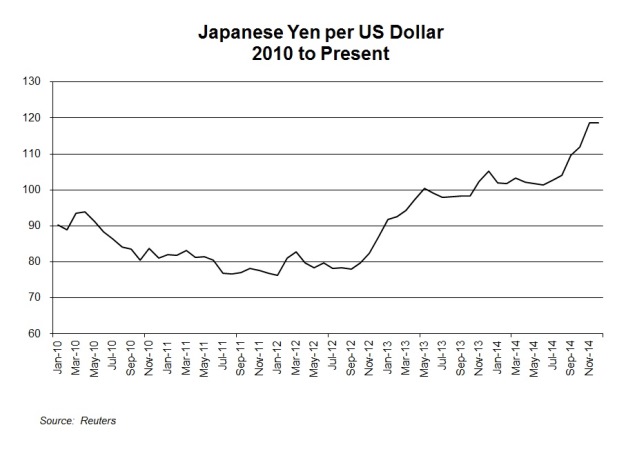

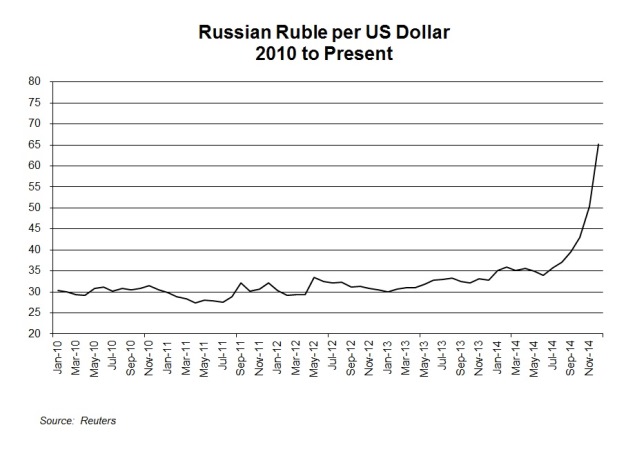

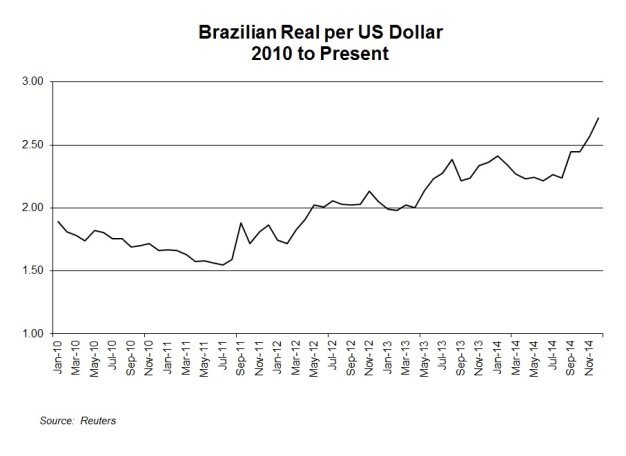

The graphics below portray the significant currency devaluation versus the US dollar for Japan, Brazil and, especially, Russia. These devaluations have improved the cost competitiveness of these groups. The Russian steel mills, by far, are now the lowest cost in the world.

So far this year, versus the US dollar, the currencies of Japan, Brazil and Russia have weakened about 16 percent, 10 percent and 107 percent, respectively. We estimate that about two thirds of Japan’s and Brazil’s costs are denominated in the home currency, and 70-80 percent of Russia’s costs.

The stronger the dollar, all other things held the same, the lower the price of HRB in the world market. With the Russian ruble at about 65 per US dollar, the operating cost to produce hot-rolled band in Russia may be only $270 per tonne.

This report includes forward-looking statements that are based on current expectations about future events and are subject to uncertainties and factors relating to operations and the business environment, all of which are difficult to predict. Although we believe that the expectations reflected in our forward-looking statements are reasonable, they can be affected by inaccurate assumptions we might make or by known or unknown risks and uncertainties, including among other things, changes in prices, shifts in demand, variations in supply, movements in international currency, developments in technology, actions by governments and/or other factors.

The information contained in this report is based upon or derived from sources that are believed to be reliable; however, no representation is made that such information is accurate or complete in all material respects, and reliance upon such information as the basis for taking any action is neither authorized nor warranted. WSD does not solicit, and avoids receiving, non-public material information from its clients and contacts in the course of its business. The information that we publish in our reports and communicate to our clients is not based on material non-public information.

The officers, directors, employees or stockholders of World Steel Dynamics Inc. do not directly or indirectly hold securities of, or that are related to, one or more of the companies that are referred to herein. World Steel Dynamics Inc. may act as a consultant to, and/or sell its subscription services to, one or more of the companies mentioned in this report.

Copyright 2014 by World Steel Dynamics Inc. all rights reserved