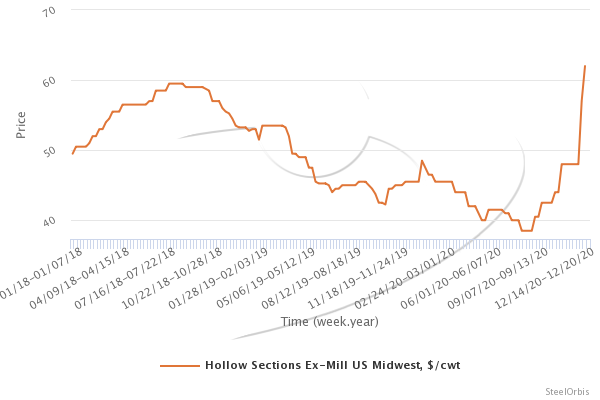

Spot market prices for US domestic hollow structural section (HSS) steel are still shooting up at breakneck speed. And while the uptrend in price is not unique to the HSS market, as scrap, flat rolled steel, energy pipe and longs prices are all rising, the pace at which HSS prices are climbing is what makes the market unique.

On December 2, US domestic tube mills announced a $5.00 cwt. ($110/mt or $100/nt) price increase, effective immediately. On December 11, a second $5.00 cwt. increase was announced, due to “rising raw material costs, strong demand, and volatility of transportation costs.”

Both increases have been accepted, which today puts US HSS spot market prices at $61.50-$62.50 cwt. ($1,356-$1,378/mt or $1,230-$1,250/nt) ex-mill, Today’s prices are higher than they were during their post-Section 232 peak, when in July 2018 spot market prices topped out at $60.00 cwt. ($1,323/mt or $1,200/nt) ex-mill. Further, today’s prices are up by an astonishing $22.50 cwt. ($496/mt or $450/nt) since late August, when HSS prices bottomed at $39 cwt. ($860/mt or $780/nt) ex-mill.

“I don’t think we’re at the top yet, but I think we’ll be there soon,” a source said. “But I wouldn’t be at all surprised if this isn’t the last increase.”