Domestic demand for wide flange beams (WFB) is currently so low that there has been little to no reaction to the latest price increase.

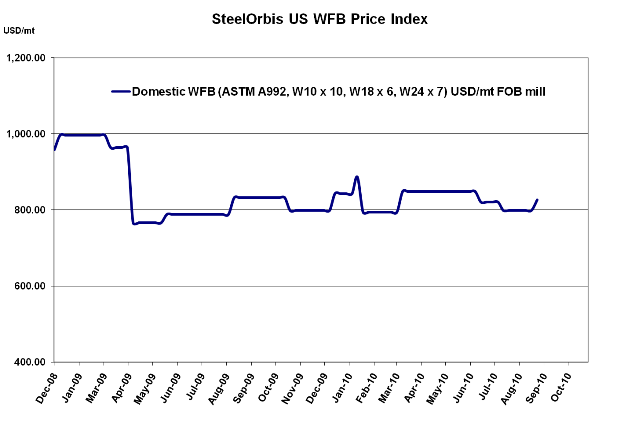

WFB mills are, for the most part, sticking to the higher prices even though business is lackluster. But service centers, feeling the brunt of scant consumption levels, have been cutting prices on anything worth quoting. For truckload or larger orders, they are willing to sell at published mill replacement costs, so their customers have been virtually unaffected by the $1.25 cwt. ($28/mt or $25/nt) transaction price increase announced earlier this month, paying about the same price they did last month (which included the service center mark-up). Current mill offering prices for WFB are listed at $37.50 cwt. ($827/mt or $750/nt) ex-mill for ASTM A992, W10 x 10, W18 x 6, and W24 x 7.

Despite the deals out there, buying activity is anemic. According to the latest MSCI Metals Activity Report, monthly shipments of WFB rose slightly in July, from 211,600 nt in June to 217,700 nt last month. However, month-ending inventory levels plummeted, from 527,800 nt in June to 494,400 nt in July, representing the lowest level for all of 2010 (the lowest, in fact, for all MSCI data going back to 2007). This indicates that service centers are eating through their inventories, and only buying higher-cost product from mills when they absolutely need it.

On the end-use side, construction is still frustratingly slow, but sources on both the West and East Coast are reporting an unlikely bright spot: custom homes. Apparently, those who were not terribly affected by the economic downturn are taking advantage of the current buyer's market and getting incredible deals on construction materials. Wide flange beams are key to custom home building, primarily for their size and strength in houses that need more than typical wood beams for support. Therefore, despite recent reports of new home sales dropping by 12 percent from June to July, there is at least one segment of construction that hasn't fallen of the cliff.

Another symptom of domestic mills' apathy toward demand conditions is their collective shoulder shrug at surprisingly low import prices. On the West Coast, beams from Korea have been heard at around $4.50 cwt. ($100/mt or $91/nt) less than current domestic mill prices. Elsewhere, import offers are quiet. European beams are not attractive enough to gain firm offers in the US, such as recently reported price from Spain at $750-$760/mt CFR FO in US Gulf Coast ports. Earlier this year, domestic mills ended their "foreign fighter" pricing, which invited mills abroad to claim some market share in the US. But because shredded scrap is forecasted to rise by as much as $40-$50/long ton in September, mills don't feel much pressure to compete with imports, especially considering that imports are drying up.

According to the latest import data from the US Import Monitoring and Analysis System (SIMA), the US imported 20,020 mt of WFB in July, slightly more than the 14,313 mt in June. However, with only a few days left in the month, August import levels are at a paltry 8,201 mt. Spain and Korea were once again the top two sources of imported beams, with 2,849 mt and 2,735 mt respectively. Luxembourg was the only source to increase beam exports to the US in July, with 2,239 mt.