SteelOrbis Shanghai

China's steel market has experienced a sharp fluctuation since mid-May. The price index of domestic flat rolled products (including hot rolled, cold rolled, galvanized and sheets, coils and plates) was at 116.71 points at the end of March, according to the steel index issued by the China Iron & Steel Association (CISA). However, the index had dropped by 0.96 points to 115.75 points by the end of June, which can be considered a big slump. Meanwhile, the plate price index was at 126.59 points at the end of March, increasing by 4.7 points to 131.29 points by the end of June. Despite the overall decline in flat rolled products, plates managed to achieve an impressive increase with an extraordinary, strong performance. This increase was beyond the expectations of the steel industry and all market players. What was the reason behind this phenomenon? The question may be answered by taking into account several essential factors.

1. Attitude of market & steel mills

Generally speaking, short term prices are determined according to the psychological mood in the market. In particular, against the general downward trend, which was caused by the macro adjustment at the end of May, the strong performance of the plate price was closely connected to the psychological mood or attitude of the market and mills. Although the prices of other products were falling at the end of May and in June, both the distributors and the mills were somehow confident that plate prices would not decrease in the future. Therefore, no panic sales were noted. As plates supplies were tight in the market, the distributors did not see the necessity of reducing their prices. Similarly, while the steel mills were reducing their prices for other products, the ex-factory price for plate continued to either rise or remain stable. Furthermore, the prices of some plates, such as shipbuilding plates, even rose sharply. Of course, the optimism of market players and the strong performance did not occur blindly. They were based on certain factors: the limitation of new production capacity, strong domestic demand, and the favorable export situation all played an essential role in supporting both the actual market and its psychological mood.

2. Limited production, strong domestic and foreign demand

a. Limited plate production capacity and optimization of industrial structure

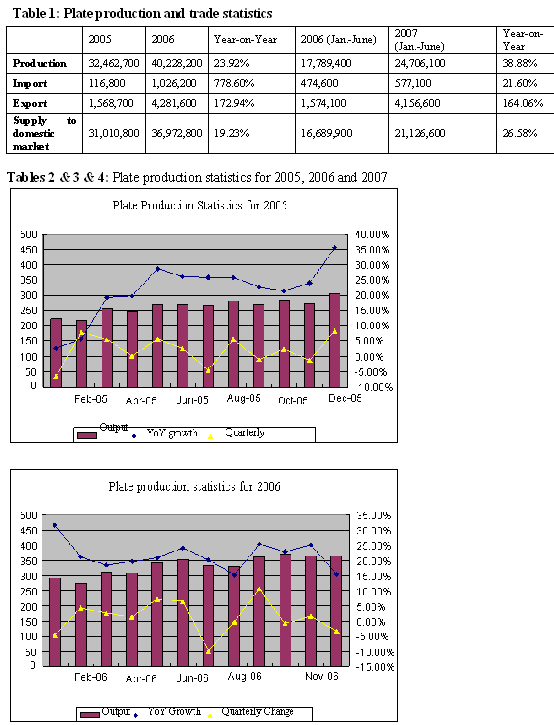

Last year, the plate production capacity saw a concentration. In 2006, 40.2282 million metric tons of plates were produced, up 7.76 million metric tons or 23.92 percent compared to the previous year (32.4627 million metric tons). Influenced by the sharp increase in plate production, the whole trend for the 2nd half of 2006 was weak and the price fluctuated at a low level around RMB 3,500/mt. According to the statistics, cumulative production from January to June 2007 is 24.7061 million metric tons, up 38.88 percent compared with 17.7894 million metric tons produced during the same period of last year. According to the comparison in the following table, production in the 2nd half of 2006 reached 22.4388 million metric tons, while production in the 1st half of 2007 is only 2.2673 tons higher, indicating very little growth. As the rapid increase in the release of supply to the domestic market in the 2nd half of 2006 is almost over, plate prices have become firmer this year.

Table 1: Plate production and trade statistics

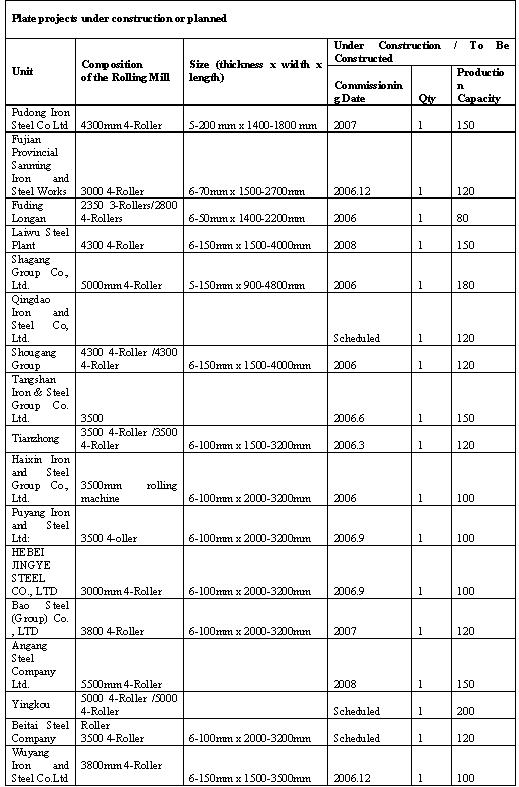

In the 2nd half of last year, up to 12 plate rolling mills were built and put into operation. Besides, there are several plate rolling mills currently being constructed. The average production capability of the newly-built rolling mills is over one million metric tons. When the modernization of older production lines is added, the total increase in production capacity nears 15 million metric tons. Of this 15 million metric tons, only less than three million metric tons was added in the first half of 2006, while the major portion was added in the second half of that year.

Table 5: Plate projects under construction or planned

Currently the price difference between hot rolled coil and plate has increased to RMB 500/mt. In the 1st half of this year, hot rolled coil production capacity increased sharply due to the new hot rolling lines at Masteel and Shougang Group which came on stream. Besides, Anyang's new mill, which will start production soon will also have a great impact on the market. Under the influence of these factors, the gap between hot rolled coil and plate prices is expected to expand further.

Many steel mills started to plan production structure adjustments before last year ended. They are not only aiming to increase production, but also to produce high value added products. As the export market is more profitable, mills are now aiming to manufacture products suitable for export, and plates for special purposes are heading the investments made in this respect.

In this regard, the proportion of carbon plates in total plate production slipped from 45.2 percent in January-May 2006 to 38.6 percent in the same period of this year. Meanwhile, the share of shipbuilding plates increased from 16.4 percent to 20.7 in the same period. The proportion of other special-purpose plates such as boiler plates, pressure vessel plates, bridge plates, container plates and pipeline plates also increased by varying degrees.

b. Positive Chinese economy boosts domestic demand

According to the National Bureau of Statistics of China, in the 1st half of 2007, capital assets in the entire country and urban capital assets increased by 25.9 percent and 26.7 percent year on year respectively.

In addition, the Chinese shipbuilding industry has been developing rapidly since the 1990s. Global demand has been strong in recent years, while the shipbuilding capacity of the previous two largest producer countries - Japan and South Korea - has not expanded sufficiently. Chinese shipbuilding companies have successfully won a large number of orders. According to the statistics, China surpassed Japan to become the 2nd largest shipbuilding country in 2006, and its new orders in the 1st quarter of 2007 even exceeded both Japan and South Korea to rank first in the world.

c. Strong international demand and robust price of plate

In the international market, though the demand for other flat steel products has gradually become weaker, the demand for plates remained relatively strong. The demand for plates from the shipbuilding, construction and energy industries is absolutely outstanding. The import volume of plates in European countries like Spain, Germany and France has substantially increased, while, the import volume in South American countries such as Brazil is also rising.

The strong demand contributes to a continuous price increase trend. The ex-factory price of plates in northern Europe increased from Euro 705-790/mt at the beginning of this year to Euro 750-815/mt in July. Meanwhile, import prices of plates to CIS countries increased from from $600/mt CFR in April to $620/mt.

The international market demand for plates has resulted in substantial growth of Chinese plate exports this year. China exported 3.33 million tons of plates this year, up 2.18 million tons or 190 percent from the same period of last year.

With the optimization of their production structure, more and more steel mills are trying to cut out the traders and to increase their share of direct supply to end-users. Their aim is to establish long-term relations with end-users and so increase their profits. Considering the strong direct demand in the shipbuilding, boiler, electric power and petrochemical industries, the importance of these moves is understood more easily. For this purpose, mills are targeting foreign customers. In this context, in the first seven months of 2007, some mills have already exported more plates than their total in 2006.

All in all, excepting any negative eventualities - such as an increase in the export tariff - plate prices are expected to remain strong for the remainder of the current year. Of course, there may be fluctuations, but the rates are expected to remain firm. Last but not least, Chinese plates have now entered an export-oriented orbit. Therefore, the international market will be the basic determining factor in the future.