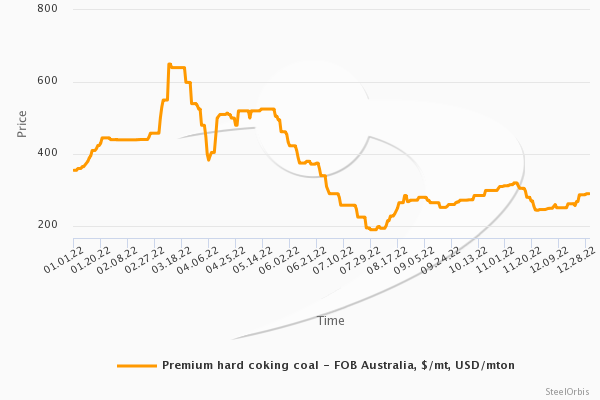

In 2022, the global coking coal market came under severe pressure. Apart from other factors, Russia's invasion of Ukraine led to disruptions of traditional supply-demand patterns, causing a sharp rise in coking coal prices.

In particular, in early March, ex-Australia premium hard coking coal prices exceeded $650/mt FOB in deals, surging by over $200/mt from the pre-war prices to the highest historical level.

However, coking coal prices at such highs were relevant during a limited period due to the absence of substantial support from the demand side.

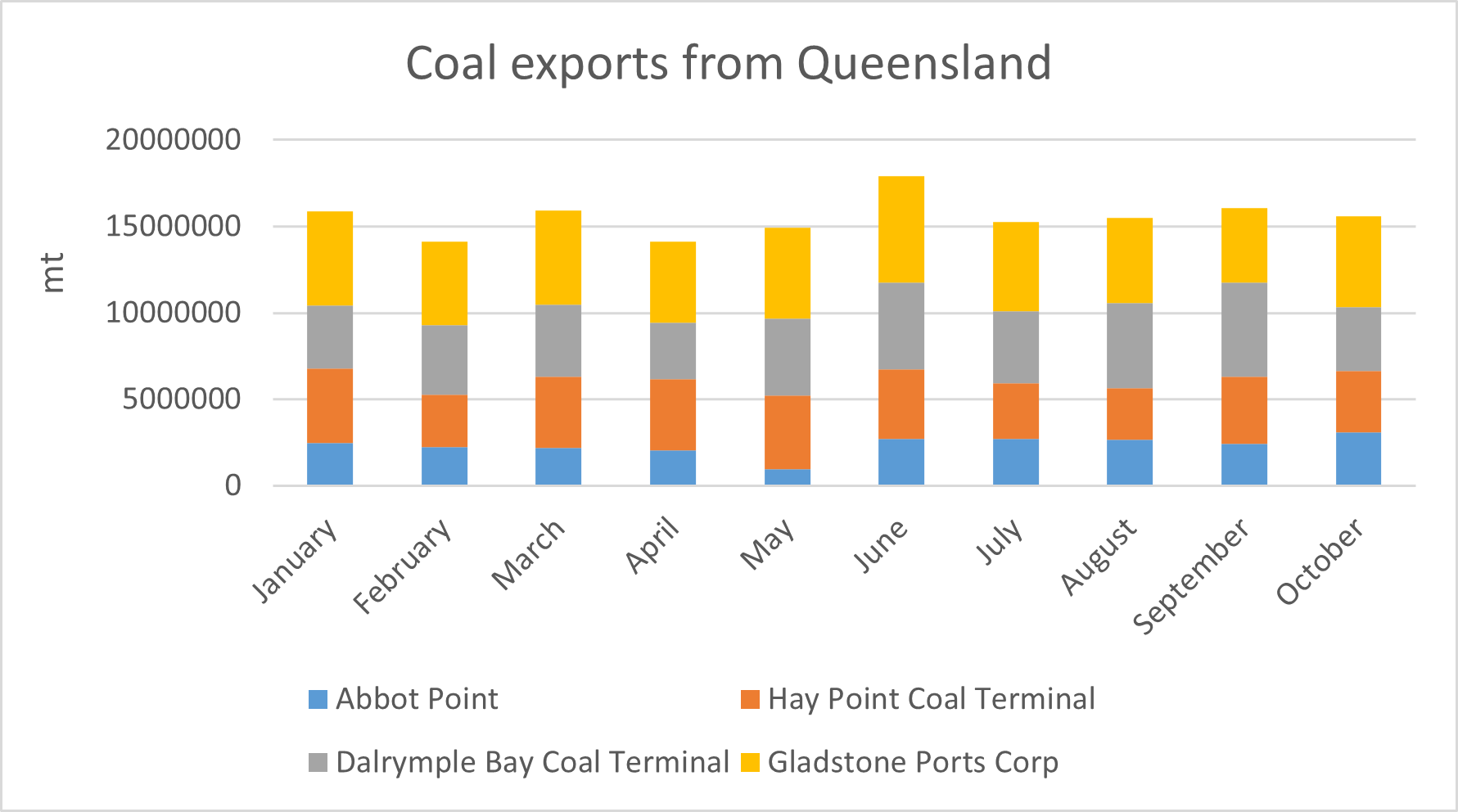

At the same time, with the world facing an energy crisis, fossil fuel prices rose sharply, forcing global customers to switch from natural gas to price-competitive options, including coal. This provided additional support for suppliers of coking coal. Specifically, aiming to capitalize on favorable thermal coal prices, global producers became increasingly focused on metallurgical coal sales into thermal coal markets, causing some decreases in coking coal supplies, which were already at high risk from weather-related issues in Australia. Specifically, the La Niña weather phenomena several times wreaked havoc across New South Wales, with coal operators impacted severely, in particular, from disruptions in ship movements and delayed maintenance works. Accordingly, total coal shipments from the major Australian ports Hay Point, Dalrymple Bay Coal Terminal (DBCT), Abbot Point and Gladstone located in the state of Queensland in the January-November period of 2022 amounted to 171.7 million mt, decreasing by 4.9 percent year on year.

The imposition by the West of sanctions on Russia along with Russian restrictions on exports of coking coal led to certain trade finance problems and seaborne logistical constraints, with buyers (primarily European) being forced to pay a premium of around $200/mt to secure prompt coal from non-Russian sources. Meanwhile, countries like China and India, on the contrary, focused on discounted ex-Russia imports. In particular, although India's total coking coal imports in the January-November period of 2022 fell by almost four percent to 48.6 million mt from 50.4 million mt in the same period of 2021, ex-Russia coking coal imports arriving in India surged by 11-fold to 1.416 million mt. Meanwhile, India’s top trading partner, Australia, saw a large decline in its share, with ex-Australia coking coal supplies to India declining by 21.5 percent year on year to 33.29 million mt in the January-November period of 2022. In the meantime, ex-US coking coal supplies to India increased by 140 percent to 6.86 million mt during the first 11 months of 2022.

Meanwhile, Russia's share in China's coking coal imports rose to 33.7 percent in the January-November period of 2022, compared to 27.2 percent in the first quarter of the year.

Coking coal demand from global end-users, in turn, remained unsustainable due to the deteriorating situation in the steel industry. According to the World Steel Association (worldsteel), in the January-November period of 2022 global crude steel production decreased by 3.7 percent year on year to 1.69 billion mt. In addition, aiming to influence the trend of coking coal prices, some global steelmakers entered the market at some point to sell coking coal which has been booked earlier, thereby exerting negative pressure on coking coal prices.

Consequently, with trade flows gradually having adjusted, by early June the Australian coking coal market retreated to the pre-war levels and afterwards prices continued to slide down further, with suppliers struggling to secure orders due to slowing global growth, which is expected to slow even further in 2023. China's policy to cap its steel output may continue to weigh on coking coal demand, in particular. Nevertheless, in the case of a recovery of trading relations between China and Australia, ex-Australia coking coal prices could gain some support from Chinese demand in 2023.