According to Germany-based independent think tank Agora Industry, Europe’s transition away from coal-based steelmaking will depend not only on new low-emission production technologies but also on the creation of stable long-term demand for near-zero emissions steel.

The organization stated that despite support from the EU Emissions Trading System (ETS) and government incentives, many green steel projects are still struggling to reach final investment decision (FID) due to uncertain market conditions and weak demand visibility.

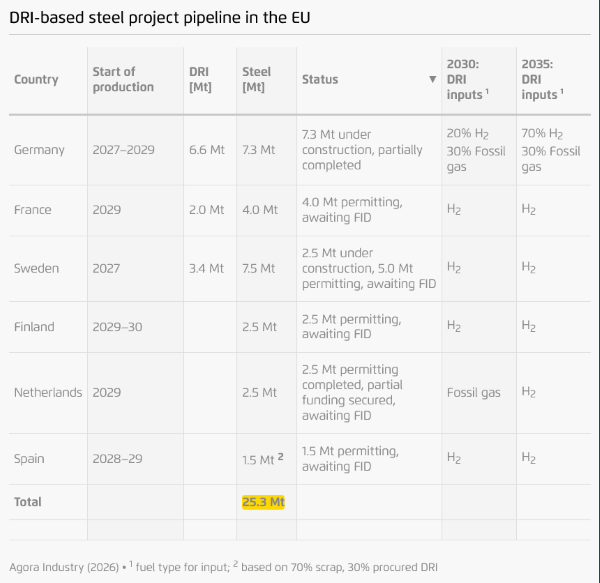

Europe has large pipeline of near-zero steel projects

Agora Industry noted that the EU currently has approximately 34 million mt of announced near-zero capable steel projects based on direct reduced iron (DRI) technology. According to the report, around 25 million mt of these projects are progressing through permitting, construction, and FID stages. The think tank stated that these volumes could theoretically satisfy the European automotive sector’s entire demand for near-zero emissions steel by 2035 if stronger market-support mechanisms are introduced.

The report identified the European automotive sector as a potential catalyst for accelerating demand for low-emission steel products. The sector consumes approximately 15 million mt of mainly flat and high-quality steel each year, most of which is currently produced through traditional coal-based blast furnace routes.

Four factors support automotive sector’s role

Agora Industry outlined four main reasons why the automotive industry could become a major driver of green steel demand.

First, the sector’s large and stable steel consumption could provide steelmakers with reliable long-term demand, helping de-risk investments in hydrogen-based DRI projects. Second, due to strict quality requirements for automotive-grade steels, scrap-based electric arc furnace production alone will not be sufficient to meet decarbonization targets. According to the report, the sector will require DRI-based ironmaking combined with electric arc furnaces or existing blast furnace infrastructure. Third, the organization stated that low-emission steel would have only a limited impact on final vehicle costs, since steel represents less than one percent of total car production costs. Fourth, the report highlighted that steel production currently accounts for between 16 percent and 27 percent of total vehicle lifecycle emissions, meaning decarbonizing steel supply chains could significantly reduce automakers’ Scope 3 emissions.

Regulatory uncertainty remains major obstacle

At the same time, Agora Industry warned that uncertainty surrounding definitions and standards for low- and near-zero emissions steel continues to represent a major obstacle for investment decisions. According to the organization, several competing international standards and ongoing EU legislative processes have yet to establish a harmonized framework.

The report also cautioned that some projects currently categorized as low-carbon could continue relying on fossil gas beyond 2035 unless stricter future regulations aligned with net-zero pathways are introduced.

Agora Industry concluded that Europe already has a substantial pipeline of clean steel projects but stressed that stronger lead-market policies, harmonized standards, and broader support for upstream sectors such as green hydrogen production will be necessary to transform announced projects into bankable investments and accelerate deployment of climate-neutral steelmaking technologies across the EU.