After their successful flat steel sales activity in Far East Asia, the CIS countries are now trying to impose similar flat steel price levels on Europe. However, the current flat steel offers to Europe of the CIS producers, who gained some relief from their sales to the Far East, are said by market players to lack competitiveness.

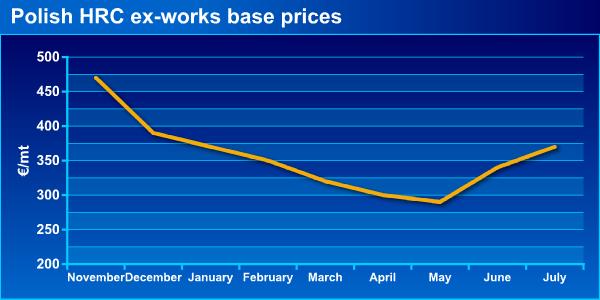

On the other hand, it is expected that the HRC ex-works price levels in Poland may increase by $30/mt to €370/mt, in line with the price announcement made by ArcelorMittal Flat Carbon Europe. Including this price expectation for July, HRC ex-works price levels in Poland in the nine-month period from November 2008 to July 2009 are as follows:

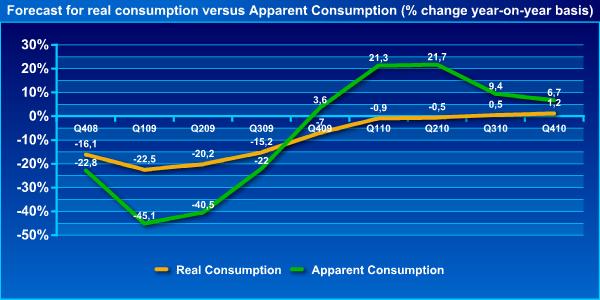

According to the World Steel Association data, overall global steel demand has increased by 21 percent year on year in the first five months of 2009, though the EU 27 has registered a decrease of 44.4 percent over the same period. Additionally, since European distributors have now switched to purchase mode, demand in Europe has gained some momentum compared to recent months. Thus, with the help of the strong ex-CIS prices, the ground has now been prepared for a price increase by the European producers. However, besides the increase in apparent demand, it is really hard to affirm that the uptrend will be sustained, unless end-users enter the market and push real demand up. As may be recalled, as expected by Eurofer and as presented below, real demand was not expected to catch up with apparent demand before October.

Local production and import flat steel price levels in Poland are currently as follows:

Origin | Product | Price | Terms |

€340/mt (base) | ex-works | ||

€400/mt (base) | ex-works | ||

HDG | €430/mt (base) | ex-works | |

€330/mt | DAF Poland | ||

€340/mt | DAF Poland |