Vietnam, which for nearly a decade had been one of the most important hot rolled coil (HRC) import destinations in Southeast Asia, is gradually losing its strategic weight in the regional flat steel market. In 2025, the country’s HRC import profile changed notably, reflecting a combination of trade defence measures, intensifying supplier competition and a stronger preference for domestic material. While Vietnam remains a large steel consumer, it is no longer the magnet for HRC imports that it once was.

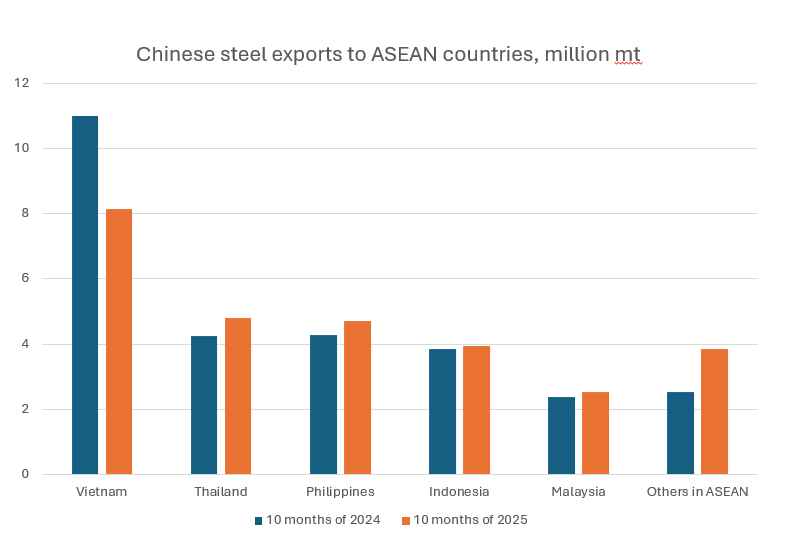

China’s steel shipments to Vietnam down 5.9 million mt in Jan-Oct

According to Vietnam’s customs data, total steel imports in the first ten months of 2025 reached around 12.72 million mt, down roughly 13.5 percent year on year. China remained the largest supplier in 2025, shipping about 7.48 million mt, but down by 44 percent or 5.88 million mt year on year.

Flat steel, including HRC, continued to account for the largest share of these volumes, but overall HRC imports declined compared with 2024, when the country had imported an estimated 12.6-12.7 million mt. In the first half of 2025, Vietnam imported 4.5 million mt of HRC, a sharp decline from nearly 6 million mt in the same period of 2024. Of this total, HRC imports from China amounted to 2.8 million mt, down 36 percent year on year. However, according to sources, imports of steel with widths of 1,880 mm or more to Vietnam were unusually high.

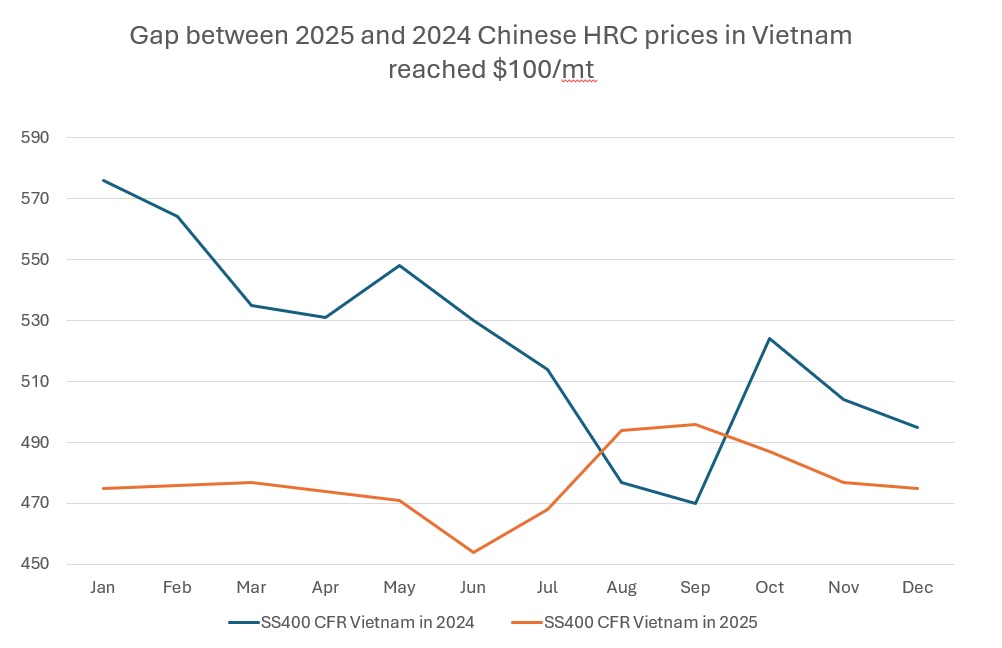

The most decisive factor behind the drop in imports has been Vietnam’s antidumping (AD) policy against Chinese HRC. Following a petition from domestic producers, Vietnam’s Ministry of Industry and Trade launched an AD investigation into HRC imports from China and India in mid-2024. In February 2025, Vietnam imposed provisional AD duties ranging from around 19 percent to nearly 28 percent on certain hot rolled flat steel products of Chinese origin, with the measures entering into force in March. By July 2025, definitive duties of 23.10-27.83 percent were imposed for a five-year period, covering carbon and alloy HRC with thicknesses from 1.2 mm to 25.4 mm and widths up to 1,880 mm.

These duties have proven effective in curbing Chinese HRC inflows. Imports of standard ex-China SAE1006 HRC largely disappeared from the Vietnamese market in 2025, as the tariff burden erased the usual price advantage. The only notable Chinese HRC still entering the country has been Q195 material with thickness of around 2 mm, which currently falls outside the scope of the duty. However, market participants increasingly expect this loophole to be addressed, as the Vietnamese authorities have already launched anti-circumvention investigations and there are widespread rumours that Vietnam may tighten the duties further to cover additional specifications and close existing gaps.

Competition inside Vietnam surges even excluding China

With Chinese volumes retreating, competition among foreign suppliers has intensified. Mills from Japan, South Korea, Taiwan, Indonesia and Malaysia have attempted to fill the vacuum left by China, while India became increasingly active toward the end of the year. Japan shipped around 1.82 million mt of steel to Vietnam in the first ten months of 2025, followed by South Korea with roughly 1.3 million mt and Indonesia with 1.02 million mt. However, despite this broader mix of suppliers, none of these countries have managed to significantly boost their HRC volumes into Vietnam on a sustained basis.

One major reason is the growing dominance of local producers. In 2025, domestic mills such as Formosa Ha Tinh Steel and Hoa Phat Group were clearly favoured by Vietnamese end-users, particularly amid tighter trade protection and a stronger “buy local” sentiment. Local material was more readily accepted for infrastructure, manufacturing and downstream processing, limiting the room for imported HRC to regain lost ground. As a result, the influx of alternative foreign supply translated more into intensified price competition than into a meaningful increase in total import volumes.

India was the only supplier that managed to stand out toward the end of the year as Chinese volumes collapsed under AD duties and foreign competitors struggled to expand their market shares. Indian mills became more aggressive on pricing, offering sizable discounts to secure bookings after Chinese material exited the market. According to export data, Indian shipments of hot rolled coil/sheet rose by about 12 percent year on year to around 0.67 million mt in the April-August period of 2025, underlining increased export activity even as overall volumes remained modest relative to China and other major suppliers. While Vietnam has been among the destinations for Indian steel coil exports, India’s overall HRC export volume in 2025, though growing, has not been sufficient to offset the sharp decline in Chinese imports into Vietnam, underscoring the limits of its market penetration.

Future of Vietnam’s HRC segment - from imports to exports?

As Vietnam’s import volumes flatten and domestic production gains ground, the country’s role in the ASEAN HRC trade is evolving. “For years, Vietnam served as the primary outlet for surplus regional and Chinese HRC, shaping price trends across Southeast Asia. In 2025, however, the combination of effective AD measures, rising domestic supply and fragmented foreign competition pushed Vietnam into a more balanced and less import-driven position,” a representative of a Vietnamese steel mill told SteelOrbis.

Looking ahead, Vietnam’s HRC market is likely to remain highly regulated and intensely competitive. A further tightening of trade defence measures remains a realistic possibility, particularly if importers continue to exploit specification-based loopholes. For ASEAN steel giants and Asian exporters, this marks a new stage: Vietnam is no longer an easy growth market for imported HRC, but a battleground where margins are thin, volumes are capped, and domestic players increasingly set the tone.

At the same time, in 2026, Vietnam is expected to cautiously explore its export potential for HRC. While the country is unlikely to become a large-scale net exporter in the near term, limited volumes could be directed to selected ASEAN markets where supply gaps persist. The EU, which has been a key strategic focus for Vietnamese flat steel producers, is likely to become a far more challenging destination next year due to the full implementation of CBAM cost obligations and rising compliance costs. Combined with thin margins, freight costs and growing trade defence risks globally, these factors are expected to curb aggressive export expansion. As a result, Vietnamese mills are likely to prioritize domestic market stability and downstream value-added products, with exports playing a supplementary, balancing role rather than acting as a primary growth driver.

According to Vietnamese customs data, in the first ten months of 2025 total steel exports reached 8.57 million mt, down by 22 percent year on year. The sharp decline indicates a significant drop in average export prices amid global market challenges. Cambodia was the top export market, reaching 1.23 million mt, up 26.42 percent year on year, accounting 14.41 percent of the total export volume amid widespread declines in major markets such as the US, Japan and the EU. Exports to other key markets like Italy settled at 925,946 mt, down by 22 percent year on year, while sales to India reached 773,823 mt, increasing by 9.96 percent year on year.