2020 was a year full of happenings and troublesome news for many, but its last quarter came as a surprise to steel market players in particular and for most of them the developments in this period were extremely positive. From early October up to the end of the year, prices surged by far over $200/mt, resulting from the lucky combination of a number of factors globally rather than from healthy market conditions.

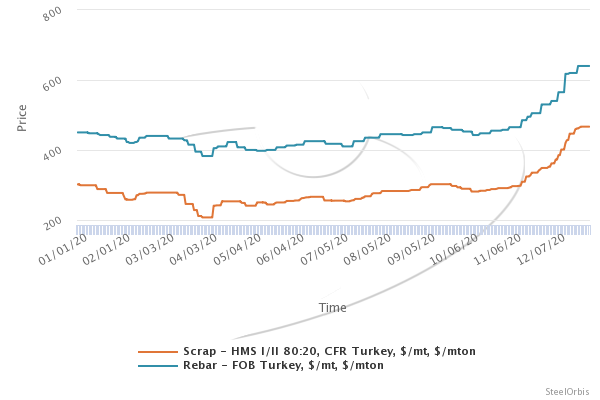

While through most of the year the steel business environment worldwide was challenging as a result of the global pandemic and some economic issues locally in different countries, by the end of the year the price increase seen in the market had been so big and rapid that a lot of players started to compare the situation with that observed back in 2008. Turkey showed a tremendous uptrend with prices surging by $20-50/mt at a time: in the opinion of many the flats market situation gave the initial fuel to the uptrend, while in the longs segment the price rise was driven more by the scrap market.

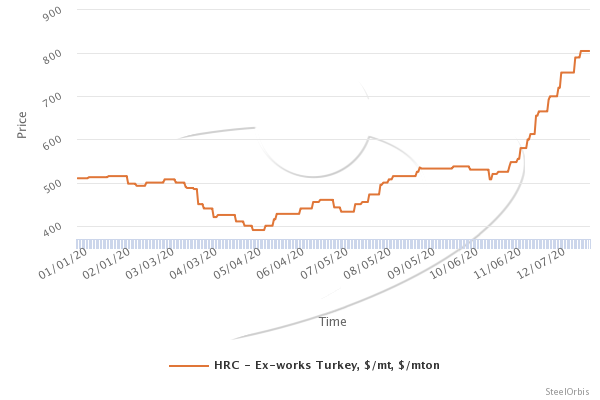

In late October and early November, Turkey witnessed some good demand for its coated and cold rolled steel, with orders mainly coming from Europe where buyers had been too cautious regarding the second wave of the Covid-19 pandemic and did not keep much stock, fearing further lockdowns. Good sales to export markets naturally supported local Turkish demand as the available volumes had been melting. Higher-priced downstream products allowed re-rollers to accept higher prices for HR feedstock, which supported the Turkish mills, which had also already been enjoying good demand in the EU. Along with low stocks on the buyers’ side, local production and supply of flats in Europe had been reduced and, while Asian exporters had been concentrating on their own regional sales, Turkey had become one of the few sellers with available volumes. As a result, Turkish mills were able to sell out their December and January production HRC within a rather short period of time, with a price increase at each step.

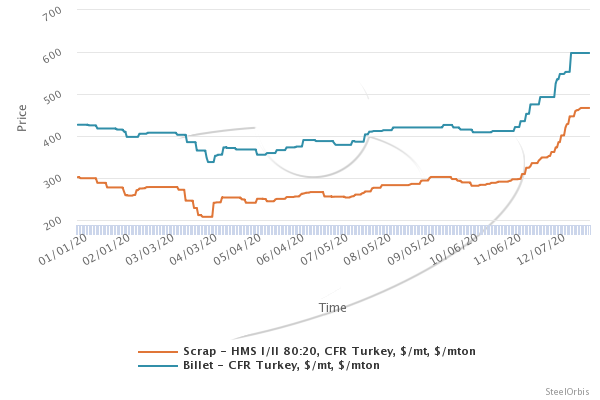

In the meantime, the supply situation in the scrap market became tight as a result of lower collection in some regions or due to increased sales to local scrap markets instead for export since local steel production rates had been increasing. Sales to Latin America at prices much higher than Turkey had been ready to pay also affected the scrap allocation from the US. Along with its stronger finished steel sales, in the flats segment specifically, Turkey had been able to accept higher and higher prices for scrap since there were fears that there would not be enough raw material to secure production needs for steel which had already been sold out.

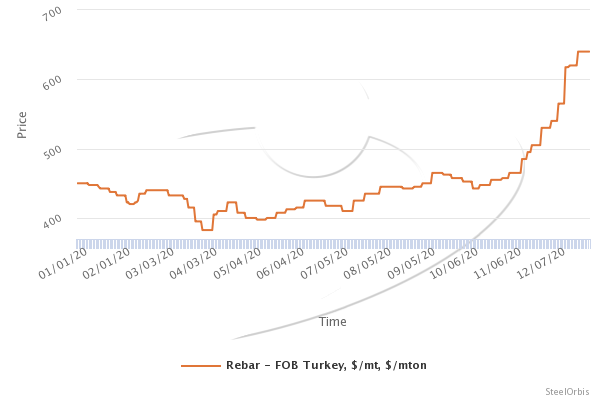

In early December, it became clear that the market situation in Europe was developing in a more positive manner than initially expected and the lack of supply resulted in higher and higher local HRC prices, thus giving Turkey and the CIS another reason to avoid discounts. In Turkey’s rebar segment, the situation was also positive, but was driven more by scrap than by a significant improvement in demand. Increased sales locally resulted mainly from buyers having no other options in terms of supply sources, while the market was not giving any signs of a trend reversal. As regards Turkey’s rebar exports, some cargoes were sold to Asia and good volumes were traded to Latin America, to Peru specifically. In the meantime, HRC prices continued climbing on a daily basis and buyers accepted each new rise, fearing there would be not enough allocation. It is worth mentioning that prices for coated and cold rolled steel had been rising at a faster pace, while at the end of the year the price gap between HRC and CRC had hit and exceeded $200/mt, as opposed to the usual $80-100/mt.

Although the Asian markets and China in particular were mainly positive in the fourth quarter of 2020, by the end of the year it had become clear that Turkey had outpaced Asia in terms of price increases. A lot of market players considered the Turkish market to be seriously overheated as prices for HRC exceeded $800/mt ex-works, while the workable level in Asia by the end of December was $695-700/mt CFR. In fact, it was considered that the higher prices in Turkey could attract Asian sellers and a lot of market players thought that this could be the start of price trend reversal as the supply situation could be eased with the increased number of sellers. The strong uptrend in the finished steel segment naturally triggered a similar price rise for semi-finished steel. Slab suppliers benefitted mainly from the positive situation in Turkey, while billet was sold principally to Latin America, the Middle East and Turkey.

Interestingly, the skyrocketing prices of scrap, finished steel and semi-finished steel globally seen in the last two to three months of the year led to several protective initiatives, in the CIS in particular. Local buyers in the CIS region felt threatened since exports had become too attractive for CIS-based suppliers and their allocation for the local market had diminished. In addition, the much higher export prices had to be balanced with domestic price levels, which were considered unacceptable by local contractors and flat steel end-users, who are basically dependent on local suppliers only. As a result, Russia ended the year evaluating an initiative to establish export taxes of 13 percent (but not less than $73/mt) for billet, 13 percent for rebar (but not less than $78/mt) and 15 percent (but not less than $49/mt) for scrap, to be imposed for six months. In Ukraine, local steelmakers were also complaining of the lack of availability of scrap supplies, since the valid €58/mt tax was not restricting scrap exports since global prices had increased too much. According to sources, discussions were being carried out on whether to raise the export tax by 100 percent or to bring in a total ban on scrap exports from Ukraine as a temporary measure.

Although the year ended on a positive note for steel market players, mainly producers, there is no clear picture for the first quarter of 2021. On the one hand, scrap allocation globally looks set to remain limited and some sources expect that import prices in Turkey could hit $500/mt. On the other hand, China’s HRC market showed a significant weakening at the end of the year, which is considered to be a bad sign for the trend in the Mediterranean region. As regards finished steel, a lot of sources expect January to be relatively positive with no big discounts, but for February many foresee a downward correction of at least $20-50/mt for HRC specifically, partly as producers went too far in their recent price increases.