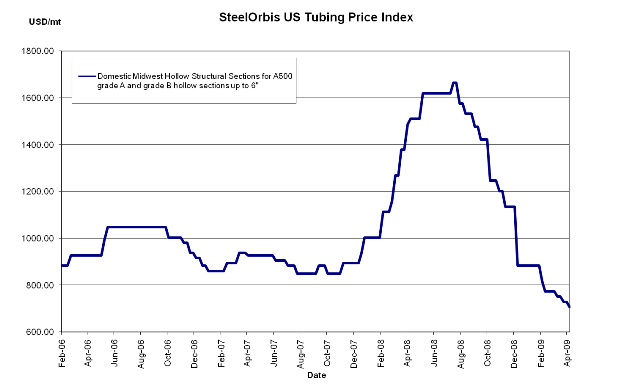

The US hollow structural section (HSS) market continues to be dominated by weak demand, leading prices to soften further in recent weeks, despite an increase in scrap prices.

US domestic HSS prices slid by about $1.00 cwt. ($22 /mt or $20 /nt) over the past couple weeks, bringing most offers to the level of $31.50 cwt. to $32.50 cwt. ($694 /mt to $717 /mt or $630 /nt to $650 /nt) ex-mill, for ASTM A500 Grade A and B, up to 6"; however, SteelOrbis has learned that for the right quantity and specs, orders can often be negotiated to a range of approximately $30.00 cwt. to $32.00 cwt. ($661/ mt to $705 /mt or $600 /nt to $640 /nt).

While prices continue their downward trend and demand remains terribly weak, the recent $45 /long ton shredded scrap price increase could pressure US domestic mills to consider keeping HSS prices firm, especially if scrap continues trending upward into June.

Nonetheless, most distributors believe that regardless of what potential positive factors there are in the market, prices will not stabilize nor improve until demand does. One distributor told SteelOrbis, "I keep saying that prices just can't drop much further, but that's also what I thought when we were at $35.00 cwt. ($772 /mt or $700 /nt). Demand just isn't picking up like we need it to and I'm now starting to think that the bottom will be at around the $27.00 cwt. to $28.00 cwt. [$595 /mt to $617 /mt or $540 /nt to $560 /nt] range."

Meanwhile, with the exception of Mexican imports, traders have been having a difficult time booking import HSS orders. Throughout this year, traders have battled against aggressive US domestic mill pricing, long overseas lead times and a lack of available vessels; however, now many foreign steel markets, such as Turkey and China, are beginning to pick up, causing these foreign mills to be even less willing to follow US domestic prices downward. The only way overseas imports can compete with US domestic offers is through incredible price discounts, which are just not feasible right now.

Mexico continues to be pretty much the only active foreign source offering HSS tubing to the US. Mills have lowered their offers by about $3.00 cwt. ($66 /mt or $60 /nt) since April, and most offers can now be found in the general range of about $27.00 cwt. to $28.00 cwt. ($595 /mt to $617 /mt or $540 /nt to $560 /nt) delivered to customers in Texas and California. Mexican mills continue to be aggressive and could offer discounts below this range on certain orders depending on order size and specifics.

Licensing data from the US Steel Import Monitoring and Analysis System (SIMA) demonstrate that total import tonnage of structural pipe and tube continued to decrease on a monthly basis in April. April import structural pipe and tube tonnage was less than half the tonnage imported in April 2008, at 17,415 mt and 39,708 mt respectively. Meanwhile, Canada and Mexico remained the two primary import sources in April, at 11,270 mt and 2,993 mt respectively. Mexico previously exported 4,393 mt of structural pipe and tube to the US in March.