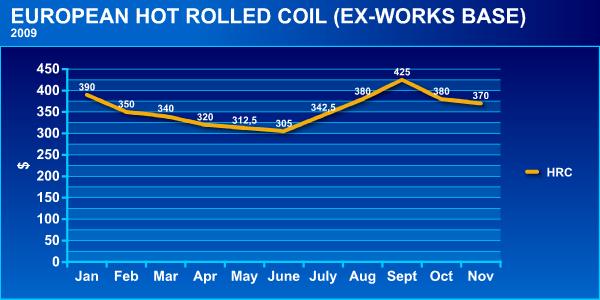

In September after the return from the holidays, HRC ex-works prices in Europe reached the level of €430/mt on the back of the restocking activities of steel service centers and distributors. However, Europe's HRC ex-works prices have now decreased to levels even lower than the pre-holiday prices, since the increase in question was not supported by real demand on the end-user side. On the other hand, import HRC offers for Europe have this week been at €320-360/mt CFR, though buyers are hesitating to buy at these competitive levels due to the long lead times involved. Additionally, European customers are increasingly adopting a wait-and-see policy as further price decreases are expected to be seen in offers from the Far East. In this situation, the increased competition between Indian and Chinese origin HDG offers is now attracting greater attention.

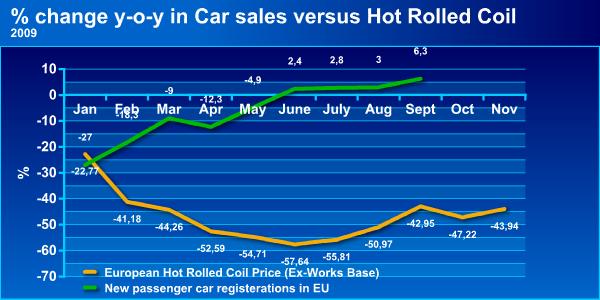

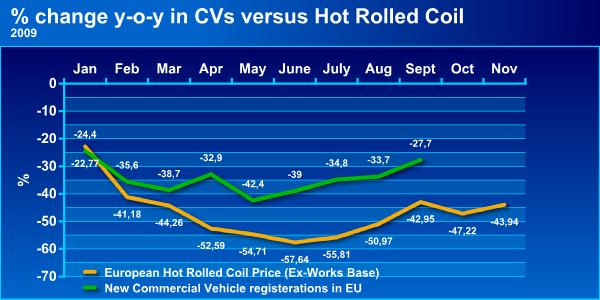

Due to the uncertainty surrounding prices in Europe, order tonnage volumes are decreasing in the local flat steel markets. Real demand is still weak on the end-user side in Europe, where the leading flat steel consuming sectors are the automotive and construction sectors. Despite the recovery seen in passenger car registrations in Europe thanks to discounts made available for new car purchases against the trading in of used cars, figures for Europe's general car exports and commercial vehicle sales are still at weakers levels compared to 2008.

According to the ACEA (European Automobile Manufacturers' Association) data, EU passenger car sales have decreased by 6.6 percent year on year in the first nine months of 2009. The only EU-15 countries which registered positive numbers are Germany (26.1 percent), Austria (6.7 percent) and France (2.4 percent).

However, looking at the ACEA data again, we can see that the recovery in commercial vehicle sales is far slower. Also, contrary to the figures for passenger cars, no EU-27 country has registered positive numbers for commercial vehicle sales.

On the other hand, pessimism is seen in the European construction market in general. Commercial and industrial construction projects have been influenced heavily by the fact that current demand for buildings is far lower compared to current numbers of completed buildings. Also, the psychological situation of investors and of the financial sector exerts an influence. However, although the impact of public expenditure has been limited in 2009, it is expected to have a more positive influence in 2010.

When we look at the above graph which shows EUROFER data for actual 2008 growth and growth projected for 2009-2010 in various EU sectors, it appears that the downtrend in almost all flat steel consuming sectors (except shipbuilding) in the EU will come to a halt in 2010.

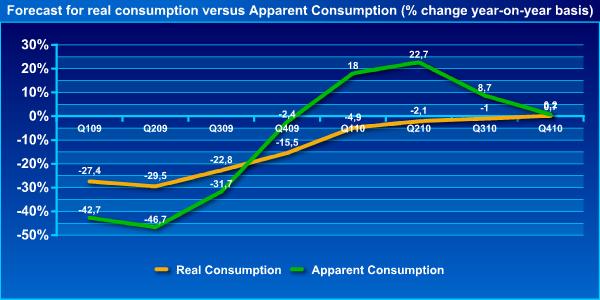

Looking at the above graph with its comparison between real consumption and apparent consumption (based on actual to-date figures and predicted figures), a serious recovery is expected to be seen in end-user demand as of the first quarter of 2010 as a result of the massive destocking process carried out in 2009.