The steel exports from China have reached an all-time high in 2025, estimated to be at 116-118 million mt. What laid behind this surge despite increasing antidumping and safeguard measures around the globe? In 2026, export volumes are expected to go down, but the major question is how much? SteelOrbis has polled market sources to answer these questions for our end-year reviews.

How did China manage to hike export volumes in 2025?

- Increase of presence in the MENA region and South America

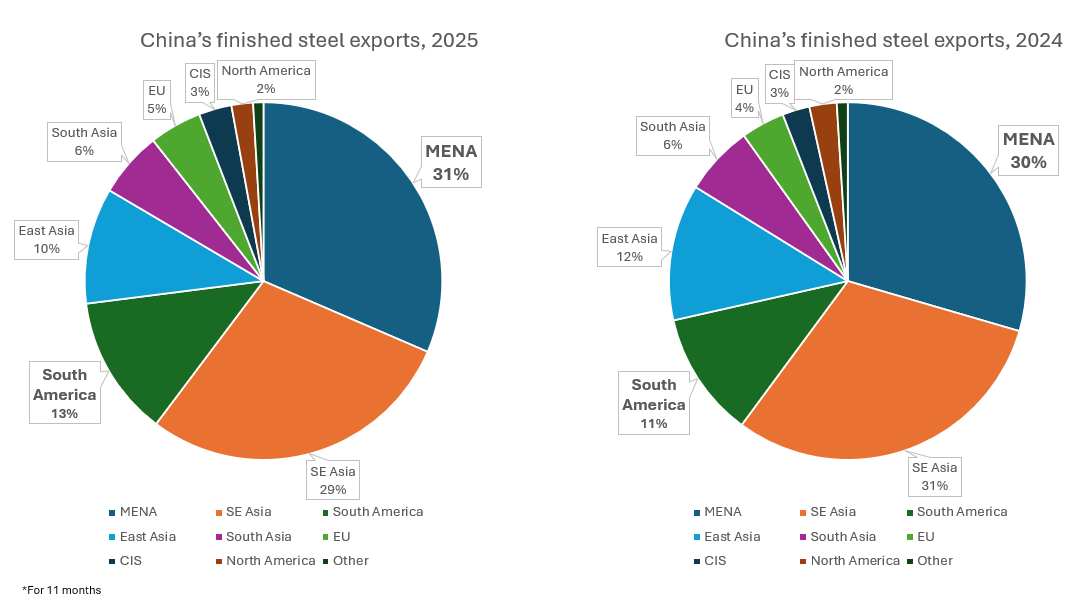

China’s finished steel exports added 6.7 million mt in the January-November period this year, and it amounted to 107.717 million mt, according to official customs data. And by the end of this year, this result looks impressive and unexpected, as most official and unofficial sources claimed in late 2024, that the export volumes would hardly be above 100 million mt this year due to increasing protectionism globally. From the geographical point of view, the support has come from the MENA region, and most specifically from the GCC.

In 2025, the MENA region (the GCC, Turkey and Africa) for the first time has become the number one of the destinations for Chinese finished steel exports with the share of 31 percent, outrunning SE Asia with 29 percent share. Only to the MENA region, China managed to enlarge exports by almost 4 million mt (over 11 months). Among the countries, Saudi Arabia has posted the biggest jump this year – by over 18 percent compared to 2024 with active flat steel exports from China and no restrictive measures for flats, together with increasing demand. Shipments to the UAE from China have been rather stable in 2025 after a surge by as much as 46 percent seen in the previous year. Also, increased competition with other Asian flat steel suppliers has prevented China from increasing its already strong position in the UAE. “China has taken most of Russian’s share in Africa [in the longs steel segment] amid very low prices and good payment terms with huge payment deferment,” an international trader told SteelOrbis. As for Turkey, finished steel shipments from China lost 10 percent in 2025 due to drop in HRC sales as a part of the import market has been taken by Malaysia and Egypt, which are duty free in Turkey.

Top 12 countries, buying Chinese finished steel in 2025 (for Jan-Nov period)

| Rank | Country | Volume, million mt | Change, y-o-y (%) |

| 1 | Vietnam | 9.246 | -21.50 |

| 2 | South Korea | 6.651 | -11.50 |

| 3 | Thailand | 5.195 | +11.90 |

| 4 | Philippines | 5.181 | +11.70 |

| 5 | UAE | 5.044 | +0.90 |

| 6 | Saudi Arabia | 5.029 | +18.40 |

| 7 | Indonesia | 4.311 | -2.60 |

| 8 | Turkey | 3.435 | -10.23 |

| 9 | Brazil | 3.105 | -7.52 |

| 10 | Pakistan | 2.801 | +31.40 |

| 11 | Malaysia | 2.797 | +5.40 |

| 12 | Peru | 2.105 | +32.10 |

Apart from the MENA region, another bright spot for China was South America, whose share in China’s total finished steel exports increased from 11 percent to 13 percent in 2025. Some reduction in sales to Brazil was a result of the introduction of temporary tariff hikes and quotas on several steel products from 2024 onward, which later expanding to 25 tariff lines, while smaller economies in the region has very limited protection and Chinese products are among the most competitive in terms of prices.

The major drop in sales volumes China has experienced in Vietnam was because of the AD duty imposed in late 2024, but overall the volume sold by China to SE Asian region has remained almost stable (around 31 million mt) mainly amid higher exports to Thailand and the Philippines, which do not have enough own capacities (especially in the flats segment).

- Non-VAT sales still active

China has managed to keep and strengthen its export positions mainly amid competitive prices. Despite attempts of the government to forbid non-VAT trading since 2024, it has been still rather active by December 2025. “After new taxation system [announced in April] we expected non-VAT will be gone forever, but traders found a way and we saw a pause in offering non-VAT of about a month or two maximum,” a Chinese trader said. Non-VAT trading is the most popular in the HRC and wire rod segments, while some rebar has also been traded in this way. Market sources from China, involved in the export business, said that from one side, non-VAT trading should be stopped sooner or later by the government, but in 2025 the exports of steel was critical, considering oversupply in the local market, so “traders can always find a way if there is a big necessity in it,” one of the large trader commented.

As for the future of non-VAT trading, China’s Customs will require documentation from the actual exporter, the sales contract, and the warranty certificate, and it has also joined forces with the tax bureau and the State Administration of Foreign Exchange to conduct joint oversight. These measures target the long-standing practice of “buying export documents”. Anyone caught evading the rules may be required to pay 13 percent VAT, corporate income tax, and individual income tax, so the cost of non-compliance may be quite high. However, it needs more time to observe the actual effect in practice.

- Surge in semis and longs exports offset drop in flats

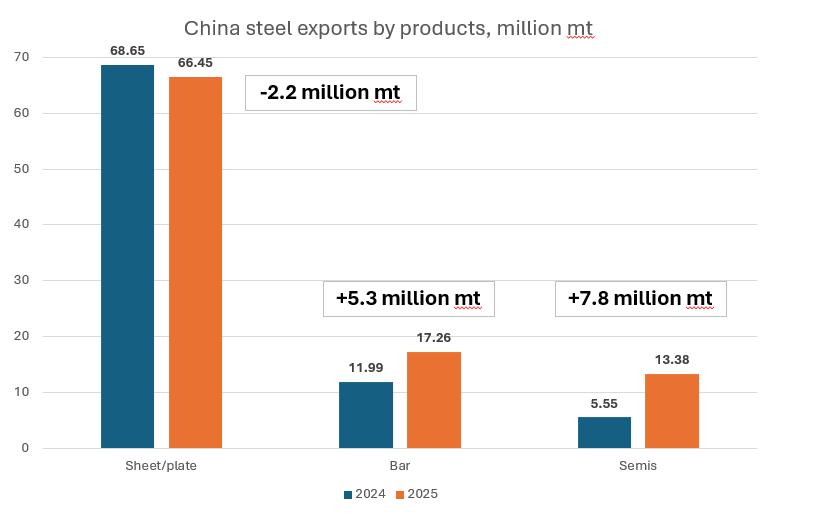

Due to structural overcapacity in China's longs market amid the deep recession in its domestic real estate industry, steel enterprises were increasingly willing to export. In 2025, the increase in finished steel export mainly comes from longs with only bar shipments overseas added 5.8 million mt in 11 months of 2025, fully offsetting drop of HR coils and sheet shipment amounting to 2.2 million mt. The flats export slows down mainly amid the anti-dumping measures. In particular, Vietnam, though still as the largest steel export destination for Chinese steel, consumes less flats from China, with the same trend seen in South Korea. However, other countries in Southeast Asian markets partially compensated this decline. Moreover, the GCC countries are pressing ahead with infrastructure projects, becoming more reliant on Chinese steel—especially high-end plate and section products. Meanwhile, Nigeria, Tanzania and Ghana imported more steel from China, acting as new growth engines to attract China’s long steel. The trend of better growth in longs exports than flats is likely to sustain in 2026.

At the same time, semi-finished exports from China have gathered momentum and posted the highest growth compared to other major export product groups – increase by over 140 percent or 7.8 million mt in January-November 2025. Almost all major destinations increased buying billets from China due to competitive prices with the largest part of billet volumes still being for the Asian market with SE Asia and Taiwan accounting for 40-45 percent of total billet exports from China, but with the hike this year, the share of Turkey increased to 10-11 percent, while Saudi Arabia account for 6-7 percent of shipments from China. “Billets or even slabs exports is not an aim of the government,” a Chinese trader said, adding that in the coming years the government will more actively promote the export of higher-value added products.

Outlook for 2026

China’s steel export volume is expected to decrease by 15-20 million mt, coming near to the 100 million mt mark in 2026, according to market sources polled by SteelOrbis. The direct export volume of steel in China should be already at peak and should indicate gradual decreases in the coming years, while the indirect export might keep strong growth in 2026 via vehicles, home appliance, shipbuilding, wind power, photovoltaic (PV), 5G, and other mechanical and motor products.

China is implementing a license system for 300 items as of January 1 2026, which will slightly increase the export costs and affect the export volume and structure, but mainly only in the first quarter of 2026, though the actual effects for the total volumes in 2026 may be rather limited as the major target of the new system is to stop non-VAT trading.

One of the important destinations, where China may lose its share in 2026, is Vietnam as the country initiated an anti-circumvention probe against ex-China imports of certain wide-width HRC. If the serious measures are implemented, Chinese HRC exporters may lose 20 percent market share or above, market sources believe.

China’s exports to GCC region might exceed 13 million mt in 2025 and since the economic growth rate of the GCC is expected to be 4.5 percent in 2026, China’s steel exports to GCC region might see further increases, and the products might be high value-added ones (e.g. HRC instead of bars).

China’s finished steel exports to Turkey are expected to further decline by 5-12 percent amid the implementation of China’s license system (and less non-VAT sales), Turkey’s challenges in the flats exports market (and less attractiveness of Chinese products compared to duty-free ones) and the spillover effects of the EU’s Carbon Border Adjustment Mechanism (CBAM) and other measures in EU like Melt and Pour -which will result in Turkey’s increased focus on own production and less use of BF imported feedstock.