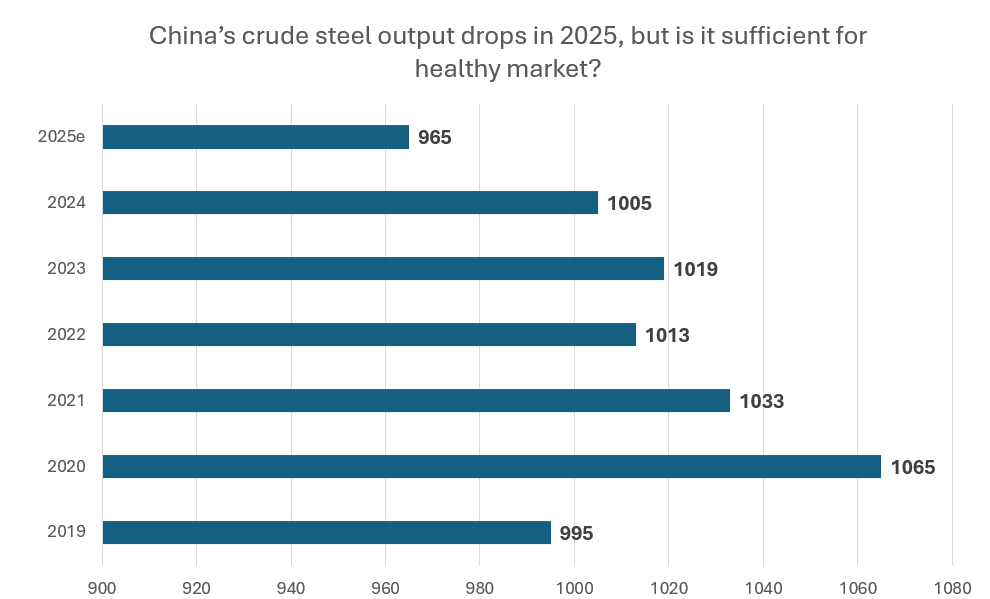

- China’s crude steel output to fall by at least 40 million mt in 2025

- The reduced output failed to support prices

- Producers follow neighbours’ attitude in adjusting output

- Government’s output control is limited to “annual cap” and “emissions punishments”

Government control of steel production, does it exist?

Officially - no, it doesn’t, especially if we compare the measures taken by the Chinese government after the oversupply crisis in 2014.

However, it does exist in a new form. Most control measures are unofficial. Early this year, rumours leaked in the market indicated that the Chinese authorities planned a cut in annual crude steel production in China by 50 million mt, which nobody (literally nobody) believed at the time. Well, we believe it now and let’s have a look how it worked.

China’s annual steel cap is set nationally, then split by province, and finally assigned to mills. “Each province must keep its full year output less than or equal to last year’s output; big state mills get firm “no growth” orders, while smaller mills are curbed flexibly via power or environmental limits,” the representative of a Chinese mill commented to SteelOrbis. If the national total is still higher than the target after two or three quarters, which happened in 2025, “the authorities tighten the screws in Q4 - so the significant cuts you see in October-December are just the final sprint to meet the annual ceiling,” he added.

In fact, many mills increased production in the first half. “There were no cuts in the first half [of 2025], so from late June we all started to receive letters from the local government with “reminders”, another Chinese source said. On the official level, the central government let steel mills produce “in accordance with the market needs”, but in fact factories in every province were following strategy of neighboring producers, being unwilling to lose market share, at least not wanting to be the first one to cut supply.

The following is an example in one province of how production controls work.

According to the information released in the first half of this year, Jiangsu Province had to reduce crude steel output in 2025 by 6 million mt compared to 2024. Accordingly, steel enterprises that have completed ultra-low emission transformation and meet the Iron and Steel Industry Specification Conditions will be subject to a five percent production cut ratio, while those that failed to meet the standards will face a stricter reduction ratio of 6-10 percent.

In 2024, Jiangsu Province’s crude steel output amounted to 119.1786 million mt. In the first ten months of 2025, Jiangsu Province’s crude steel output totaled 98.3761 million mt, signaling there would only be a 14.8025 million mt allowance for its crude steel production in the November-December period this year if it met the reduction target of 6 million mt in 2025, which would be a tough task for steelmakers in Jiangsu Province. Average monthly production in Jiangsu province was 9.8 million mt so far in 2025.

China’s crude steel output in 2025 is expected to decline by at least 40 million mt in 2025 (equivalent to 4 percent compared to 2024) to 965 million mt, SteelOrbis estimates.

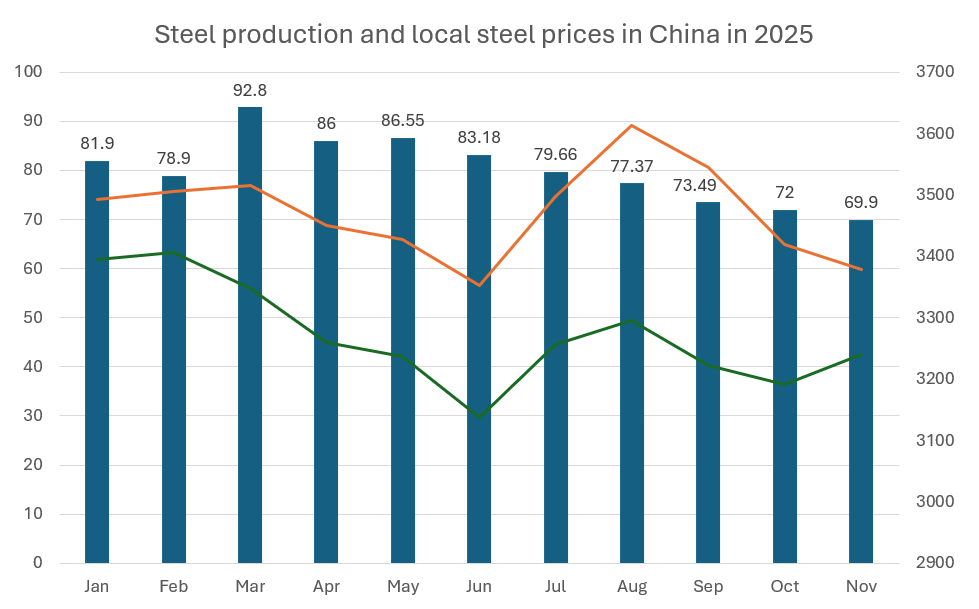

Production falls at fastest pace in five years, did it help?

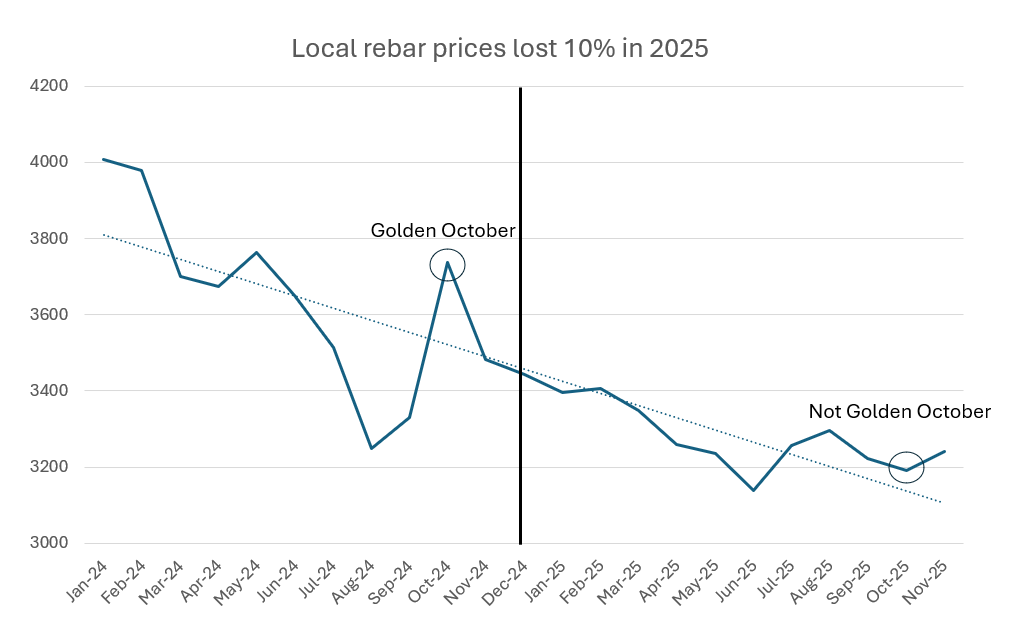

“Controlled freedom” in production has failed to help prices. In fact, local rebar prices in China have fallen by 10.2 percent or RMB 372/mt (over $50/mt) in 2025 (January-November period comparison) to RMB 3,272/mt ex-warehouse, according to SteelOrbis’ data. Though the manufacturing industry has posted a steady performance, the drop in real estate industry and construction activities has been too sharp, triggering a surge in exports.

In the first half of 2025, the correlation between production, which stayed high, and prices, which were gradually going down, continued to exist. Prices hit their lowest point of the year in June, and unexpectedly rebounded in July-August, but by the end of the year the strong production cuts that were obvious if we look at the statistics were accompanied by another fall in prices. “I would say that all futures changes and expectations of a better market in the first half of the year played their role,” a trader said.

The performance in the local HRC market has been slightly better than in the local rebar market, which suffered the most from the weak construction industry. As a result, China’s rebar production totaled 158.01 million mt in January-October, down two percent year on year, according to China’s National Bureau of Statistics (NBS), while at the same period HRC output was 187.496 million mt, increasing by 5.3 percent year on year.

New capacity policy - is it strict enough?

In 2015, the government implemented measures, controlling capacities (cutting as much as 150 million mt of sub-standard steel capacity) and making efforts to boost consumption. Since then, the control measures have changed a lot and steel mills in China have obtained some freedom with the capacity swap policy. This policy stayed in place until August 2024 and was then cancelled as it led to even some growth of capacities. A new upgraded version of the capacity replacement policy was proposed recently, and is going to play one of the main roles in the “controlled freedom” of future production.

From one side, this policy looks really strict and shows that the government has paid attention to previous mistakes and will tackle capacities. But will we see a real impact in 2026 compared to 2025?

On October 24, China’s Ministry of Industry and Information Technology (MIIT) raised the new steel capacity swap ratio to 1.5:1 (versus 1.25:1 for most BF-based mills in the previous policy), while it also strengthened the oversight of production capacity replacement.

For instance, in 24 months, the swap will be restricted to companies within the same group, with surplus capacity no longer to be transferred to outsiders. One of the large Chinese traders commented to SteelOrbis that it is not only the swap ratio that has changed, but mills overall will be less eager to use this policy in their favor in the future as “in previous years mills were trading these capacity swaps, aiming to legally increase the capacities they use”. The capacity swap policy was terminated in August 2024 and so its impact on real steel production in 2025 was less than in previous years.

At the same time, old capacity must be fully eliminated before new capacity enters into operation. Moreover, for capacity swap projects announced before August 23, 2024, construction and acceptance must be completed before October 2027.

An enterprise's ironmaking and steelmaking capacity that has been in operation for less than 90 days per year for two consecutive years shall not be used for capacity replacement. In the Yangtze River Economic Belt region, the construction or expansion of steel smelting projects outside compliant industrial parks will be prohibited. Before 2025, the capacity swap policy was actually used to increase working capacities and to make them more efficient as they were added instead of less efficient capacities or capacities in different areas. So, the new policy will combat these tricks the mills were using, but the real impact on capacity cuts remains to be seen, according to market sources.

Outlook

The stricter capacity replacement plan is aimed to further reduce China's crude steel output, and “controlled freedom” with annual production caps will remain in place, which should further reduce crude steel production in China in 2026.

According to the China Metallurgical Industry Planning Research Institute, domestic steel consumption in 2024 came to 863 million mt, equivalent to approximately 200-250 million mt of crude steel overcapacity. According to SteelOrbis Research’s estimates, crude steel production in China will drop to 900 million mt by 2030.

However, the pace of steel output decline in China in 2026 is very hard to predict with profits being at low levels, which means that production cuts have to be decent, but, with China targeting to put an end to involution-driven competition, this will promote market-driven mergers and reorganizations among steelmakers, and which may lead to more efficient production.

China’s steel production is forecast to decline by a further 15-35 million mt in 2026. The Chinese authorities will continue their efforts to shift from controlled policies toward a freedom-based approach, but whether these will be successful or otherwise is hard to say, and the Chinese steel market will still be characterized by uncertainty.