As US mills have announced modest price increases in several ferrous markets over the last couple months, spot offers have for some products have lagged behind official list prices. Such has not been the case for the US flat rolled sheet market, which has successfully pushed through several successive price increases, totaling as much as $10.00 cwt. ($220/mt or $200/nt) depending on product, since the market started to trend upward in June.

Nucor’s $1.50 cwt. ($33 /mt or $30 /nt) price increase announcement for hot and cold rolled sheet, made Thursday, August 13, was about $0.50 cwt. ($11 /mt or $10 /nt) less than AK Steel’s and US Steel’s October price increases; however, it is still a decent increase given the lack of support from raw materials (benchmark US busheling scrap prices only rose $15/ton this month), and spot offers are already on the rise from last week.

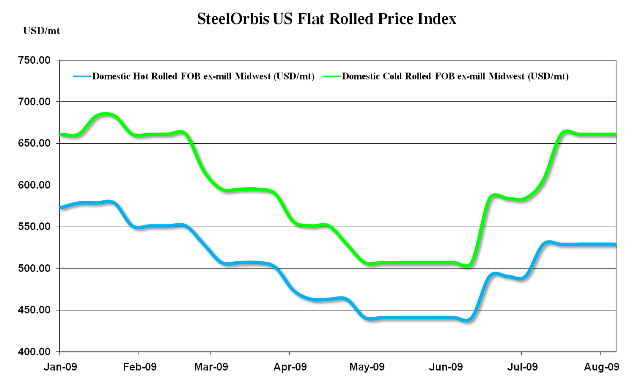

Spot offers for domestic HRC have increased by at least $1.00 cwt. ($22 /mt or $20 /nt) over the past week and can now be found in the general range of $24.00 cwt. to $26.00 cwt. ($529 /mt to $573 /mt or $480 /nt to $520 /nt), with most spot deals booking near the middle of the range.

Meanwhile, domestic cold rolled coil (CRC) offers have increased by about $1.00 ($22 /mt or $20 /nt) over the last week and now range from approximately $30.00 cwt. to $32.00 cwt. ($661 /mt to $705 /mt or $600 /nt to $640 /nt). CRC demand and activity remain far stronger than that for HRC and this is reflected in the gap between HRC and CRC spot offers.

The flat rolled market remains a seller’s market for now but there are still the questions of what will happen at the end of the fourth quarter once more blast furnaces are running at full strength and whether scrap will be able to continue its pricing momentum. Nonetheless, due to the improving demand for US flat rolled and lack of import penetration, it appears that the current domestic flat rolled pricing momentum will be able to carry through the fourth quarter without experiencing any significant setbacks.

As for imports, traders continue to see little activity; however, they are waiting on the newest offshore offers to emerge after Nucor’s increase, as most foreign sources had been waiting for Nucor’s announcement to assess their next price move. It is likely that most foreign offers for HRC and CRC will mirror the US domestic increase and climb by at least another $1.50 cwt. ($33 /mt or $30 /nt), though offers in general remain scarce and the most recent offshore offers were already significantly higher-priced than domestic material. Furthermore, many import sources have already exited from the US market entirely and are content to offer to more lucrative markets, primarily in Asia. China and India are expected to keep at least one foot in the US CRC and HDG markets, though.