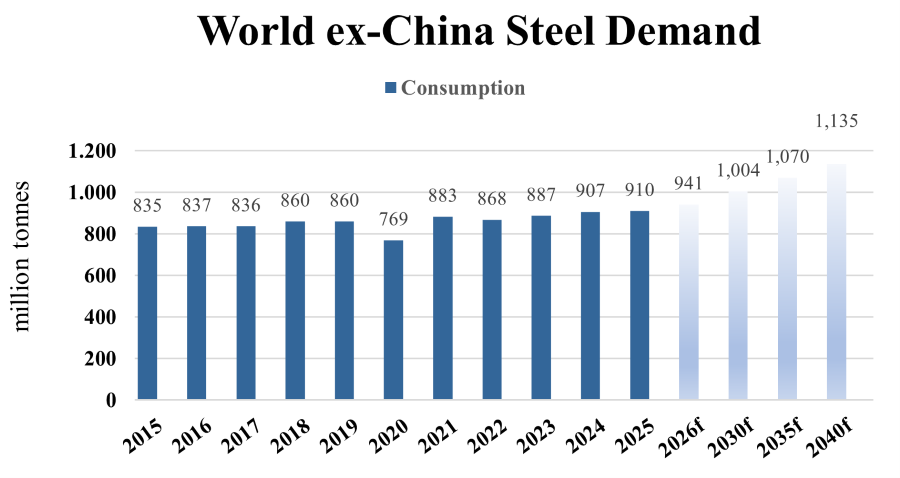

Apparent demand growth in the World ex-China the past five years has not been sufficient to absorb the excesses in the system, especially those emanating from China:

- ASC has risen from about 860 million tonnes in 2019, the last full year preceding the Covid pandemic, to an estimated 910 million tonnes in 2025 for a CAGR growth rate of exactly 1.0% during that period.

- India was a key exception to this trend, posting a CAGR growth of 7.3% during the same period, with demand rising to 153 million tonnes in 2025 from about 101 million tonnes in 2019.

- When excluding India, steel demand in the World ex-China actually declined at a rate of -0.1% during the same period, from 759 million tonnes in 2019 to 757 million tonnes in 2025.

The combination of stagnant demand in the World ex-China/India and rising exports from China has proved to be the Achilles heel for international steel prices in the last handful of years:

- The price of hot-rolled band on the World Export market has declined from an average of $498 per tonne in 2019 ($542 per tonne 2018-2019 average) and a high of $905 per tonne in 2021 (the post-Covid peak) to $466 per tonne in 2025.

- The combined cost of integrated steelmakers’ raw materials – iron ore and coking coal – has risen from an average figure of $311 per tonne in 2019 to $333 per tonne in 2025. (Note: these figures are based on the prevailing prices of 62% Fe iron ore, delivered to northern China ports combined with the price of Australian premium coking coal, FOB port of export, adjusted for usage ratios, respectively.)

- Hence, the “spread” between the price of hot-rolled band, FOB port of export, and the cost of integrated raw materials has compressed from $187 per tonne in 2019 (and a recent peak figure of $504 per tonne in 2022) to only $113 per tonne in 2025.

The “spread” figure – a good proxy for the profitability of export-oriented integrated steelmakers – is the lowest on record going back to 2009 in the aftermath of the Global Financial crisis. Even the period of ultra-depressed prices driven by the Chinese “Export Armada” of 2015-2016 at an average “spread” of $174 per tonne does not compare to the most recent situation.

- Hence, the key question for the World Export price of Hot-rolled Coil and related products in the decade ahead is whether the most recent experience of historically depressed spreads over raw material costs – i.e. the margin – is a medium to long-term phenomenon or a more typical brief “shake-out” period?

- Our forecast assumes the answer lies somewhere in the middle: a potential prolonged “shake-out” period that lasts several years on a combined basis in the early part of the cycle – rather than several brief downside “blips” as in prior cycles – followed by a gradual recovery as capacity reductions in China catch-up to waning demand during the second half of the cycle.

As a generality, WSD sees the regional pricing dynamics being driven by a combination of “traditional” market forces – such as regional supply/demand, international steel product trade, raw material prices, etc. – and non-industry-specific dynamics, such as:

- The evolution of the “Age of Protectionism,” not only with respect to direct steel trade but increasingly the “indirect” trade in steel-intensive (such as automobiles, etc.) and other manufactured goods.

- The continuation, or perhaps the stalling-out, of the Decarbonization movement seeking to reduce industry emissions in various ways, depending on regions and government policies.

- The Artificial Intelligence Revolution and its impact on global energy demand, employment, and manufacturing technologies among a slew of other “existential” ramifications.

- Shifting global World Order—Under the second Trump administration, trade deals are rapidly changing, and the role of American diplomacy has shifted significantly.

This report includes forward-looking statements that are based on current expectations about future events and are subject to uncertainties and factors relating to operations and the business environment, all of which are difficult to predict. Although we believe that the expectations reflected in our forward-looking statements are reasonable, they can be affected by inaccurate assumptions we might make or by known or unknown risks and uncertainties, including among other things, changes in prices, shifts in demand, variations in supply, movements in international currency, developments in technology, actions by governments and/or other factors.

The information contained in this report is based upon or derived from sources that are believed to be reliable; however, no representation is made that such information is accurate or complete in all material respects, and reliance upon such information as the basis for taking any action is neither authorized nor warranted. WSD does not solicit, and avoids receiving, non -public material information from its clients and contacts in the course of its business. The information that we publish in our reports and communicate to our clients is not based on material non-public information.

The officers, directors, employees or stockholders of World Steel Dynamics Inc. do not directly or indirectly hold securities of, or that are related to, one or more of the companies that are referred to herein. World Steel Dynamics Inc. may act as a consultant to, and/or sell its subscription services to, one or more of the companies mentioned in this report.

Copyright Ó 2026 by World Steel Dynamics Inc. all rights reserved