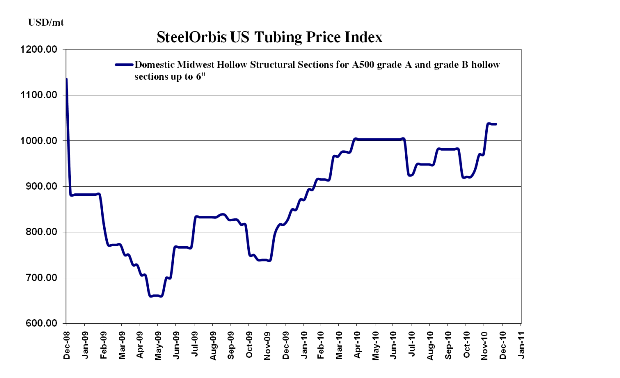

Spot prices in the US domestic hollow structural sections (HSS) market remain at last week's previously reported levels, although Atlas Tube's $2.00 cwt. ($44/mt or $40/nt) price increase announcement Monday will soon drive prices up once more.

With four price increases in hot rolled coil (HRC) announced since November 29, and spot prices for HRC up approximately $7.50 cwt. ($165/mt or $150/nt) since just before Thanksgiving, tubing market insiders predict that there could be further increases on top of Atlas' $40/nt announcement that could range anywhere from $2.00-$4.00 cwt. ($44-$88/mt or $40-$80/nt) as a reaction to escalating hot rolled prices.

Upticks in pricing in the HSS market have been consistently following those seen in HRC; however, demand levels for the two products are not as consistent. The latest data from the Metal Service Center Institute (MSCI) indicates that while monthly and daily shipments from US steel service centers of flat-rolled products were up 1.3 percent and approximately 6 percent respectively in November over the previous month, monthly and daily shipments of pipe and tube were down 6 percent and approximately 1 percent respectively over the same period.

Sources indicate that the majority of mills on the West Coast will be shutting down in the next few days, and not resuming production until the first week of January, due to the upcoming Christmas and New Year holidays, after which mills are expected to fully enforce this next set of increases, giving buyers only a small window of opportunity to place last minute orders at current spot prices. For now, tubing spot prices are still $46.00-$48.00 cwt. ($1,014-$1,058/mt or $920-$960/nt) ex-Midwest mill, while ex-West Coast mill prices remain in the $50.00-$51.00 cwt. ($1,102-$1,124/mt or $1,000-$1,020/nt) range.

Even though some import offers are looking more attractive now compared to volatile US prices, many are still holding off investing in offshore product until there is a clear indication of just how long upward pricing tendencies are going to last. "If this lasts past Q1 of next year, then I'll consider it" said one Southeast distributor. Nonetheless, tubing offers from Turkey at $44.00-$46.00 cwt ($970-$1,014/mt or $880-$920/nt) FOB loaded truck in US Gulf ports persist.