the most commonly reported domestic HSS spot prices are still ranging between $58.00-$60.00 cwt. ($1,279-$1,323/mt or $1,160-$1,200/nt) ex-Midwest mill, unchanged from our last report two weeks ago.

On the West Coast, spot prices have firmed to $58.00-$59.00 cwt. ($1,279-$1,301/mt or $1,160-$1,180) ex-West Coast mill, up $1.00 cwt. ($22/mt or $20/nt) on the low end from late March. A price increase for $2.00-$3.00 cwt. ($44-$66/mt or $40-$60/nt) on HSS has been anticipated from West Coast mills for a couple weeks to reflect the mid-March $2.00 cwt. flat-rolled price increase from West Coast flats mills. Although Midwest HRC prices have softened over the past few weeks, spot prices for HRC on the West Coast are holding steady $46.00-$48.00 cwt. ($1,014-$1,058/mt or $920-$960/nt) ex-mill, and with HSS demand still-for the most part-steady, at least a portion of the expected HSS increase is likely to stick.

As for imports, Mexican mills-which many expected to raise tubing offer prices over the last two weeks-are holding off, waiting until the immediate direction of US HSS prices is clearer. Current offers still stand at $50.00-$51.00 cwt. ($1,102-$1,124/mt or $1,000-$1,020/nt) FOB loaded truck in US Gulf ports and $53.00-$54.00 cwt. ($1,168-$1,190/mt or $1,060-$1,080/nt) FOB loaded truck in US West Coast ports.

Overseas, Turkish HSS offers have dipped about $3.00 cwt. since our last report two weeks ago and are now ranging between $47.50-$48.50 cwt. ($1,047-$1,069/mt or $950-$970/nt) duty-paid FOB loaded truck in US Gulf ports for July delivery. With an approximate $10.00-$12.00 cwt. ($220-$265/mt or $200-$240/nt) difference between Turkish tubing offers and US domestic prices, import activity is likely to liven in the near term-particularly for buyers located in close proximity to Gulf Coast ports. However, buyers in other parts of the country maintain that with traditionally higher summer fuel surcharges, overland freight costs on top of the seemingly competitive Turkish offer price make the risk not one they are willing to take.