What's the likelihood that the surge of Chinese steel demand in 2013 may be the last increase for quite a while? WSD thinks this is a good possibility. Consider these points:

- Adjusted fixed asset investment (gross fixed capital formation) in China is so large that it's straining the country's financial systems.

- The pace of new apartment construction is both staggering and, we believe, unsustainable.

- The country's export prospects seem to be diminishing-and especially so if governments in Advanced Countries turn mercantilistic because of their desire to boost manufacturing employment at home.

- The Chinese RMB stays strong versus the Japanese yen.

- If adjusted fixed asset investment declines as a share of GDP and household consumption rises, this is not good for steel demand since steel consumption per trillion RMB of fixed asset investment is about seven times more steel intensive than household spending.

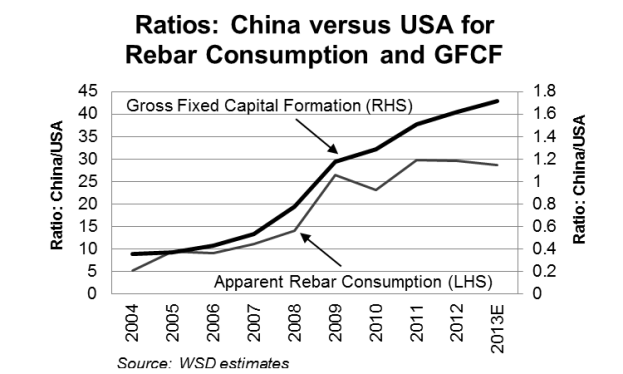

One way to judge whether or not Chinese steel demand may have risen to unsustainable levels is to consider rebar consumption in China versus the US-with the figures for 2012 at 175 and 6 million metric tons, respectively. Chinese gross fixed capital formation is about 1.6 times higher than that in the US; yet, its rebar consumption is about 30 times higher.

For additional information of WSD's services, please contact us at:

Or visit our website at:

www.worldsteeldynamics.com