During periods of highly elevated steel export and home market prices – i.e., in steel shortages – its normal for the “spreads” between the prices of different steel products and steel-related raw materials to rise to extreme levels.

In our previous Strategic Insight report – titled the “Game of Spreads: Part 1” – we examined the price spreads since 2010 for: 1) the Chinese home-market steel price versus the iron ore + coking coal cost; 2) Turkey rebar export price versus Turkey HMS 1&2 80/20 import scrap price; and 3) the USA HRB Price versus the Shredded steel Scrap Price. In this memorandum, we examine three more relationships:

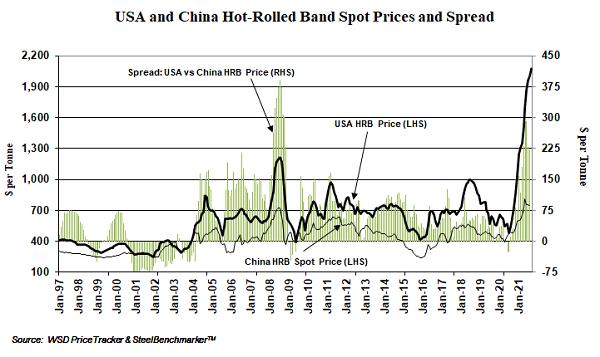

Spread 1: USA hot-rolled band price versus Chinese steel mill ex-works hot-rolled band price. While these prices don’t correlate well with one another, they provide a valuable indicator of the price paid by steel users in the two countries – which is about $1,300 per tonne less in China at the present time. The price of USA hot-rolled band is currently about $2,100 per tonne, with the ex-works China hot-rolled band price at about $750 per tonne. A spread this wide was exceeded, only briefly, in the summer 2008 when an extreme steel shortage was in effect. In the past decade, the spread has usually varied at times from $100 to $900 per tonne, with a typical figure, if there’s such a thing, at about $600 per tonne. (Note: In comparison, WSD’s estimate of the average price to be in effect over the steel cycle, from 2023 to 2030, is $640 per tonne for USA hot-rolled band and $470 per tonne for the Chinese ex-works home-market HRB price – for a spread of $170 per tonne.)

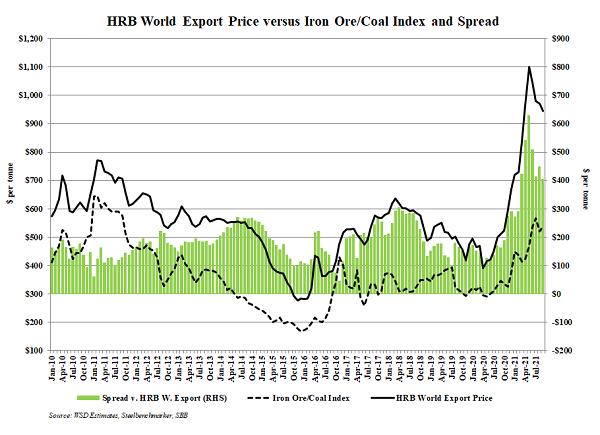

Spread 2: The HRB export price versus the iron ore and coking coal cost per tonne of steel product for the integrated steel producer. This spread is a good indicator of the profitability in the hot-rolled band business. Since 2010, the spread has swung widely and has averaged roughly $200 per tonne. In 2021, it has typically ranged from $400 to $600+ per tonne – which helps to explain why the steel mills are enjoying a “Golden Profit Age.” (Note: Based on WSD’s estimates of the average prices to be in effect over the steel cycle from 2023 to 2030, the HRB export price at $513 per tonne, FOB the port of export, compares to the iron ore and coking coal cost for the integrated producer $280 per tonne – for a spread of $233 per tonne.)

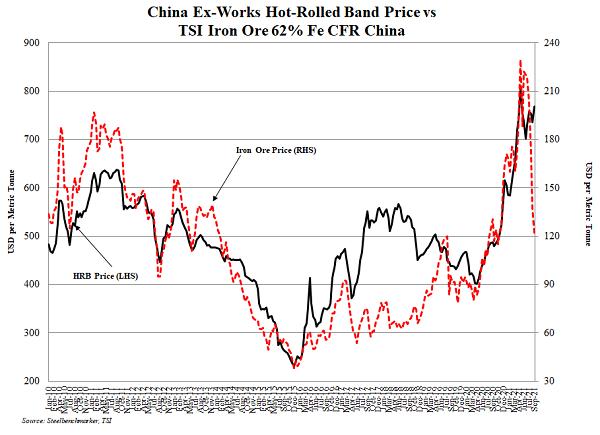

Spread 3: China Hot-Rolled Band Price versus the TSI Iron Ore Price delivered to China. Since 2010, hot-rolled band in China has typically been $300 to $450 per tonne above the iron ore price. Both prices have been highly volatile and have often moved in synch with one another. As of September 15, 2021, the spread was $646 per tonne. (Note: Based on WSD’s estimates of the average figures to be in effect over the steel cycle during 2023 to 2030, the Chinese hot-rolled band price of $490 per tonne compares to the iron ore price at $84 per tonne – for a spread at $406 per tonne.

This report includes forward-looking statements that are based on current expectations about future events and are subject to uncertainties and factors relating to operations and the business environment, all of which are difficult to predict. Although we believe that the expectations reflected in our forward-looking statements are reasonable, they can be affected by inaccurate assumptions we might make or by known or unknown risks and uncertainties, including among other things, changes in prices, shifts in demand, variations in supply, movements in international currency, developments in technology, actions by governments and/or other factors.

The information contained in this report is based upon or derived from sources that are believed to be reliable; however, no representation is made that such information is accurate or complete in all material respects, and reliance upon such information as the basis for taking any action is neither authorized nor warranted. WSD does not solicit, and avoids receiving, non -public material information from its clients and contacts in the course of its business. The information that we publish in our reports and communicate to our clients is not based on material non-public information.

The officers, directors, employees or stockholders of World Steel Dynamics Inc. do not directly or indirectly hold securities of, or that are related to, one or more of the companies that are referred to herein. World Steel Dynamics Inc. may act as a consultant to, and/or sell its subscription services to, one or more of the companies mentioned in this report.

Copyright 2021 by World Steel Dynamics Inc. all rights reserved