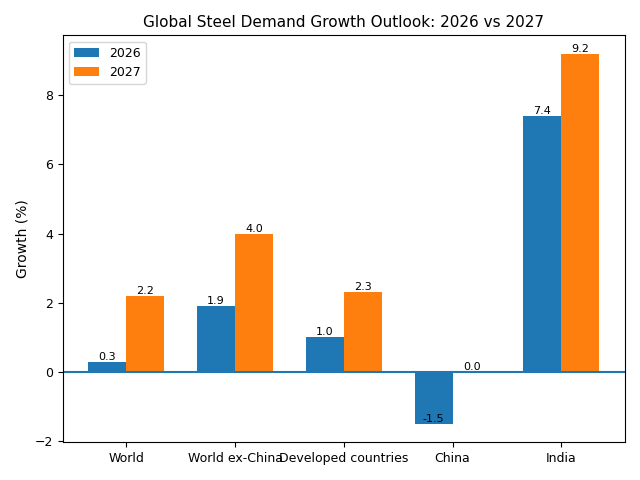

According to the April 2026 Short Range Outlook (SRO) report released by the World Steel Association (worldsteel), global steel demand is expected to increase by 0.3 percent in 2026 to reach 1.72 billion mt, marking a modest recovery, while growth is forecast to accelerate to 2.2 percent in 2027, bringing demand to 1.76 billion mt.

Signs of bottoming out in global demand

UNESID’s Chief Economist and Chair of the worldsteel Economics Committee Alfonso Hidalgo Calcerrada stated that the latest forecasts are in line with the projections published in October 2025, confirming that global steel demand bottomed out in the 2025-2026 period and is entering a gradual recovery phase as of 2026.

According to the report, the acceleration in growth in 2027 will be driven mainly by diverging regional dynamics. The slowdown in the rate of contraction in China and the strong demand growth in developing markets, particularly India, are among the key factors supporting the global outlook.

Middle East risks weigh on demand Outlook

The report indicates that the ongoing conflict in the Middle East is expected to lead to a sharp decline in the region’s steel demand in 2026, emerging as a key factor negatively affecting a region that had previously been expected to show strong growth.

However, under the base-case scenario, the conflict is assumed to be resolved by June, in which case demand in major economies is expected to remain generally resilient. Nevertheless, if hostilities persist beyond the second quarter, downward revisions may be required, particularly for regions with high energy sensitivity.

China’s contraction slows, flat outlook for 2027

China’s steel demand contraction is expected to ease to 1.5 percent in 2026, as the correction in the housing market approaches its bottom. Increased infrastructure investment and export-supported manufacturing are expected to partially support demand.

In 2027, demand in China is projected to remain largely flat. As the prolonged correction in the real estate sector nears its end, demand is expected to transition to a more balanced structure.

Growth in developing economies to slow in 2026

Steel demand growth in developing economies excluding China is expected to slow to 2.5 percent in 2026. This deceleration will be driven by the sharp contraction in the Middle East and the normalization of stockpiling activity in ASEAN countries.

However, growth is forecast to accelerate to 5.1 percent in 2027, supported by strong demand in developing Asia and Africa, along with a recovery in the Middle East.

India maintains strong growth momentum

India continues to be the fastest-growing major steel market globally, with demand expected to grow by 7.4 percent in 2026 and accelerate to 9.2 percent in 2027. Infrastructure investments, the automotive sector, railway expansion and rising demand for consumer goods are among the key drivers.

Recovery underway in developed economies

Steel demand in developed economies is estimated to have increased by 0.2 percent in 2025, ending a three-year decline. Growth is expected to reach one percent in 2026 and further accelerate to 2.3 percent in 2027.

In the EU and the UK, demand is forecast to grow by 1.3 percent in 2026 and three percent in 2027, supported by increased infrastructure and defense spending as well as improving macroeconomic conditions. However, volatility in energy prices remains a key downside risk.

In the US, steel demand is expected to grow by 1.7 percent in 2026 and two percent in 2027. While private sector investments and infrastructure spending will support demand, high costs and tight financing conditions are likely to limit the pace of recovery.

Overall outlook: stronger recovery in 2027

Overall, global steel demand is expected to enter a recovery phase with modest growth in 2026, followed by a broader and stronger expansion in 2027. However, geopolitical risks and uncertainties in the global trade environment will remain key factors shaping the outlook.