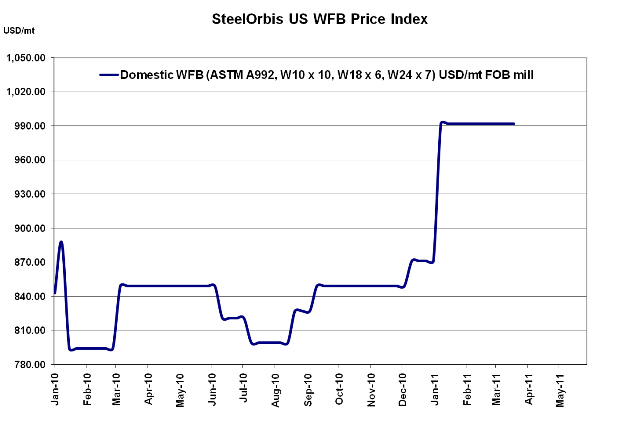

Although US domestic wide flange beam (WFB) prices have been following a neutral trend so far this year, purchasing activity levels are starting to wane.

The jump in both monthly shipments and month-ending inventories from US service centers in January was the result of buyers trying to secure tonnage before a $3.25 cwt. ($72/mt or $65/nt) price increase for February shipments. But since then, prices have not moved--a slight decrease in shredded scrap pricing in February followed by a neutral trend in March has not given US mills much reason to adjust asking prices, and as they have been selling primarily on an "as-needed" basis, there hasn't been much incentive to cut deals. Indeed, beam prices offered by service centers and distributors are slightly higher than mill asking prices, when throughout much of the last quarter of 2010, many were routinely selling product at or below mill prices.

Currently, domestic WFB prices are still listed at $45.00 cwt. ($992/mt or $900/nt) ex-mill (for ASTM A992, W10 x 10, W18 x 6, and W24 x 7), and the widespread expectation is that prices will not move for May shipments once another sideways scrap move is announced in April. While any break from wild price fluctuations is usually welcomed, this comfortably neutral trend for beams could turn sour if purchasing activity does not pick up soon.

According to the latest MSCI Metals Activity Report, monthly structural steel shipments in February totaled 187,800 nt, down from 218,500 in January. As previously mentioned, much of January's levels can be attributed to restocking ahead of the price increase, but February's levels don't exactly represent a return to the status quo--in fact, it's even lower than levels seen during the steel industry's recent "dark ages." Adding to the equation are high levels of month-ending inventories, which spiked from 502,200 nt in December to 530,300 nt in January, and only fell by 5,000 nt in February. A measurable uptick in demand would theoretically balance out inventory and shipments, but according to various economic indicators, commercial construction is not expected to see a major boost anytime this year--the much-anticipated spring construction season will likely be an improvement on 2010, but probably not enough for the sector to declare itself "recovered."

Not surprisingly, import offers for WFB are being largely ignored, even though prices have not changed much in the last month. Offers from Korea are still approximately $44.50 cwt. ($981/mt or $890/nt) duty-paid FOB load truck in West Coast ports, with some offers heard at slightly higher levels, but until US beam buyers are more certain of what the spring construction season holds, they are not eager to purchase product 2-3 months out.

As for imports arriving this month, shipment levels reflect the spike in import inquiries that followed rising domestic prices in early January, but the numbers will probably drop off in the coming months. According to import license data from the US Import Monitoring and Analysis System (SIMA), the US has imported 13,521 mt of WFB H-sections and 6,760 mt of I-sections so far in March, reflecting an increase of 92 percent and 205 percent, respectively, from February levels. Korea continued to be a top source of H-sections, but South Africa, usually a relatively stable background player, has so far surpassed Korea's numbers--6,759 mt compared to 6,164 mt. Luxembourg, which is traditionally a major source of beams to the US, has only accounted for 306 mt of H-sections in March. Conversely, Luxembourg is the number two source of I-sections to the US so far in March, with 1,175 mt only topped by South Africa's 4,805 mt.